A Fresh Look at Atlas Copco (OM:ATCO A) Valuation Following Recent Share Price Pullback

Atlas Copco (OM:ATCO A) shares have caught some attention this month as investors assess recent shifts in valuation. With its performance over the past month showing a small dip, there is renewed interest in what might lie ahead.

See our latest analysis for Atlas Copco.

Atlas Copco’s share price has pulled back over the past month, extending a trend that has seen a 9.7% decline year-to-date. While momentum has faded lately, the wider view reveals long-term holders are still well in the green with a 25.9% total shareholder return over three years and 55.2% over five years.

If you’re interested in discovering what sets market standouts apart, now is a great time to broaden your search and explore fast growing stocks with high insider ownership

With shares pulling back and growth forecasts still positive, the crucial question is whether Atlas Copco is now undervalued, or if investors have already factored in all future upside. Is this a true buying opportunity, or is the market one step ahead?

Most Popular Narrative: 11.5% Undervalued

Atlas Copco’s narrative fair value stands at SEK175.06, notably higher than the last close price of SEK155. This suggests market expectations may have lagged behind recent improvements in profitability and underlying business momentum.

Sustained investments in product innovation, including AI-driven efficiency in compressors and launches such as the new GHS pump VSD+, position Atlas Copco to benefit from ongoing shifts toward automation, energy efficiency, and digitalization in industrial and infrastructure markets. These trends enhance long-term revenue growth and support premium pricing power.

Curious what bold, data-driven assumptions are powering this valuation jump? There is a sharp focus on margin strength and future earnings potential. Want to see which critical forecasts could shake up the outlook? Find out what’s behind these numbers in the full narrative.

Result: Fair Value of $175.06 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent currency headwinds and ongoing weakness in large-order segments could threaten Atlas Copco's growth outlook in the near term.

Find out about the key risks to this Atlas Copco narrative.

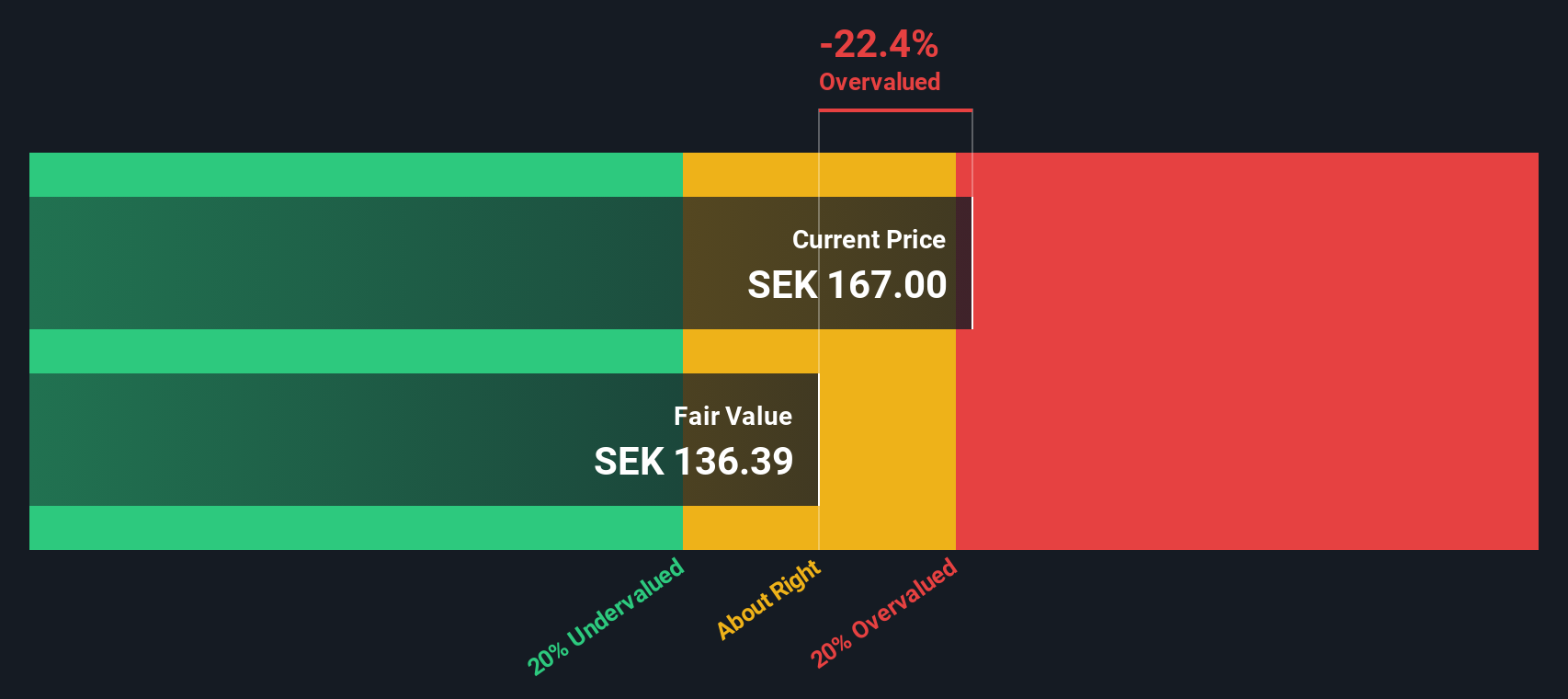

Another View: What About Discounted Cash Flow?

While market narratives suggest Atlas Copco is undervalued, our SWS DCF model arrives at a more cautious conclusion. According to this approach, Atlas Copco is actually trading above its fair value estimate. This hints at less upside and possibly more risk. Which story best reflects reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Atlas Copco for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Atlas Copco Narrative

If you have a different perspective or want to dive into the underlying figures yourself, you can create your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Atlas Copco.

Looking for more investment ideas?

Don't miss your chance to seize tomorrow’s winners. Put your portfolio ahead by tapping into handpicked opportunities that go beyond the obvious and set you apart from the crowd.

- Capitalize on sustainable cash flow by targeting value opportunities with these 879 undervalued stocks based on cash flows.

- Tap into innovation and growth by zeroing in on breakthrough technologies powered by these 25 AI penny stocks.

- Lock in reliable returns by uncovering yield-focused picks through these 16 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com