Top UK Dividend Stocks For November 2025

As the FTSE 100 index faces challenges amid weak trade data from China and global economic uncertainties, investors are keeping a close eye on market trends and potential opportunities. In such fluctuating conditions, dividend stocks can offer a measure of stability and income, making them an attractive option for those looking to navigate the current market landscape.

Top 10 Dividend Stocks In The United Kingdom

| Name | Dividend Yield | Dividend Rating |

| Treatt (LSE:TET) | 3.70% | ★★★★★☆ |

| Seplat Energy (LSE:SEPL) | 6.97% | ★★★★★☆ |

| Pets at Home Group (LSE:PETS) | 6.19% | ★★★★★★ |

| OSB Group (LSE:OSB) | 6.07% | ★★★★★☆ |

| NWF Group (AIM:NWF) | 5.04% | ★★★★★☆ |

| MONY Group (LSE:MONY) | 6.35% | ★★★★★★ |

| Macfarlane Group (LSE:MACF) | 5.53% | ★★★★★☆ |

| Keller Group (LSE:KLR) | 3.49% | ★★★★★☆ |

| Hargreaves Services (AIM:HSP) | 5.57% | ★★★★★☆ |

| 4imprint Group (LSE:FOUR) | 4.48% | ★★★★★☆ |

Click here to see the full list of 54 stocks from our Top UK Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

