Are ADM Shares Priced Fairly After Recent 8% Drop and Supply Chain Partnerships?

- Ever wondered if Archer-Daniels-Midland is trading at a bargain, or if the current price already reflects its fair value? You are not alone. Right now might be the perfect time to dig in.

- The stock climbed 11.5% year-to-date and 11.2% in the past year. However, just in the last month, shares dipped by 8.0% and are off 6.8% in the past week. That combination raises fresh questions about growth prospects and shifting risk perceptions.

- In recent weeks, headlines have focused on Archer-Daniels-Midland’s new sustainability initiatives and supply chain partnerships. Both topics are fueling conversation about the company's long-term potential. However, investor sentiment remains mixed as broader markets react to changing commodity prices and ongoing policy debates impacting agribusiness.

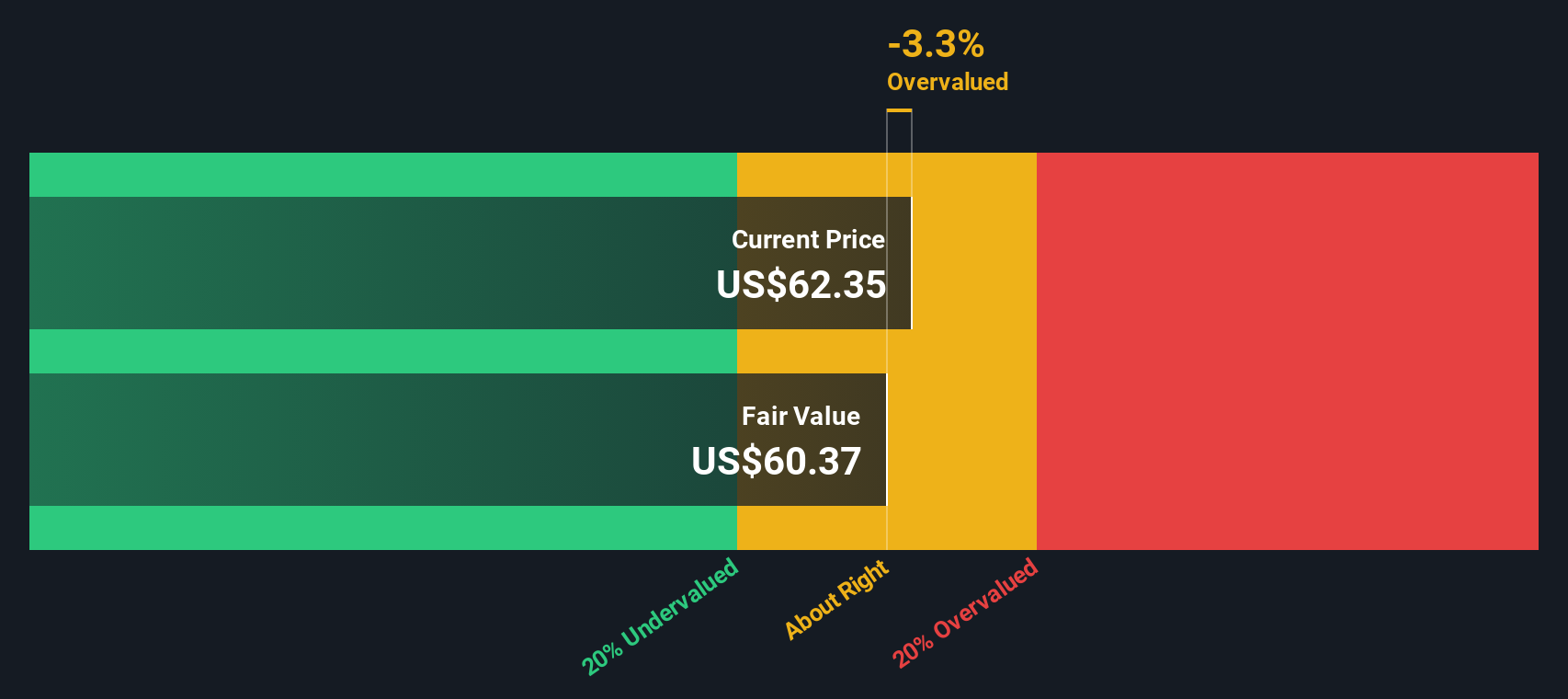

- On our six-point valuation checklist, Archer-Daniels-Midland scores a 2 out of 6. This suggests there are some signs of undervaluation but also some red flags. We will break down what goes into this score, compare the valuation approaches investors use, and reveal a smarter way to gauge if ADM is genuinely mispriced at the end of this article.

Archer-Daniels-Midland scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Archer-Daniels-Midland Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them back to today's value. This provides a sense of what the company is truly worth based on its long-term cash-generating ability.

For Archer-Daniels-Midland, the DCF model uses a "2 Stage Free Cash Flow to Equity" approach. The most recent reported Free Cash Flow is $4.71 Billion. Analyst estimates project a decrease to $2.18 Billion in 2027, with further cash flows for the next decade extrapolated using internal models. Cash flow projections show a gradual decline over ten years, indicating more modest growth or even contraction in the future.

