Paradox Interactive (OM:PDX): Valuation Insights After Major Franchise Launches and Europa Universalis V Release

Paradox Interactive (OM:PDX) has been busy, with the company unveiling a series of high-profile releases across its legendary strategy franchises. Europa Universalis V, Surviving Mars: Relaunched, and major expansions for Crusader Kings III and Age of Wonders 4 all arrived this month.

See our latest analysis for Paradox Interactive.

Despite a string of major game launches, including Europa Universalis V and expansions for Surviving Mars, Crusader Kings III, and Age of Wonders 4, Paradox Interactive’s share price return year-to-date is down over 22%, with a one-year total shareholder return of -7.8%. Recent momentum appears muted following these releases, suggesting that the market is yet to reprice on growth potential or has concerns about longer-term delivery.

If you're tracking strategic publishers like Paradox, it might be time to broaden your search and uncover fast growing stocks with high insider ownership

With all these blockbuster launches, is Paradox Interactive trading at a discount with upside not yet recognized by the market? Or is the recent performance proof that investors are already pricing in the company's future growth?

Most Popular Narrative: 18.4% Undervalued

Paradox Interactive's most prominent valuation narrative places fair value at SEK201.67, while the last close sat notably lower at SEK164.5. With the market lagging behind updated forecasts, factors driving this valuation are under close scrutiny.

The company's strategy of maximizing recurring revenue through expansions (DLCs), game subscriptions, and live-service updates for established franchises capitalizes on growing consumer demand for ongoing digital game experiences. This approach supports durable and high-margin cash flows. Continued global adoption of digital distribution platforms like Steam and Epic reduces distribution costs and gives Paradox greater access to worldwide audiences. This is likely to enhance both sales potential and net margins over the long term.

Curious about why this narrative points to Paradox leaping above current prices? The secret sauce is in aggressive margin forecasts and franchise longevity assumptions. Tempted to see which future earnings projections turn this 18% discount into reality? Uncover the full storyline behind this bold valuation.

Result: Fair Value of SEK201.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy reliance on evergreen franchises and unpredictable revenue from major releases could challenge Paradox’s growth if new titles underperform or audiences shrink.

Find out about the key risks to this Paradox Interactive narrative.

Another View: Multiples Paint a Pricier Picture

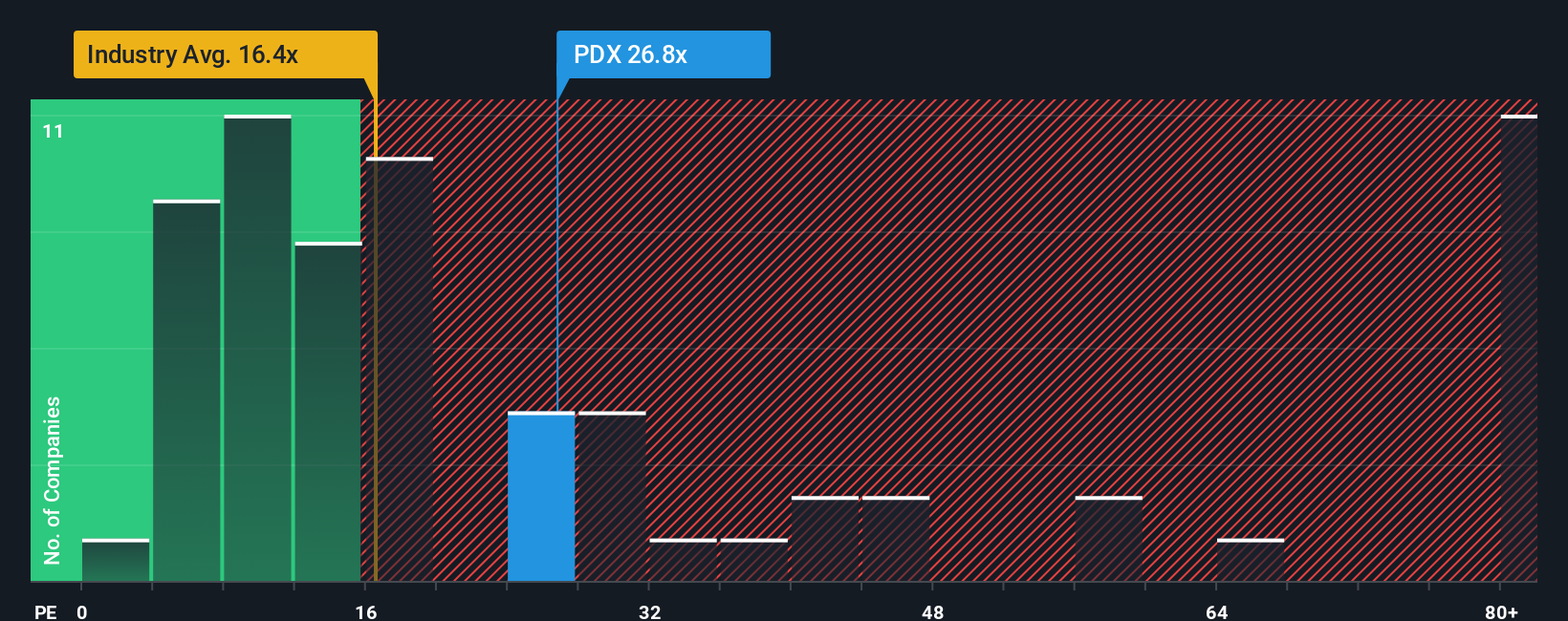

While many see upside from Paradox Interactive’s fair value, the classic price-to-earnings lens tells a different story. Paradox trades at 27.2x earnings, making it more expensive than both the European entertainment sector average of 15.6x and similar peers at 16.2x. Even compared to its fair ratio of 24.8x, the shares appear a little rich, which suggests less margin of safety if growth expectations slip.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Paradox Interactive Narrative

If you want to challenge these narratives, or dig into the figures and craft your own interpretation, you can do just that in minutes: Do it your way

A great starting point for your Paradox Interactive research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep an eye on new opportunities. Don’t let the next big winner slip by. Use these tailored lists to uncover potential market leaders today.

- Boost your income stream by reviewing these 16 dividend stocks with yields > 3%, which offers yields above 3% for stable, long-term returns.

- Tap into cutting-edge growth by checking out these 32 healthcare AI stocks, which is driving breakthroughs in digital health and medical AI innovation.

- Seize undervalued potential by targeting these 883 undervalued stocks based on cash flows, priced below their true cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com