TrendForce Jibang Consulting: The memory industry's capital expenditure in 2026 is still conservative, with limited support for bitwise output growth

The Zhitong Finance App learned that according to the TrendForce Jibang Consulting survey, as the average sales price of memory (ASP) continues to rise and supplier profits also increase, subsequent capital expenditure for DRAM and NAND Flash will continue to rise, but there is limited support for the growth of bitwise output in 2026. The focus of investment in the DRAM and NAND Flash industries is gradually shifting from simply expanding production capacity to high-value-added products such as process technology upgrades, high-rise stacks, hybrid bonding, and HBM.

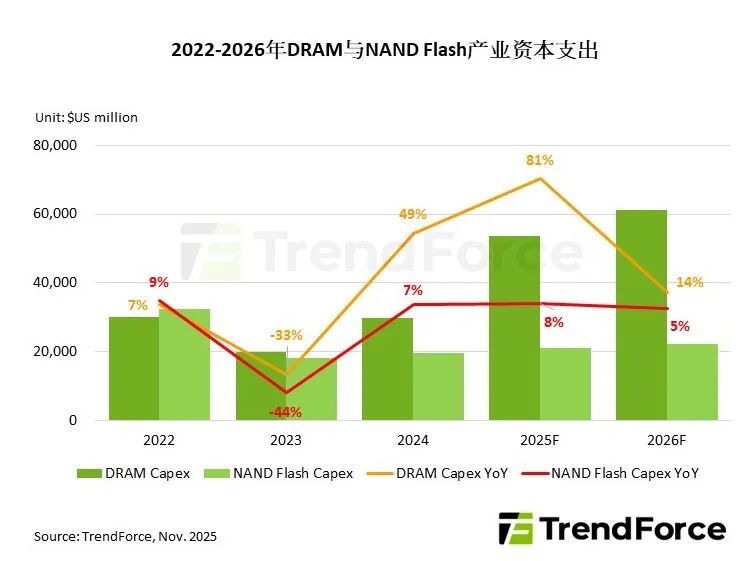

Among them, the DRAM industry's capital expenditure is expected to reach 53.7 billion US dollars in 2025, and is expected to grow further to 61.3 billion US dollars in 2026, with an annual growth rate of 14%. In the NAND Flash section, capital expenditure is expected to be US$21.1 billion in 2025, and is expected to increase slightly to US$22.2 billion in 2026, an annual increase of about 5%.

Among DRAM suppliers, Micron (Micron Technology) is considered the most active manufacturer. Its capital expenditure is expected to reach US$13.5 billion in 2026, an annual increase of 23%, mainly focusing on 1 gamma process penetration and TSV equipment construction. SK hynix (SK hynix) has also increased significantly. It is expected to be 20.5 billion US dollars in 2026, an annual increase of 17% to cope with the expansion of M15x's HBM4 production capacity. Samsung (Samsung) expects to invest $20 billion, an annual increase of 11%, to penetrate HBM's 1C process and slightly increase P4L wafer production capacity.

TrendForce Jibang Consulting pointed out that there is currently insufficient supply of clean room space. Examining the production capacity space of all DRAM suppliers, only Samsung and SK hynix still have opportunities to slightly expand production lines, while Micron will need to wait for its new US ID1 plant to be completed, and production will not be possible until 2027 at the earliest, so any subsequent capital expenditure will contribute very little to the 2026 bit output.

Among NAND Flash suppliers, Kioxia/SanDisk (Kioxia/SanDisk) is considered the most active manufacturer to expand production capacity to consolidate its position because it does not have a DRAM business. Kioxia/SanDisk is expected to invest US$4.5 billion, an annual increase of 41%, to accelerate BiCS8 production and invest in BiCS9 R&D. Micron's 2026 goal is to slightly increase NAND Flash production capacity and focus on the G9 process and Enterprise SSD business, and the capital expenditure is expected to increase by 63% per year. In contrast, Samsung and SK Hynix/Solidigm (think) will reduce or limit NAND Flash capital expenditure, giving priority to shifting investments to the HBM and DRAM sectors.

According to TrendForce Jibang Consulting's analysis, the current explosion in demand in the NAND Flash industry is mainly driven by the rapid rise in AI demand for storage capacity and cloud service provider (CSP) order transfers due to insufficient HDD supply. This phenomenon is a structural shortage rather than a brief period of market fluctuation.

However, the industry has experienced many boom cycles in the past few years, causing some manufacturers to be conservative in terms of capital expenditure and production expansion strategies. As capital expenditure in 2026 focuses on process upgrades and the introduction of hybrid-bonding rather than expanding production, it will lead to limited supply increases. TrendForce believes that the shortage of supply in the NAND Flash market is expected to continue throughout 2026.