Banca Mediolanum (BIT:BMED) Lifts Net Profits as Net Interest Income Slips—Is Its Diversification Sustainable?

- Banca Mediolanum S.p.A. recently reported its third quarter and nine-month 2025 earnings, showing third quarter net interest income of €214.9 million and net income of €248.8 million, both up from a year earlier, while nine-month net income reached €726 million.

- An interesting insight is that despite lower year-to-date net interest income, the bank managed to post higher net profits, highlighting the impact of non-interest income sources and operating efficiency.

- We'll now explore how the company's ability to raise nine-month net income despite lower net interest income shapes its investment narrative.

We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Banca Mediolanum Investment Narrative Recap

To be a shareholder in Banca Mediolanum, one needs to believe in the company’s capacity to maintain resilient earnings through diversification, especially when interest margins are under pressure. The recent earnings update underlines this, as higher net profits were achieved despite lower net interest income, suggesting that the most important near-term catalysts, fee income growth and operational efficiency, remain intact, while the principal risk remains margin pressure from regulatory and competitive changes. Overall, the latest results provide reassurance but do not materially alter these key factors.

The August 1, 2025 half-year results announcement stands out for its early signal of this same trend: net interest income was already showing a year-on-year dip, but net profits moved higher. This theme, confirmed in the third quarter, strengthens the argument that Banca Mediolanum’s fee-driven business lines and cost control are at center stage for the investment story, reinforcing their role as primary earnings drivers in the absence of significant interest margin tailwinds.

However, despite these positive signals, investors should be aware that regulatory shifts affecting product fee structures...

Read the full narrative on Banca Mediolanum (it's free!)

Banca Mediolanum's outlook anticipates €2.3 billion in revenue and €1.1 billion in earnings by 2028. This scenario reflects a 1.6% annual decline in revenue and no change in earnings from the current €1.1 billion level.

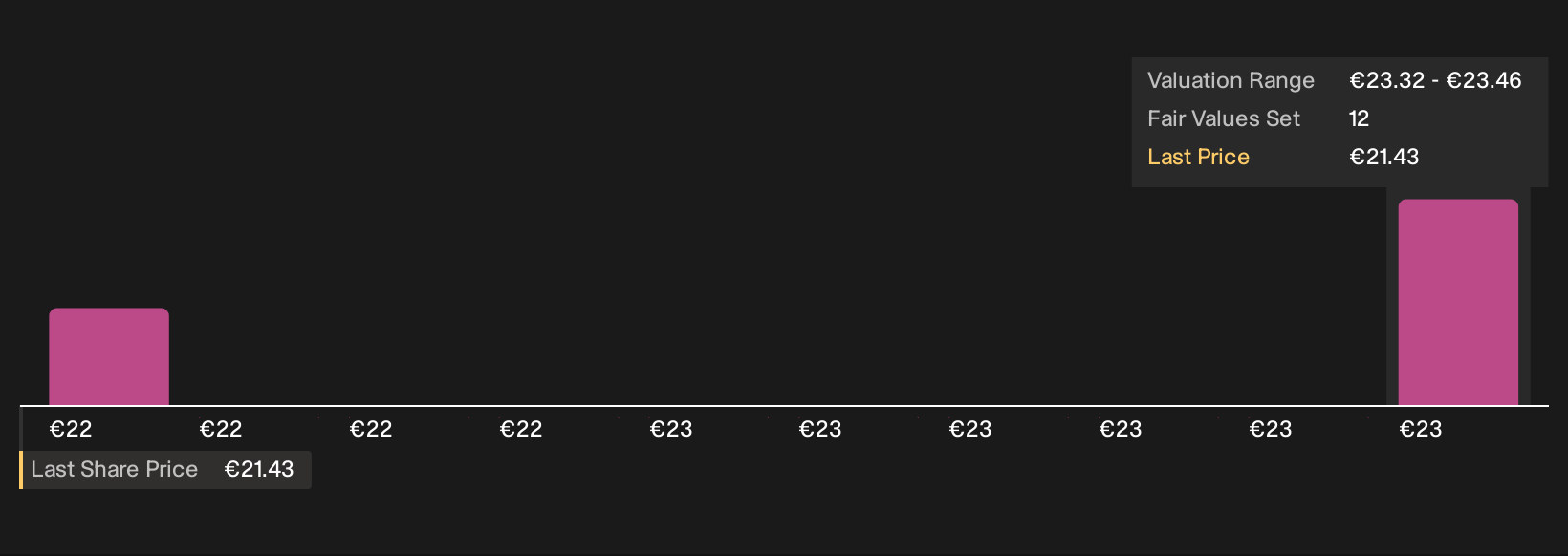

Uncover how Banca Mediolanum's forecasts yield a €18.89 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members produced two fair value estimates for Banca Mediolanum, ranging from €16.39 to €18.89 per share. While many expect resilience from strong fee income, evolving regulation may continue to challenge margin stability, so it pays to explore the range of viewpoints.

Explore 2 other fair value estimates on Banca Mediolanum - why the stock might be worth 14% less than the current price!

Build Your Own Banca Mediolanum Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Banca Mediolanum research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Banca Mediolanum research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Banca Mediolanum's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com