Is MercadoLibre Still Attractive After Fintech Expansion and Recent Price Pullback?

- Curious whether MercadoLibre is a bargain or overpriced in today’s market? If you have a keen eye for value, now may be an ideal time to take a closer look.

- Despite a slight pullback of 4.6% over the past week and 5.9% over the last month, MercadoLibre is still up 15.1% year-to-date and has climbed 119.1% in the past three years.

- Recent headlines have highlighted MercadoLibre’s expansion efforts in Brazil along with its ongoing investments in fintech. These developments are fueling excitement among growth-oriented investors. On the other hand, changing risk perceptions around emerging markets and ongoing regulatory developments have also contributed to the short-term price volatility.

- Currently, MercadoLibre scores a 4 out of 6 on our valuation checks, which suggests it appears undervalued across most measures. We will break down these results using different valuation approaches, and there will also be a way to look at valuation that goes beyond the usual metrics.

Find out why MercadoLibre's 8.3% return over the last year is lagging behind its peers.

Approach 1: MercadoLibre Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future cash flows and then discounting those amounts back to today's value. This approach is widely used because it anchors valuation in the actual cash the business is expected to generate over time.

For MercadoLibre, the latest reported Free Cash Flow (FCF) stands at $8.77 Billion. Analyst outlook sees this figure continuing to climb, forecasting $10.75 Billion by the end of 2027. While analysts typically look five years ahead, Simply Wall St extrapolates beyond that and projects MercadoLibre’s FCF will reach $15.66 Billion in 2035. These cash flows are modeled in US Dollars.

