Dropbox (DBX) Valuation in Focus After Q3 Profit Surge, Raised Guidance, and AI Product Momentum

Dropbox (DBX) caught investors’ attention after reporting third quarter results that showed improved profitability and strong retention rates. The company also raised its full-year 2025 revenue guidance. This updated outlook is fueling fresh discussion around its growth prospects.

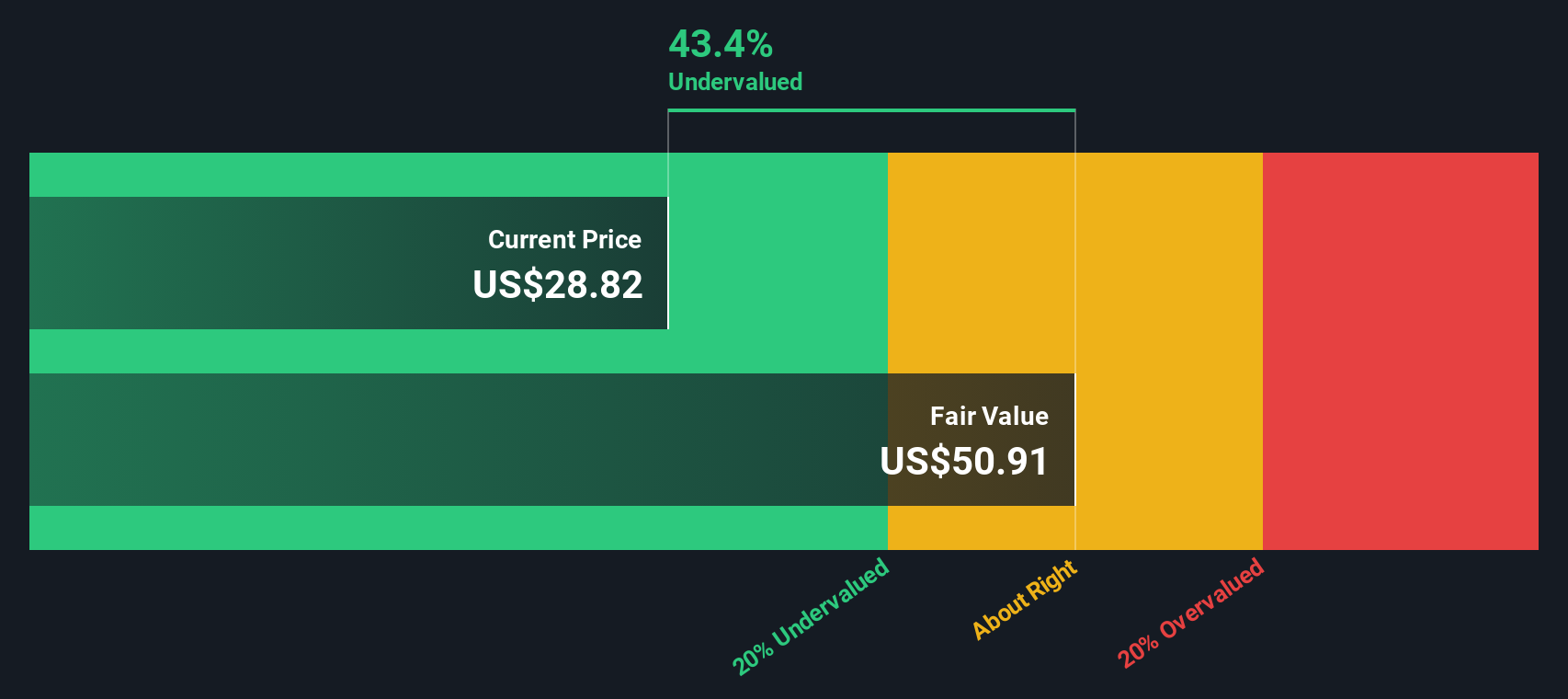

See our latest analysis for Dropbox.

The upbeat quarterly report and new AI-driven product momentum have reignited interest in Dropbox, with the share price gaining over 6% in the past week and a 9% total return for shareholders over the last year. Momentum appears to be building as the market responds to the updated guidance and future growth potential.

If Dropbox’s renewed growth ambitions have you rethinking your strategy, this is a great time to broaden your search and discover fast growing stocks with high insider ownership

With Dropbox lifting its guidance and its shares on the rise, investors are left to ponder whether the current price reflects all these upbeat developments, or if this is an emerging buying opportunity before further growth is recognized.

Most Popular Narrative: 8% Overvalued

The most widely followed narrative points to a fair value below Dropbox’s current share price, noting that analysts see limited upside. This sets the context for a deeper dive into the underlying assumptions shaping market sentiment right now.

The planned expansion and deeper integration of AI-driven productivity tools (Dash), including upcoming self-serve offerings and seamless bundling with Dropbox's existing file sync and share product, position the company to capture higher ARPU and accelerate recurring revenue growth as digital transformation and hybrid work drive demand for intelligent, collaborative cloud platforms.

Curious what’s behind that outlook? One central assumption could flip expectations: the narrative’s take on user-based revenue and profitability. Want the full financial projections and the wild card that could shake up these results? The details might surprise you.

Result: Fair Value of $28.13 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent revenue declines and intensifying competition from larger tech players could quickly turn sentiment and challenge the growth story for Dropbox.

Find out about the key risks to this Dropbox narrative.

Another View: Undervalued According to Our DCF Model

While analyst price targets suggest Dropbox is about 8% overvalued, a look through our DCF model presents a very different picture. The SWS DCF model estimates Dropbox's fair value at $59.29, nearly double the current share price. Does this large gap hint at a hidden opportunity, or is it a sign to dig deeper?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Dropbox Narrative

If you have a different angle or want to review the numbers yourself, you can craft your own Dropbox outlook in just minutes, so why not Do it your way

A great starting point for your Dropbox research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for Your Next Smart Move?

Don’t let opportunity pass you by. Use the Simply Wall Street Screener to pinpoint standout investment ideas beyond Dropbox and strengthen your portfolio with fresh momentum.

- Capture high yields and steady income by checking out these 15 dividend stocks with yields > 3% offering returns above 3 percent in today’s market.

- Seize the edge with these 27 AI penny stocks fueling innovation and reshaping industries through artificial intelligence breakthroughs.

- Accelerate your gains by tapping into these 870 undervalued stocks based on cash flows that are trading below their intrinsic value right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com