GrainCorp (ASX:GNC) Is Down 9.6% After Profits Fall Despite Higher Sales—Has the Bull Case Changed?

- GrainCorp Limited recently reported its full year earnings for the period ended September 30, 2025, with sales rising to A$7,305.7 million from A$6,506.8 million last year, but net income dropping to A$39.9 million from A$61.8 million previously.

- Despite achieving higher sales, the company saw a significant contraction in bottom-line results, reflecting the impact of challenging global market conditions on profitability.

- We'll examine how GrainCorp's weaker profit outcome, despite increased sales, may influence its previously outlined growth narrative and analyst expectations.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

GrainCorp Investment Narrative Recap

At its core, the GrainCorp story is about believing in the company’s ability to deliver reliable earnings amid ongoing swings in agricultural commodity cycles. The most recent earnings update, which featured higher revenue but weaker profit and a share price drop, has brought short-term margin pressures into focus as the most immediate risk, with cost management and margin outlook now even more central to the debate. The catalysts tied to diversification and operational efficiency remain, but the impact of the latest result on these themes is material and will weigh on expectations in the near term. The recent earnings announcement stands out as most relevant, directly highlighting how increased grain sales did not fully offset margin headwinds from softer global prices and supply chain costs. The market’s reaction suggests investors are monitoring not only agricultural output but also GrainCorp’s ability to protect margins through efficiency and diversification, such as broader port operations and innovations in animal nutrition and agri-energy. However, investors should also be mindful that while recent results put margin pressure in the spotlight, the company’s exposure to ongoing global competition and unpredictable crop yields is a risk that could...

Read the full narrative on GrainCorp (it's free!)

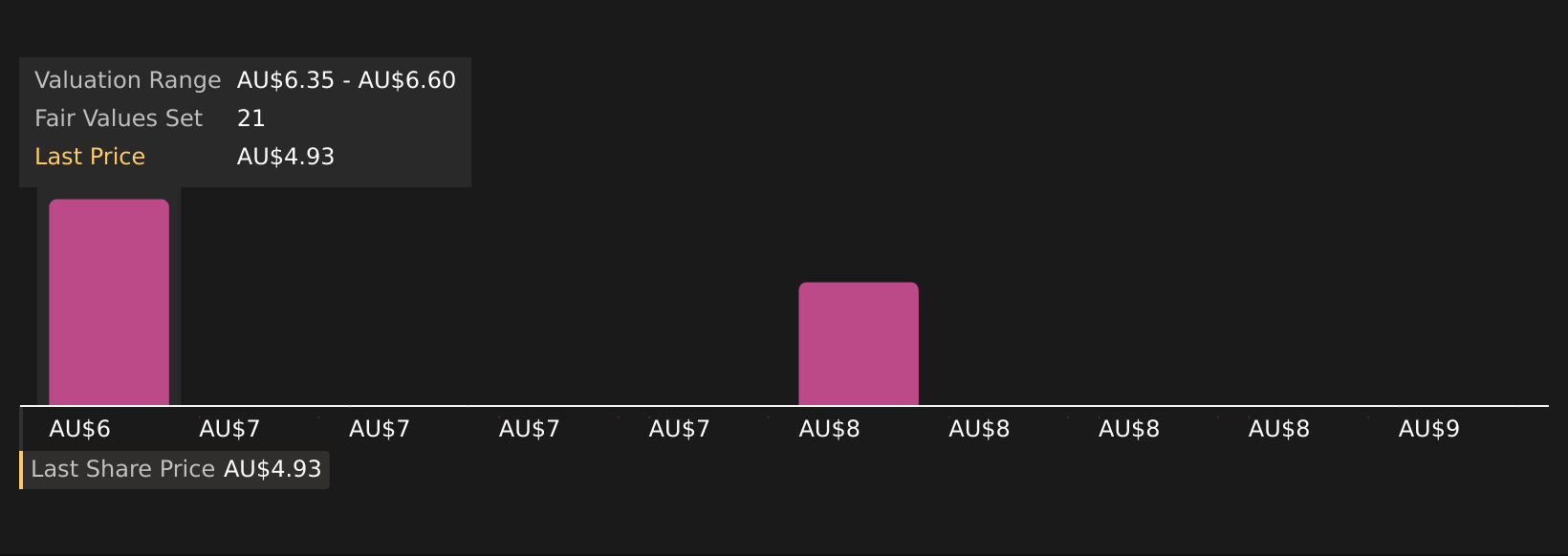

GrainCorp's narrative projects A$6.9 billion revenue and A$112.7 million earnings by 2028. This requires a 1.4% annual revenue decline and a A$42.4 million increase in earnings from A$70.3 million today.

Uncover how GrainCorp's forecasts yield a A$9.21 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community members estimate GrainCorp’s fair value between A$8.93 and A$9.72 per share. With shifting margins now at the forefront, it pays to consider how wider earnings volatility impacts these varied outlooks.

Explore 3 other fair value estimates on GrainCorp - why the stock might be worth just A$8.93!

Build Your Own GrainCorp Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your GrainCorp research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free GrainCorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GrainCorp's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com