Is Charter (CHTR) Relying on Buybacks to Offset Broadband Growth Challenges?

- In the past week, Charter Communications reported third-quarter 2025 results showing sales of US$13.67 billion and net income of US$1.14 billion, both slightly lower than a year ago, and revealed ongoing large-scale share repurchases. Following these results, a prominent analyst downgrade cited concerns about missed expectations in broadband subscriber growth and adjusted EBITDA.

- The scale of Charter's share buybacks highlights ongoing confidence from management, despite increasing market focus on the challenges in broadband customer growth.

- We will examine how the quarterly earnings shortfall, especially in broadband subscribers, challenges the company's broader investment narrative going forward.

We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Charter Communications Investment Narrative Recap

Charter Communications’ investment case hinges on belief in its ability to grow broadband and mobile connectivity while efficiently managing costs and capital returns. The disappointing Q3 results, especially weak broadband subscriber growth, place significant pressure on this core narrative, making execution in broadband retention and acquisition the most important near-term catalyst, and ongoing subscriber losses one of the most critical risks, notably, the latest results materially affect both areas.

Charter’s ongoing large-scale share buybacks are especially relevant now, as they underscore management’s intention to return capital despite recent earnings and broadband pressures. With over US$2.09 billion spent repurchasing shares in the third quarter alone, these actions are a focal point for current and potential shareholders who weigh capital efficiency against fundamental business growth.

Yet, with subscriber growth showing clear signs of strain, there remains a significant consideration for investors that...

Read the full narrative on Charter Communications (it's free!)

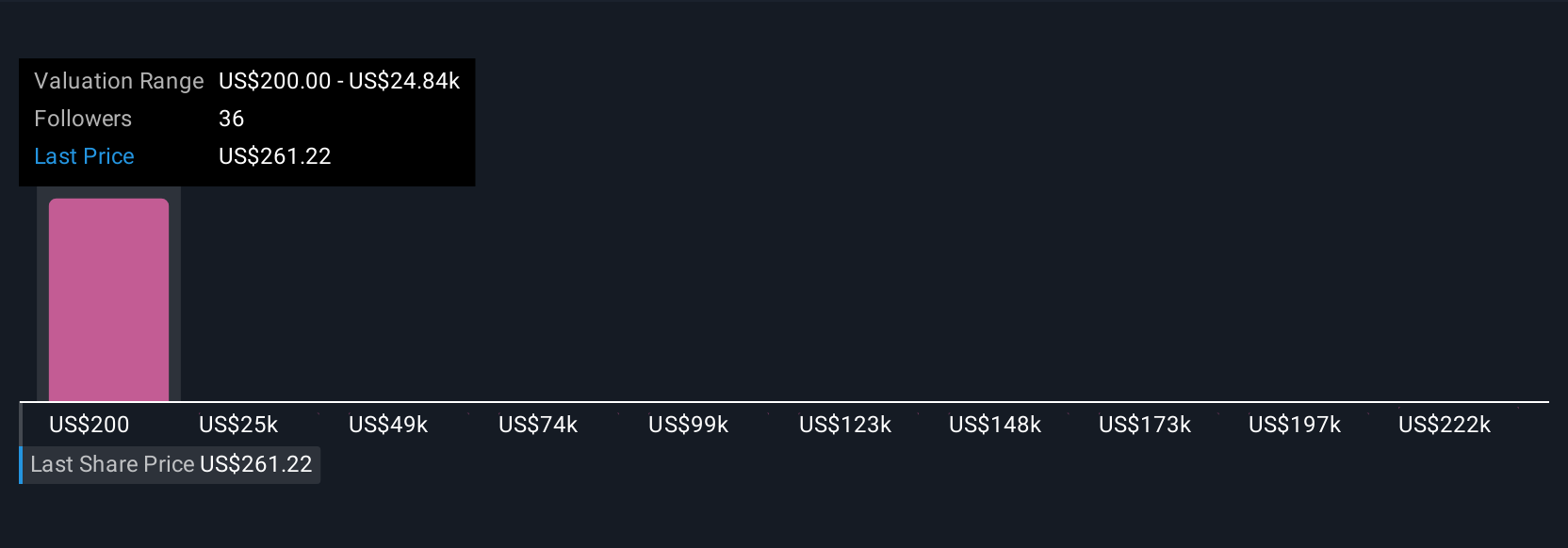

Charter Communications' outlook anticipates $56.8 billion in revenue and $6.0 billion in earnings by 2028. This scenario assumes an annual revenue decline of 0.9% and an earnings increase of $0.7 billion from the current $5.3 billion.

Uncover how Charter Communications' forecasts yield a $314.94 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Fair value estimates from four members of the Simply Wall St Community range from US$314.94 to US$865.07. Many participants highlight stalled broadband growth as a key concern that could weigh on Charter’s future potential, compare competing perspectives to see which risks matter most to you.

Explore 4 other fair value estimates on Charter Communications - why the stock might be worth over 4x more than the current price!

Build Your Own Charter Communications Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Charter Communications research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Charter Communications research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Charter Communications' overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com