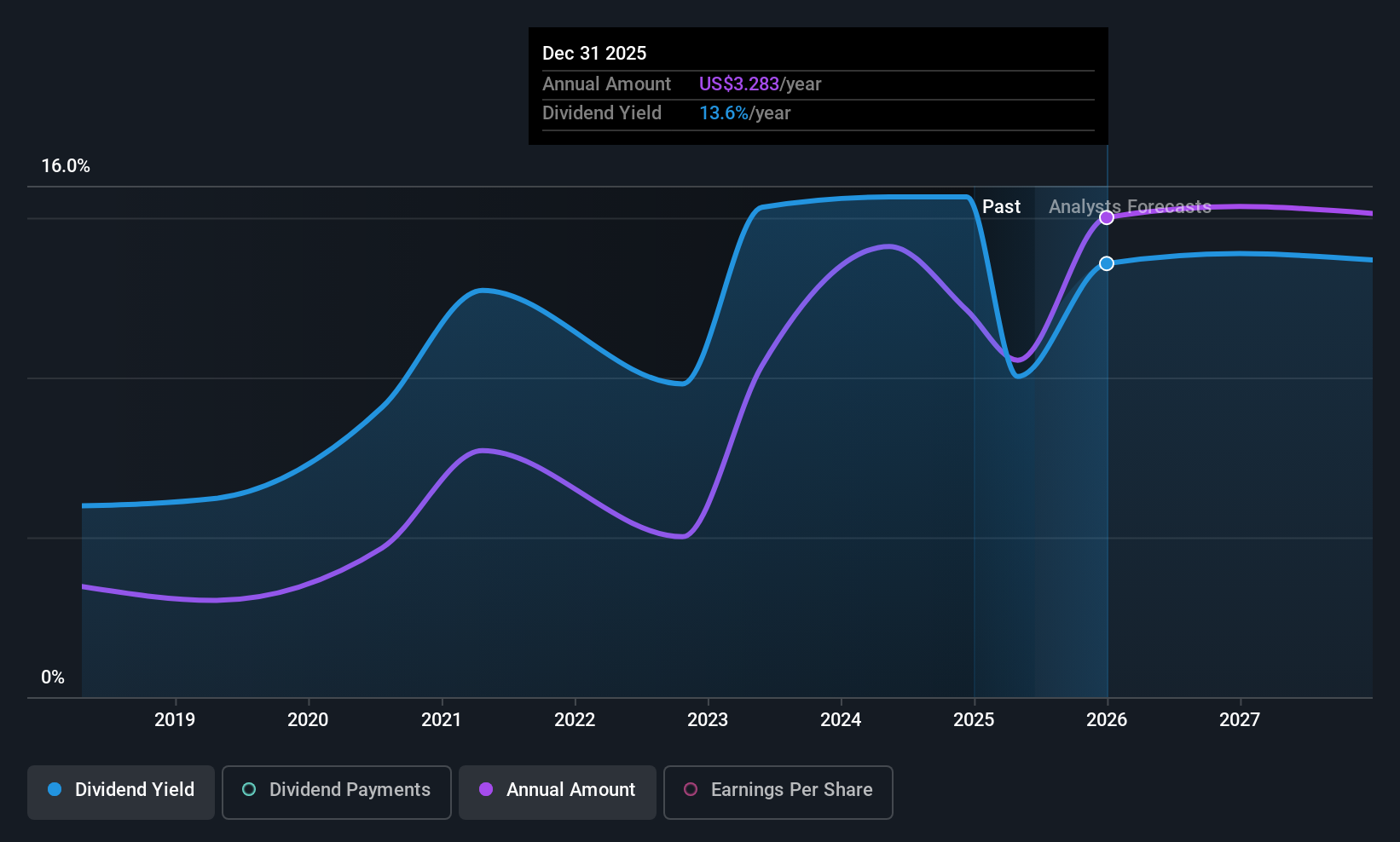

Halyk Bank of Kazakhstan (LSE:HSBK)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Halyk Bank of Kazakhstan Joint Stock Company, along with its subsidiaries, offers corporate and retail banking services mainly in Kazakhstan, Kyrgyzstan, Georgia, and Uzbekistan with a market cap of $7.01 billion.

Operations: Halyk Bank of Kazakhstan's revenue segments include Retail Banking (KZT 210.22 billion), Corporate Banking (KZT 861.97 billion), Investment Banking (KZT 272.71 billion), and Small and Medium Enterprises (SME) Banking (KZT 195.87 billion).

Dividend Yield: 6.2%

Halyk Bank of Kazakhstan offers a substantial dividend yield, ranking in the top 25% among UK market dividend payers. Its dividends are well covered by earnings, with a current payout ratio of 30.2%, projected to rise to 50.2% in three years. However, the bank's dividend history has been volatile over the past decade. Recent announcements include a $50 million share buyback program aimed at optimizing capital structure and affirming dividends for 2024 at KZT 21 per share.

- Click here to discover the nuances of Halyk Bank of Kazakhstan with our detailed analytical dividend report.

- According our valuation report, there's an indication that Halyk Bank of Kazakhstan's share price might be on the cheaper side.

