Ivanhoe Mines (TSX:IVN): Valuation Insights After Major Insider Exits Top Shareholder

CITIC Metal Africa Investments Limited, which previously held 10% of Ivanhoe Mines (TSX:IVN), has fully exited its position after selling 300,000 shares on November 7th for $3.8 million. Major insider moves like this can spark discussion around the company’s outlook, particularly among investors tracking changes in shareholder structure.

See our latest analysis for Ivanhoe Mines.

Ivanhoe Mines’ share price recently closed at $12.56, following a challenging stretch that saw a sharp 20.8% decline over the past month and a 9.1% gain in the last 90 days. While the 1-year total shareholder return stands at -29.1%, longer-term holders are still comfortably ahead, with a 116.9% total return over five years. The stock’s volatility and insider activity are sparking renewed debate about future growth versus risk as investor sentiment shifts.

If the shifts in Ivanhoe Mines have you curious about broader trends, now is the ideal time to broaden your search and discover fast growing stocks with high insider ownership

So as Ivanhoe Mines weathers outsized volatility and high-profile insider exits, is this recent weakness a rare chance to invest at a discount? Or is the market already accounting for all of the company’s future growth prospects?

Most Popular Narrative: 31.9% Undervalued

With the widely followed narrative suggesting Ivanhoe Mines could be trading at a substantial discount to its fair value, the latest close of CA$12.56 is far below the consensus valuation estimate. This context sets up a key catalyst for what might drive the outlook from here.

Completion and ramp-up of the Kamoa-Kakula smelter (targeted for September) and the associated drop in logistics costs are expected to meaningfully reduce unit costs, directly boosting future operating margins and cash flow.

Ever wondered what bold operational targets underpin this upbeat valuation? The full narrative hides some aggressive revenue forecasts, massive margin shifts and a long-term PE multiple that is rare even for mining giants. Curious which forecasts justify that high target? The next part reveals what analysts are betting on for Ivanhoe’s future numbers.

Result: Fair Value of $18.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, lingering operational disruptions or a downturn in copper prices could quickly challenge even the most optimistic outlook for Ivanhoe Mines.

Find out about the key risks to this Ivanhoe Mines narrative.

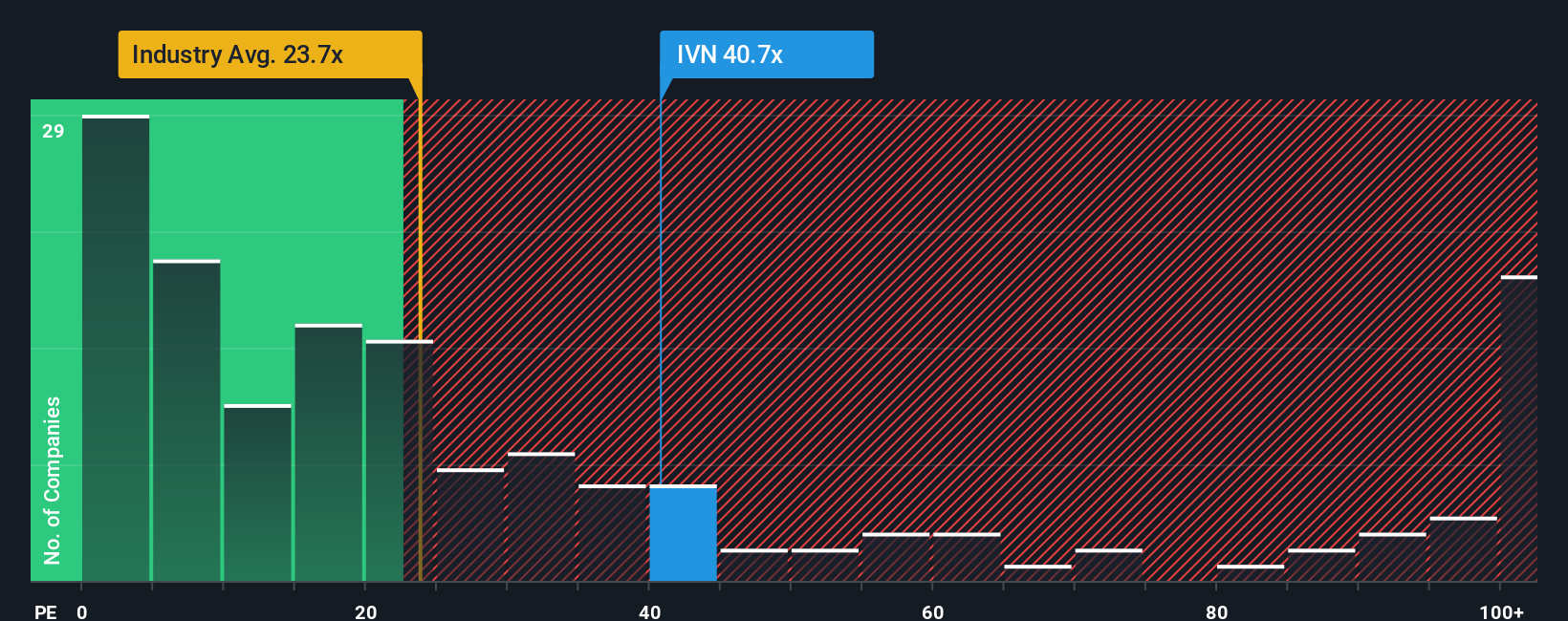

Another View: Price Ratios Point to Caution

Taking a multiples-based approach paints a more expensive picture. Ivanhoe Mines trades at a price-to-earnings ratio of 41.5x, which is significantly higher than both the industry average of 20.5x and its own fair ratio of 30x. This premium signals investor optimism but also adds downside risk if expectations shift. Are current growth forecasts strong enough to justify such a steep valuation premium?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ivanhoe Mines Narrative

If you want to challenge these views or dive into the numbers on your own, you can craft your own take in just a few minutes: Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Ivanhoe Mines.

Looking for More Compelling Investment Ideas?

Chasing your next great investment move? The Simply Wall Street Screener unlocks unique strategies that you might not see anywhere else. Don’t settle for the same old picks when you could find standouts at the cutting edge.

- Pinpoint tomorrow’s tech leaders as you scan these 25 AI penny stocks that are fueling advances in artificial intelligence and automation across industries.

- Grow your income with confidence by tracking these 16 dividend stocks with yields > 3% which offer reliable yields above 3% for steady cash flow potential.

- Get ahead of the next crypto boom by screening these 82 cryptocurrency and blockchain stocks that are driving innovation in decentralized finance and blockchain technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com