It Looks Like Academies Australasia Group Limited's (ASX:AKG) CEO May Expect Their Salary To Be Put Under The Microscope

Key Insights

- Academies Australasia Group will host its Annual General Meeting on 21st of November

- Total pay for CEO Christopher Campbell includes AU$510.0k salary

- The total compensation is similar to the average for the industry

- Academies Australasia Group's EPS declined by 17% over the past three years while total shareholder loss over the past three years was 70%

Shareholders will probably not be too impressed with the underwhelming results at Academies Australasia Group Limited (ASX:AKG) recently. At the upcoming AGM on 21st of November, shareholders can hear from the board including their plans for turning around performance. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. The data we present below explains why we think CEO compensation is not consistent with recent performance.

View our latest analysis for Academies Australasia Group

Comparing Academies Australasia Group Limited's CEO Compensation With The Industry

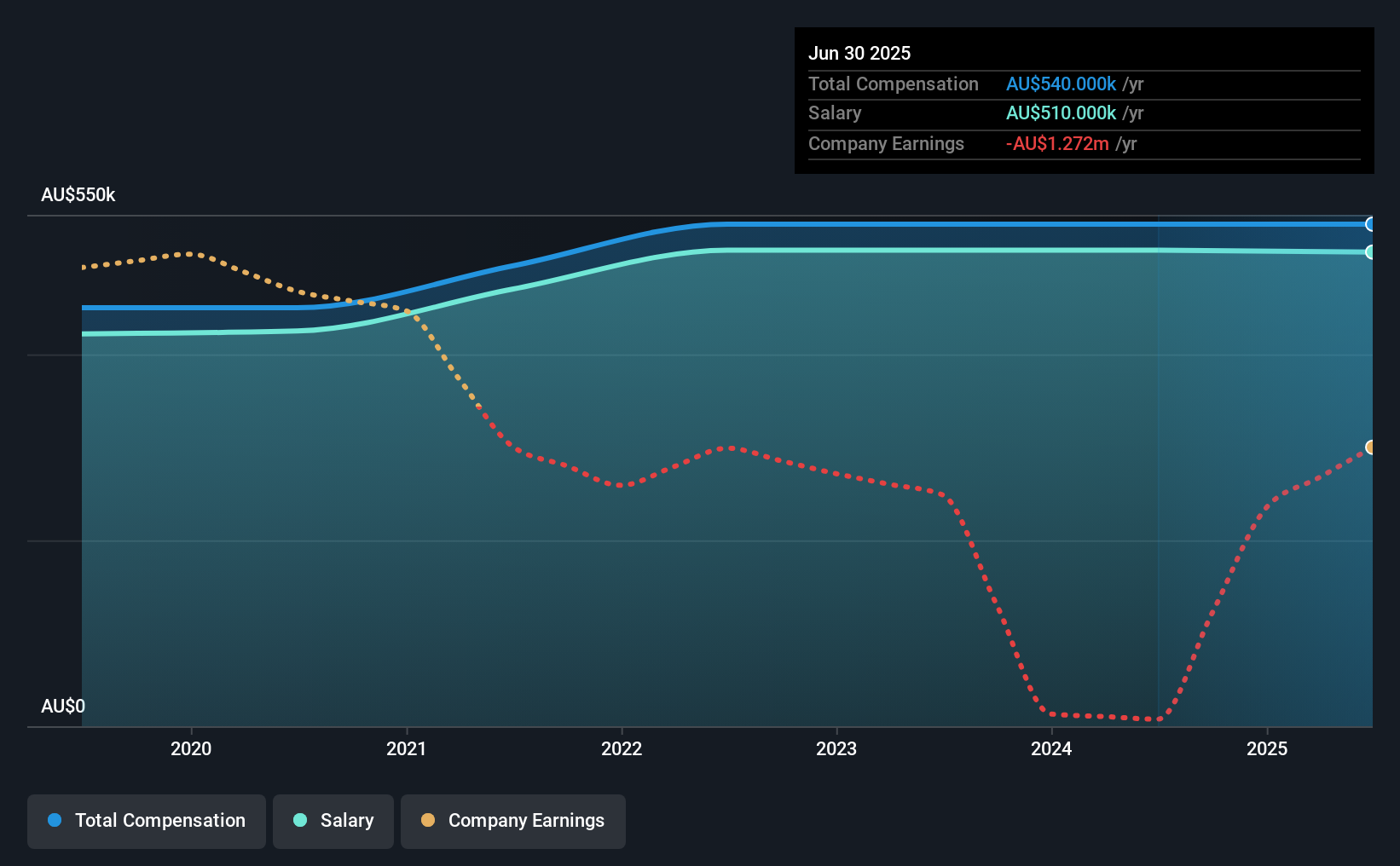

According to our data, Academies Australasia Group Limited has a market capitalization of AU$17m, and paid its CEO total annual compensation worth AU$540k over the year to June 2025. This was the same as last year. We note that the salary portion, which stands at AU$510.0k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Australian Consumer Services industry with market capitalizations under AU$306m, the reported median total CEO compensation was AU$541k. This suggests that Academies Australasia Group remunerates its CEO largely in line with the industry average. Moreover, Christopher Campbell also holds AU$2.7m worth of Academies Australasia Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | AU$510k | AU$512k | 94% |

| Other | AU$30k | AU$28k | 6% |

| Total Compensation | AU$540k | AU$540k | 100% |

Talking in terms of the industry, salary represented approximately 65% of total compensation out of all the companies we analyzed, while other remuneration made up 35% of the pie. It's interesting to note that Academies Australasia Group pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Academies Australasia Group Limited's Growth Numbers

Over the last three years, Academies Australasia Group Limited has shrunk its earnings per share by 17% per year. Its revenue is up 1.4% over the last year.

The decline in EPS is a bit concerning. The fairly low revenue growth fails to impress given that the EPS is down. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Academies Australasia Group Limited Been A Good Investment?

With a total shareholder return of -70% over three years, Academies Australasia Group Limited shareholders would by and large be disappointed. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 3 warning signs for Academies Australasia Group (of which 2 are potentially serious!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.