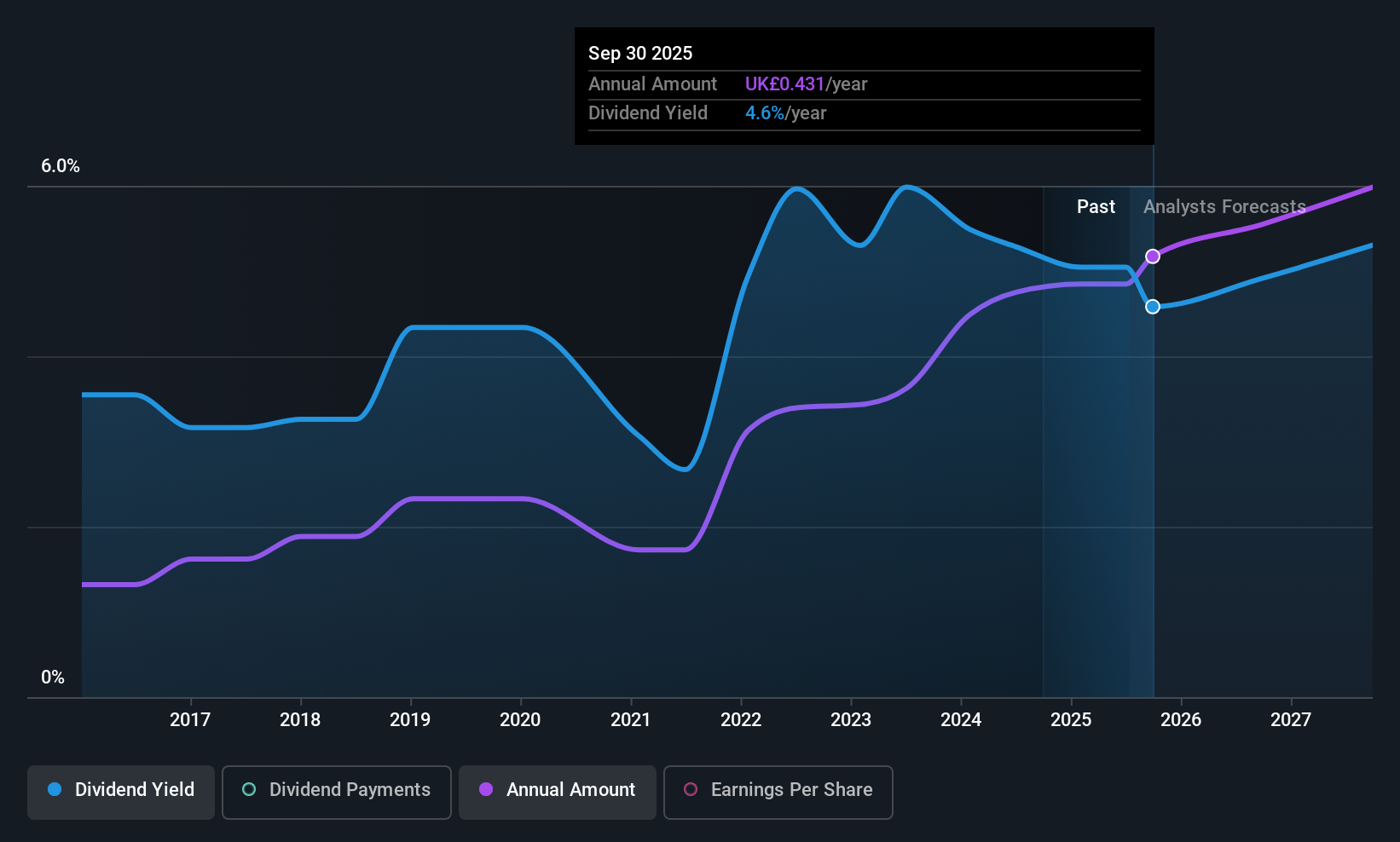

Lloyds Banking Group (LSE:LLOY)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Lloyds Banking Group plc, along with its subsidiaries, offers a variety of banking and financial services in the UK and internationally, with a market cap of approximately £55.79 billion.

Operations: Lloyds Banking Group plc generates its revenue through a diverse array of banking and financial services offered both domestically in the UK and on an international scale.

Dividend Yield: 3.5%

Lloyds Banking Group's dividend yield is relatively low compared to the top UK dividend payers, with a current payout ratio of 58% and forecasted improvement to 37.8% in three years, indicating sustainable coverage. Despite a history of unreliable and volatile dividends, recent moves such as share buybacks totaling £1.4 billion suggest efforts to enhance shareholder value. The bank's earnings guidance for 2025 anticipates net interest income of GBP 13.6 billion, slightly above prior expectations.

- Navigate through the intricacies of Lloyds Banking Group with our comprehensive dividend report here.

- Insights from our recent valuation report point to the potential overvaluation of Lloyds Banking Group shares in the market.

Paragon Banking Group (LSE:PAG)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Paragon Banking Group PLC offers financial products and services in the United Kingdom with a market cap of £1.54 billion.

Operations: Paragon Banking Group PLC's revenue is derived from two main segments: Mortgage Lending, contributing £278.30 million, and Commercial Lending, accounting for £106.80 million.

Dividend Yield: 4.9%

Paragon Banking Group's dividend payments are well covered by earnings and cash flows, with payout ratios of 40.6% and 17.6% respectively, indicating sustainability despite a history of volatility over the past decade. While its dividend yield of 4.93% is below the top UK payers, Paragon trades at a significant discount to its estimated fair value and peers, suggesting potential value for investors seeking both income and growth opportunities in the sector.

- Click to explore a detailed breakdown of our findings in Paragon Banking Group's dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Paragon Banking Group shares in the market.

Seize The Opportunity

- Reveal the 54 hidden gems among our Top UK Dividend Stocks screener with a single click here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com