Is There Still Room for Nvidia After a 37.5% Jump in 2025?

- Wondering if NVIDIA's meteoric rise is justified, or if all the excitement has pushed the stock beyond its true value? You're not alone. Figuring out what the company is really worth has become a hot topic for investors and curious market-watchers alike.

- NVIDIA's stock has surged 37.5% year-to-date and more than doubled over the last three years, suggesting there could be both growing optimism and higher expectations built into the price.

- This momentum hasn't come out of nowhere. Fresh advances in artificial intelligence, new product announcements, and partnerships across major tech sectors have kept NVIDIA in the headlines, fueling investor enthusiasm. As chipmakers race to power the next wave of AI development, NVIDIA's unique position has attracted attention from both Wall Street and the broader tech world.

- Yet when we break down the numbers, NVIDIA only scores 2 out of 6 on our undervalued checks, raising interesting questions about its current price tag. Next, we'll dig into the most common ways to judge the company's value, before exploring what might be an even better approach in the conclusion.

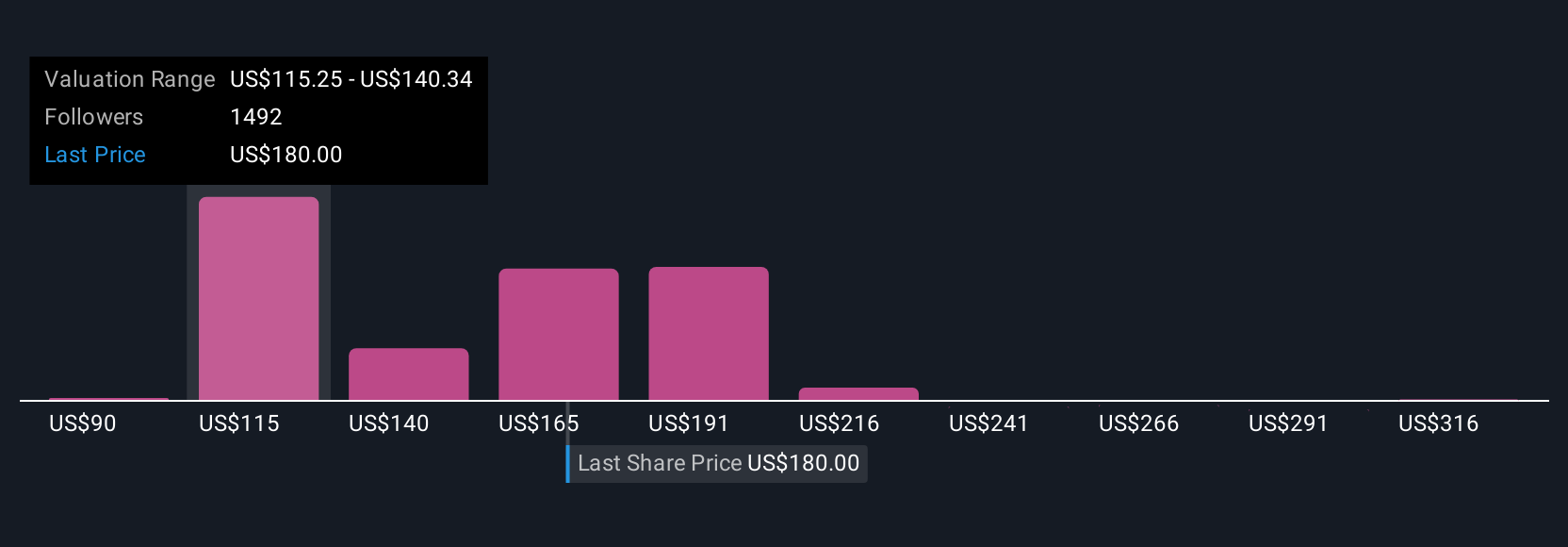

NVIDIA scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: NVIDIA Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. This method reflects what those future earnings are worth currently. It is widely used in finance to evaluate long-term growth prospects and underlying business strength.

For NVIDIA, the most recent reported Free Cash Flow stands at $72.28 billion. Analysts provide free cash flow estimates for the next five years, with projections rising from $96.56 billion in 2026 to $210.21 billion in 2029. Simply Wall St extends these forecasts beyond analyst estimates and anticipates that NVIDIA's free cash flow could reach $284.04 billion by 2030, with further growth projected through extrapolation.