The DCF model calculates an intrinsic value of $48.81 per share. Relative to the current market price, this implies the stock is trading at a 14.7% premium, suggesting it is overvalued based on projected cash flows.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Archer-Daniels-Midland may be overvalued by 14.7%. Discover 865 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Archer-Daniels-Midland Price vs Earnings

For profitable companies like Archer-Daniels-Midland, the Price-to-Earnings (PE) ratio is a widely used valuation measure. The PE ratio tells investors how much they are paying for each dollar of a company’s earnings, making it especially relevant when the business generates consistent profits.

Growth expectations and company-specific risks play a major role in shaping what is considered a “normal” or fair PE ratio. A higher growth outlook or lower risk profile often justifies a higher PE, while slower growth or greater risk should result in a lower PE.

Currently, Archer-Daniels-Midland trades at a PE ratio of 22.6x. This is broadly in line with the peer average of 23.7x and noticeably above the food industry average of 18.5x. At first glance, this places ADM in the mid to high range compared to its industry and competitors, possibly reflecting higher earnings quality or more resilient growth prospects.

Instead of relying purely on simple peer or industry comparisons, Simply Wall St uses a proprietary “Fair Ratio” methodology. This metric blends together data on earnings growth, risk factors, profit margins, industry specifics, and company size to create a more tailored benchmark. For Archer-Daniels-Midland, the Fair PE Ratio is calculated at 23.0x. By comparing this to the current PE, investors get a clearer view of whether the shares are priced attractively for the company’s specific profile, not just the sector in general.

Since Archer-Daniels-Midland’s current PE ratio of 22.6x is very close to the Fair Ratio of 23.0x, the shares appear to be priced about right based on earnings fundamentals.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1401 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Archer-Daniels-Midland Narrative

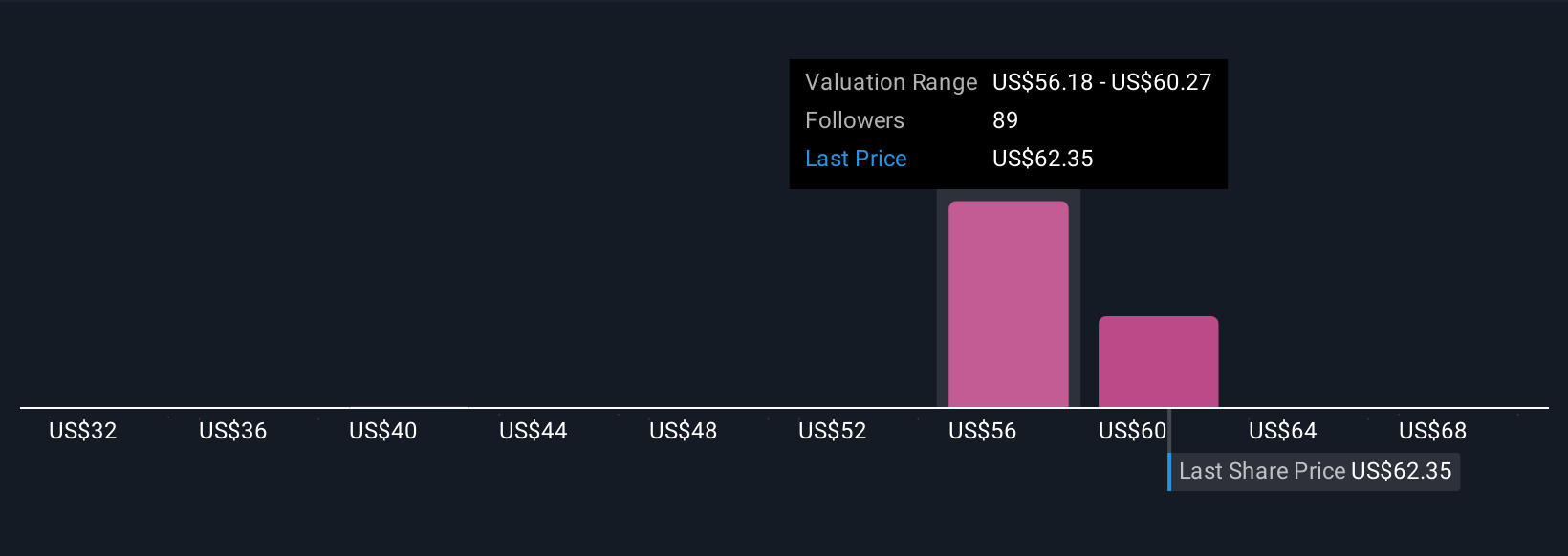

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is a simple, story-driven approach where you combine your perspective on a company’s future, such as your assumptions for revenue growth, profit margins, and risk factors, with the numbers, creating your own forecast and fair value estimate. Narratives translate the story you believe about Archer-Daniels-Midland into actual financial forecasts and automatically connect those to a fair value, so you can see if the current price makes sense.

This approach is both easy and accessible, with millions of investors already using Narratives on the Simply Wall St platform, especially within the Community page. Narratives empower you to make clearer decisions about when to buy or sell by showing how your Fair Value compares to the current Price, and they refresh in real time as new news or earnings are released. For example, one investor may build a bullish Narrative, assuming policy support leads to stronger margins and targets a fair value over $70. Another, more cautious investor might expect continued volatility and estimate fair value as low as $54. Narratives help you invest your way, grounded in your own assumptions and the latest information.

Do you think there's more to the story for Archer-Daniels-Midland? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com