AtriCure (ATRC): Valuation Insights After Strong Q3 Growth, Narrowed Losses and Upbeat Guidance

AtriCure (ATRC) shares were in focus after the company reported a surge in revenue for the third quarter of 2025 and sharply narrowed its net loss. The company also raised its full-year revenue guidance.

See our latest analysis for AtriCure.

Strong growth and reduced losses have caught investors’ attention lately, yet AtriCure’s momentum has faced headwinds, with a 1-day share price return of 1.75% following earnings but a 1-year total shareholder return of -14.4%. Recent medical trial news and raised revenue guidance may help shift sentiment. However, the long-term track record remains mixed.

If this upswing in healthcare innovation interests you, consider exploring the latest opportunities through our curated list of promising companies: See the full list for free.

With AtriCure posting double-digit revenue growth and a sharply smaller net loss, the stock still trades well below consensus price targets. Is this a buying opportunity as future growth potential takes shape, or is all the good news already reflected in the share price?

Most Popular Narrative: 35.9% Undervalued

Compared to its recent $32.05 closing price, the narrative’s fair value target of $50 suggests a potential opportunity, making a bold case for long-term upside.

Expanding access to international markets, including robust sales growth in Europe and Asia, and continued investment in global commercialization initiatives are broadening geographic diversification and building recurring revenue streams. These developments position AtriCure to benefit from rising healthcare demand and spending worldwide.

Curious what future milestones analysts see shaping this valuation? The narrative draws on surprising growth assumptions, margin improvements, and a profitability flip few saw coming. Unpack the numbers, challenge the boldest expectations, and discover what fuels this premium fair value—only in the full narrative.

Result: Fair Value of $50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, intense competition and slower international adoption could challenge AtriCure’s growth story and pose risks to the optimistic outlook for future profits.

Find out about the key risks to this AtriCure narrative.

Another View: Discounted Cash Flow Reality Check

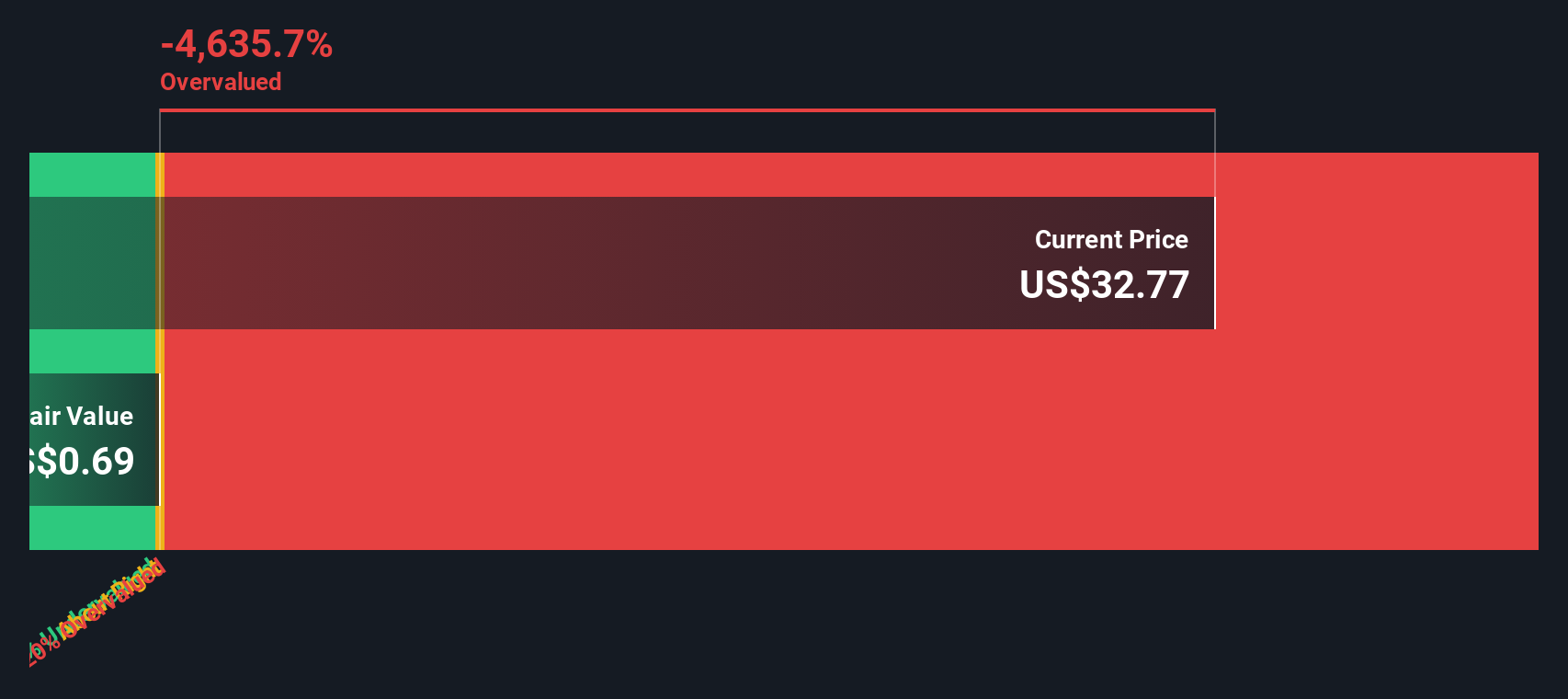

While the consensus price target signals upside, our SWS DCF model suggests a far more conservative view, placing fair value at just $0.78 per share, which is dramatically below the current trading price. This big gap highlights how sensitive long-term forecasts can be to changing company fortunes. Could expectations be overreaching, or is the market betting big on future success?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AtriCure for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own AtriCure Narrative

If you think the story should be told differently or want to dig into the numbers on your own terms, build your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding AtriCure.

Looking for more investment ideas?

Don’t settle for just one opportunity when you could spot tomorrow’s winners today. Use the Simply Wall Street Screener to gain a real edge.

- Spot undervalued gems set for a rebound and seize the moment with these 874 undervalued stocks based on cash flows before others catch on.

- Power up your portfolio by targeting forward-thinking businesses with explosive potential through these 25 AI penny stocks.

- Lock in reliable income by zeroing in on companies delivering generous yields using these 16 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com