According to this DCF analysis, NVIDIA's estimated fair value per share is $165.10. However, based on current trading levels, this suggests the stock is approximately 15.2% overvalued when measured against its projected cash flow generation.

In summary, while NVIDIA's growth outlook is compelling and its future cash flows appear strong, the market price currently reflects a high level of optimism, more than the numbers support at this time.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NVIDIA may be overvalued by 15.2%. Discover 879 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NVIDIA Price vs Earnings (PE Ratio) Analysis

The Price-to-Earnings (PE) ratio is widely regarded as one of the best ways to value profitable companies like NVIDIA, since it relates the company’s stock price directly to its operational earnings. It’s a quick way to gauge how much investors are willing to pay for each dollar of earnings, which often reflects growth expectations and perceived risk. Generally, a higher PE ratio can signal that investors expect above-average growth, while a lower PE might suggest more modest prospects or higher risk.

NVIDIA’s current PE ratio stands at 53.4x, which is notably higher than the semiconductor industry average of 34.0x and also above its peer group’s average of 70.1x. To provide a fairer benchmark, Simply Wall St calculates a proprietary “Fair Ratio” for NVIDIA by taking into account not just earnings growth, but also factors such as margin strength, industry dynamics, market capitalization, and company-specific risks. For NVIDIA, the Fair Ratio is pegged at 65.8x.

The Fair Ratio provides a more tailored guide than generic industry averages or peer comparisons because it adapts to NVIDIA’s unique characteristics. By weighing in growth opportunities, profitability, market size, and risk profile, this measure helps investors judge valuation more accurately than simply stacking numbers up against competitors.

Comparing NVIDIA’s current PE of 53.4x to its Fair Ratio of 65.8x, the stock appears undervalued by this measure. This suggests investors may not be fully pricing in the company’s standout strengths or future potential.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1406 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your NVIDIA Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, a dynamic approach that helps you move beyond static numbers to connect your view of a company's story with a financial forecast and, ultimately, a fair value.

With Narratives, you build your own perspective about NVIDIA by describing the story you believe in, combining your estimates for future revenue, profit margins, and key risks or opportunities to create a personalized forecast and fair value assessment. Narratives help you think through the 'why' behind the numbers, making your investment decision more meaningful and transparent.

This easy-to-use tool is available directly on Simply Wall St’s Community page, empowering millions of investors to share their logic, compare assumptions, and see how their beliefs stack up against others'. Narratives are dynamic and automatically update when major news, earnings, or product launches affect NVIDIA’s business outlook, keeping your fair value relevant in real time.

By comparing your Narrative’s fair value to the current price, you can act with confidence, knowing not just what you think NVIDIA is worth, but why. For example, some investors see NVIDIA’s fair value as low as $68, reflecting cautious growth and margin assumptions, while others project targets as high as $341 by expecting market leadership and robust expansion; Narratives allow you to chart your own course in this wide spectrum.

For NVIDIA, we will make it really easy for you with previews of two leading NVIDIA Narratives:

- 🐂 NVIDIA Bull Case

Fair Value: $232.79

Current Price is 18.3% above this fair value

Projected Revenue Growth Rate: 30.36%

- Analysts see surging AI adoption and innovation driving strong, multi-year data center demand and revenue growth potential for NVIDIA.

- NVIDIA’s end-to-end platform strategy and recurring software revenues reinforce powerful margins and customer lock-in, supporting higher long-term earnings.

- Risks include geopolitical tensions, hyperscalers opting for custom chips, and supply chain fragilities. Overall, consensus is upbeat, with analysts' 2028 fair value target at $207.02 and the bullish end topping $270.

- 🐻 NVIDIA Bear Case

Fair Value: $67.95

Current Price is 179.9% above this fair value

Projected Revenue Growth Rate: 14.4%

- Emerging competitors (AMD, Samsung, Intel) and major customers (Amazon, Google, Microsoft) developing in-house chips could squeeze NVIDIA’s market share and margins over time.

- Revenue cannibalization is possible from hyperscalers and cloud providers prioritizing cost-effective solutions or vertically integrating, while gaming segment growth may stagnate, reducing potential upside.

- The bear case projects significant downside risk, with resurgent supply from chiplet technology, high capex requirements, and increased market competition potentially dragging fair value as low as $67.95.

Do you think there's more to the story for NVIDIA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com