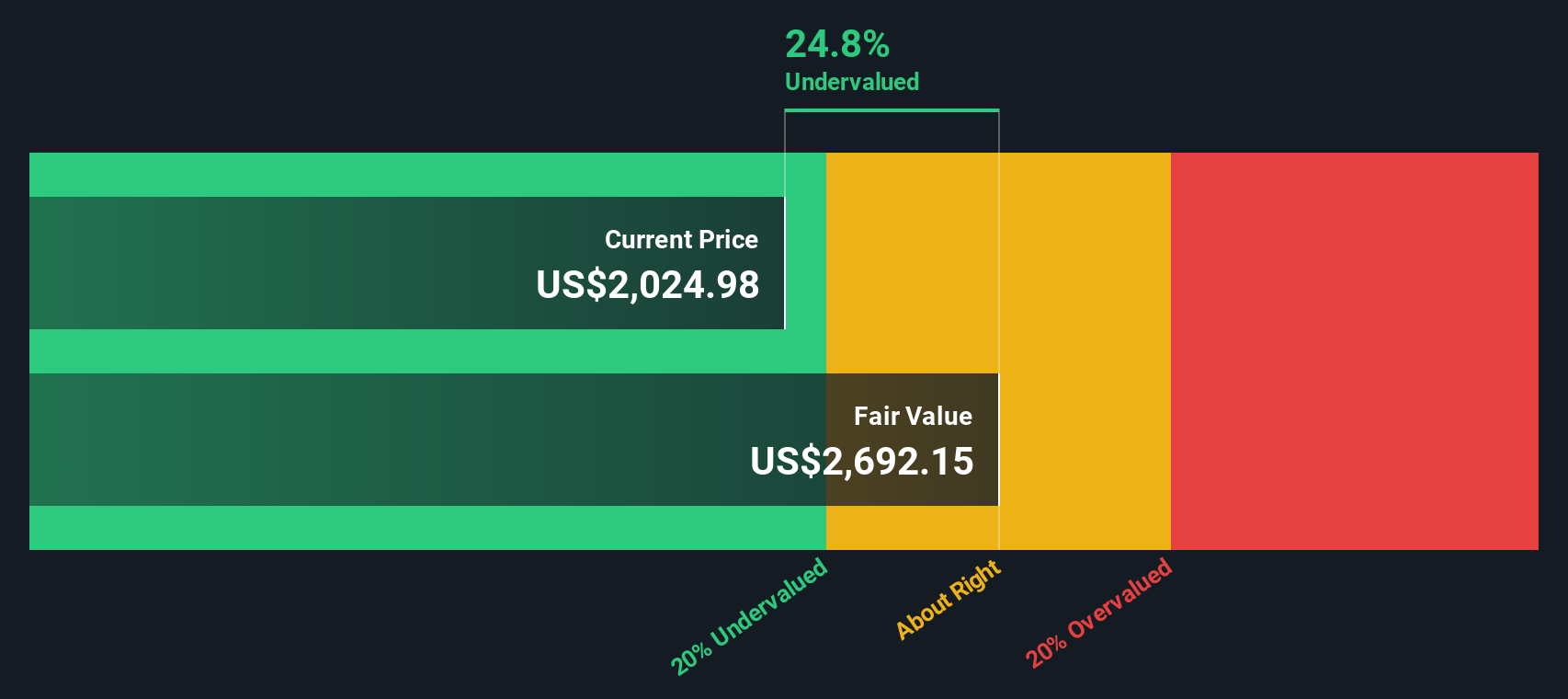

By discounting all estimated future cash flows back to their present value, the DCF model calculates an intrinsic value of $2,886 per share. Compared to MercadoLibre’s recent share price, this results in an implied discount of 29.6%. In practical terms, the stock is currently trading well below what its discounted future cash flows suggest it is worth.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests MercadoLibre is undervalued by 29.6%. Track this in your watchlist or portfolio, or discover 876 more undervalued stocks based on cash flows.

Approach 2: MercadoLibre Price vs Earnings

The Price-to-Earnings (PE) ratio is a commonly used metric for valuing profitable companies because it directly ties a company's stock price to its actual earnings. This makes it especially useful for businesses like MercadoLibre that are generating consistent profits, as it quickly illustrates how much investors are willing to pay for each dollar of earnings today.

The "normal" or "fair" PE ratio for a company is shaped by several factors, most notably the expected future growth of earnings and the risks associated with the business or industry. Higher growth often justifies a higher PE, while greater risk tends to push the ratio down.

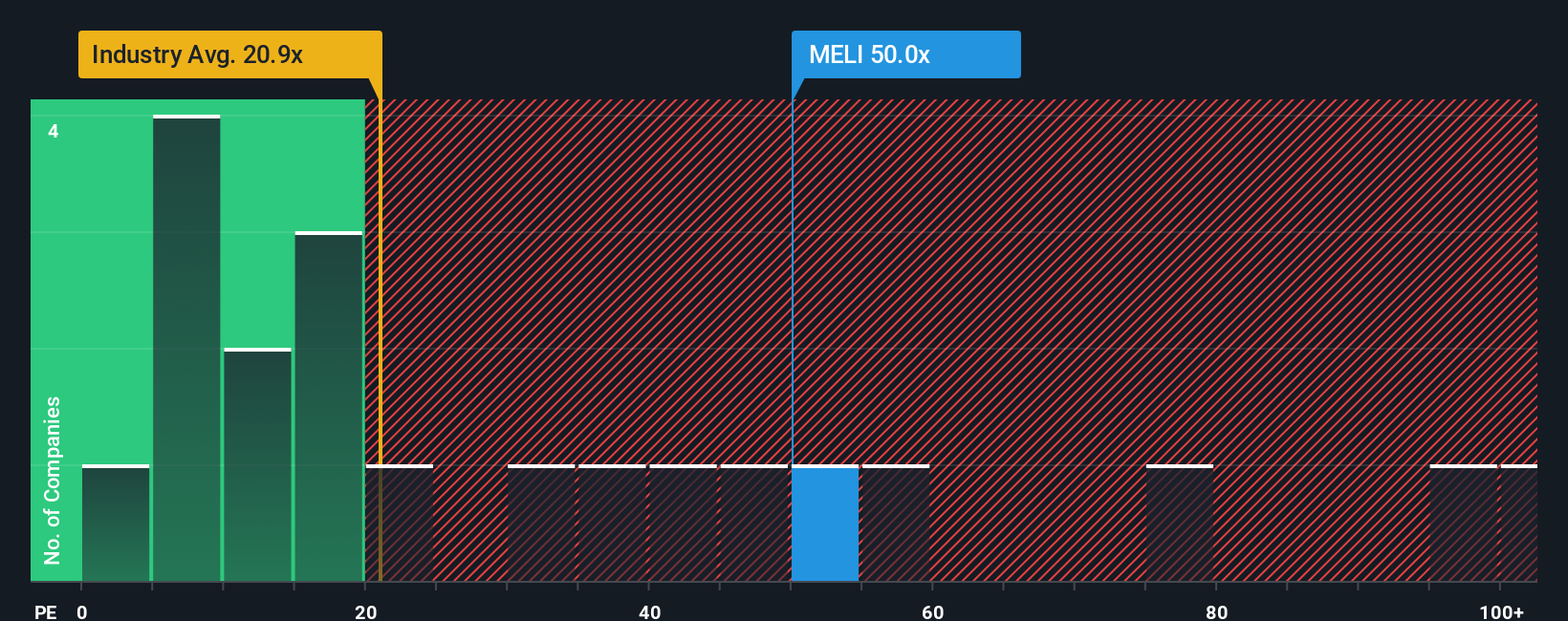

MercadoLibre currently trades at a PE ratio of 49.58x. Comparing this figure, the sector's industry average PE sits much lower at 20.25x, and the average PE for direct peers is 53.48x. This tells us that while MercadoLibre's shares are priced higher than the broader industry, they are in line with their closest competitors in the e-commerce and online marketplace space.

