United States Antimony (UAMY) Is Down 11.3% After Landing $352 Million in Multi-Year Supply Deals

- United States Antimony Corporation recently announced its third quarter 2025 results, reporting revenues of US$8.7 million and a net loss of US$4.78 million, while also securing two major five-year supply contracts with the U.S. government and a domestic industrial manufacturer valued at a combined US$352 million.

- The new US$106.7 million supply agreement with a U.S. industrial fabric manufacturer highlights growing industrial emphasis on reshoring critical mineral supply chains and seeking domestic partners for supply security.

- Now, we'll consider how the addition of these long-term contracts and robust revenue growth informs United States Antimony's investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

United States Antimony Investment Narrative Recap

To be a United States Antimony shareholder, you need to believe in domestic supply chain security for critical minerals and the company's ability to turn rapidly rising revenues and hefty new contracts into operational scale and eventual profits. While securing two major long-term supply contracts provides clear revenue visibility and addresses demand certainty, a short-term catalyst, the most significant risk remains execution: operational and regulatory setbacks, particularly with new mining projects, could constrain USAC’s ability to deliver on these agreements. The latest agreements do not directly override these immediate operational challenges, so the risk profile for near-term profitability and margin expansion remains unchanged for now.

Of the recent announcements, the new US$106.7 million, five-year supply agreement with a U.S. industrial fabric manufacturer stands out for its relevance, as it highlights the company’s growing role in reshoring critical mineral supply chains and underpins future revenue stability, an important factor for those prioritizing demand reliability as a catalyst. However, the translation of contract wins into sustainable bottom-line growth still depends largely on overcoming ongoing production ramp-up and supply chain hurdles.

But in contrast to these opportunities, investors should be aware that persistent permitting delays and regulatory opposition could stall production growth just as new contracts come into force…

Read the full narrative on United States Antimony (it's free!)

United States Antimony's narrative projects $208.1 million revenue and $82.5 million earnings by 2028. This requires 100.7% yearly revenue growth and an $83.4 million increase in earnings from the current -$889.8 thousand.

Uncover how United States Antimony's forecasts yield a $7.50 fair value, in line with its current price.

Exploring Other Perspectives

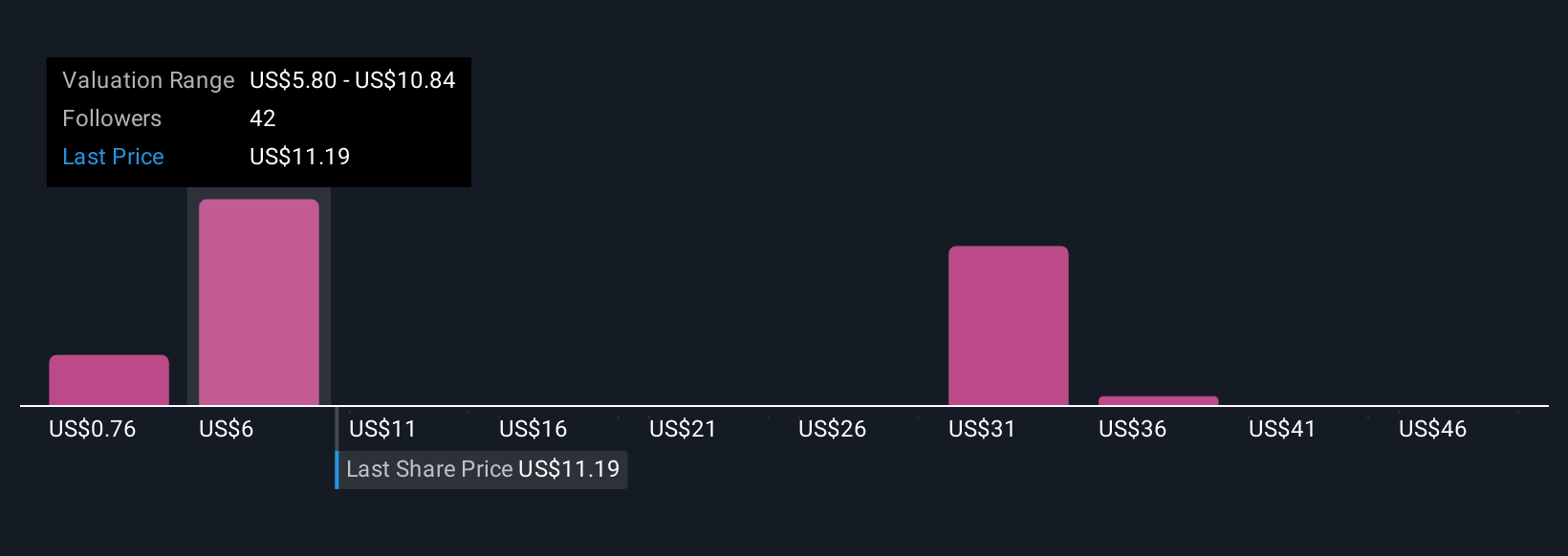

Twenty-one fair value estimates from the Simply Wall St Community range widely between US$0.76 and US$51.17 per share. As opinions swing, remember that upcoming production expansion and regulatory risks can shape outcomes very differently depending on execution.

Explore 21 other fair value estimates on United States Antimony - why the stock might be worth over 6x more than the current price!

Build Your Own United States Antimony Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your United States Antimony research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free United States Antimony research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United States Antimony's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com