Simply Wall St's proprietary “Fair Ratio” metric goes a step further by factoring in company-specific drivers such as earnings growth, profit margin, risk profile, size, and industry dynamics to suggest what a reasonable PE should be. This approach matters because peer and sector averages can overlook crucial differences in business quality or growth outlook. The Fair Ratio brings all these elements together for a more accurate valuation target.

For MercadoLibre, the Fair Ratio is calculated as 31.71x. When lined up against the current PE of 49.58x, the shares appear more expensive than what would be justified by these underlying fundamentals, even when accounting for the company's impressive growth and market position.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1402 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your MercadoLibre Narrative

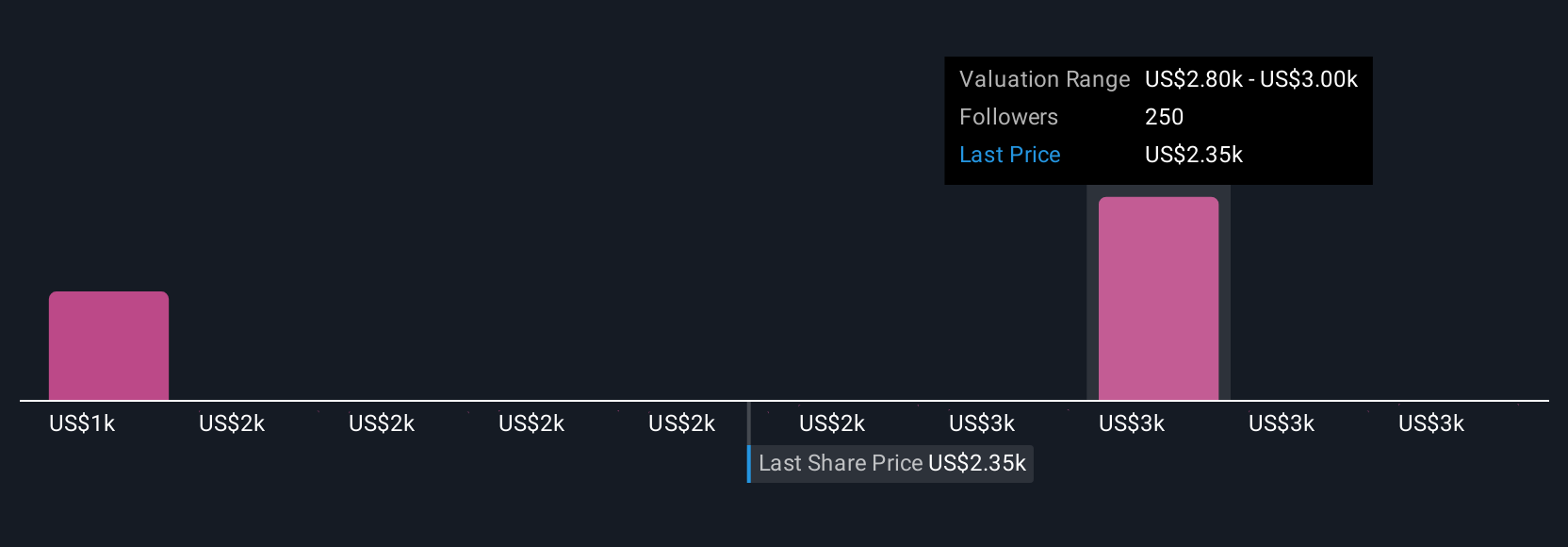

Earlier, we mentioned a more powerful way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, flexible way for you to describe your view of a company's future by connecting its business story to your own forecasts for revenue, earnings, and margins.

Rather than focusing only on standard ratios, Narratives let you put your perspective behind the numbers. This approach explains why you think MercadoLibre will succeed or face challenges and then reveals the implied fair value that follows from your assumptions.

On Simply Wall St's Community page, millions of investors are now accessing Narratives as an easy and intuitive tool that updates automatically whenever fresh news, earnings, or data is released. This means your Narrative stays relevant and actionable in real time, helping you spot opportunities or risks before others do.

With Narratives, you can directly compare your estimated fair value with the current price, giving you a logical, story-driven way to help decide your course of action. For example, some investors believe MercadoLibre will deliver rapid earnings growth and have set price targets as high as $3,500. Others are more cautious, setting targets as low as $2,170 based on concerns about competition and profitability. Narratives help you articulate and test your own thesis so your investment decision always fits your view of the future.

Do you think there's more to the story for MercadoLibre? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com