Does JPMorgan Chase’s 30.9% Rally Signal a Rare Opportunity After Strong Consumer Spending News?

- Ever wondered whether JPMorgan Chase is trading at a fair price or if there is untapped value hidden in those share prices? You are in good company, because that is what we are about to explore.

- The stock has been on a notable run, climbing 1.0% in the past week, up 3.3% over the last month, and surging an impressive 30.9% year-to-date.

- Recent headlines around strong consumer spending and renewed investor confidence in the banking sector are fueling optimism. News of robust loan growth and strategic investments by JPMorgan are resonating with the market, helping explain the impressive price momentum.

- Right now, JPMorgan Chase scores just 1 out of 6 on our valuation checks, suggesting pockets of undervaluation but also possible caution. Let us break down those valuation methods and, later on, dive into an even more insightful approach to finding true value.

JPMorgan Chase scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: JPMorgan Chase Excess Returns Analysis

The Excess Returns valuation model assesses how much value JPMorgan Chase is creating above its cost of equity, focusing on the returns generated on invested capital over time. Simply put, this approach shows the difference between what the company earns versus what it needs to pay shareholders for using their money.

For JPMorgan Chase, the model considers several key inputs:

- Book Value: $124.96 per share

- Stable EPS: $22.49 per share (Source: Weighted future Return on Equity estimates from 13 analysts.)

- Cost of Equity: $11.11 per share

- Excess Return: $11.38 per share

- Average Return on Equity: 16.63%

- Stable Book Value: $135.23 per share (Source: Weighted future Book Value estimates from 13 analysts.)

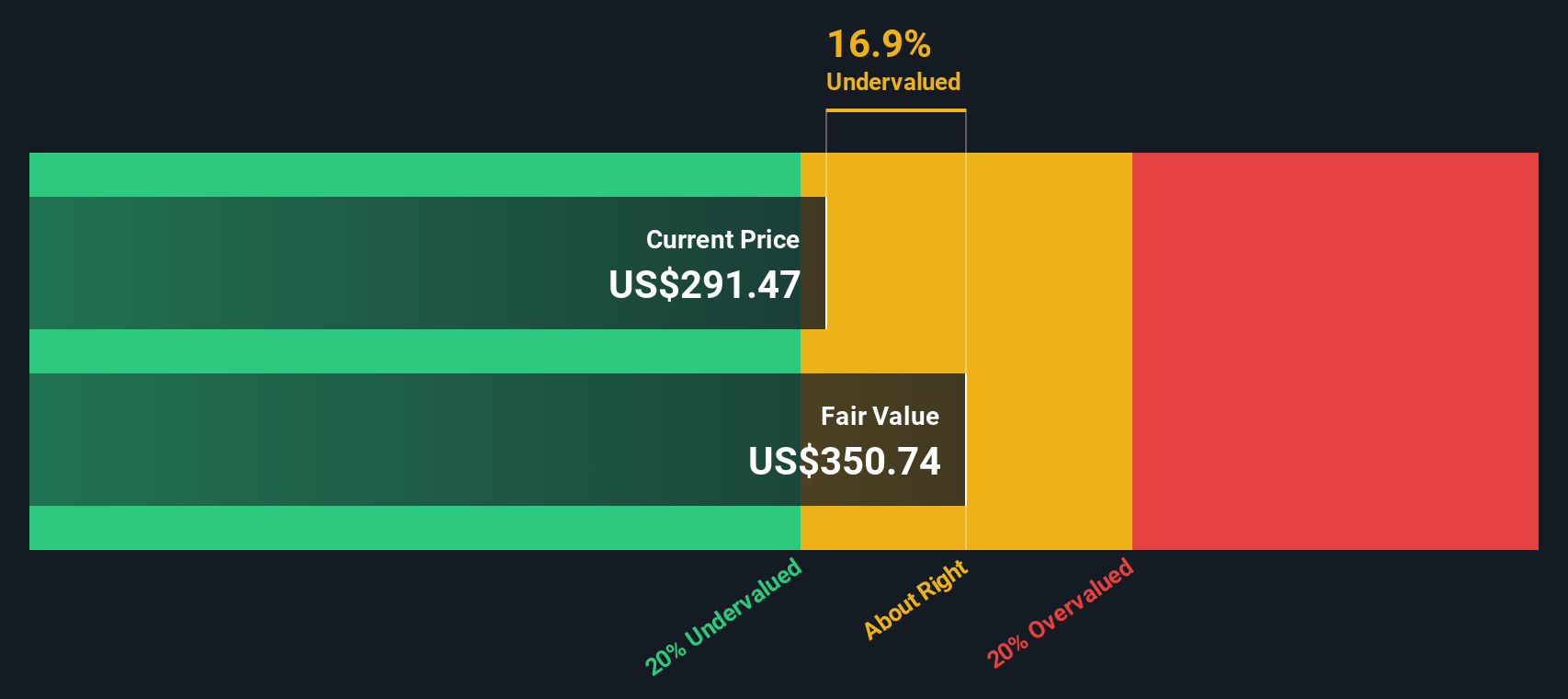

Based on these metrics, the Excess Returns model produces an estimated intrinsic value for JPMorgan Chase that is about 13.9% higher than its current trading price. This suggests the stock is undervalued according to this method and presents a buffer that could reward investors if the performance outlined above continues.

Result: UNDERVALUED

Our Excess Returns analysis suggests JPMorgan Chase is undervalued by 13.9%. Track this in your watchlist or portfolio, or discover 870 more undervalued stocks based on cash flows.

Approach 2: JPMorgan Chase Price vs Earnings

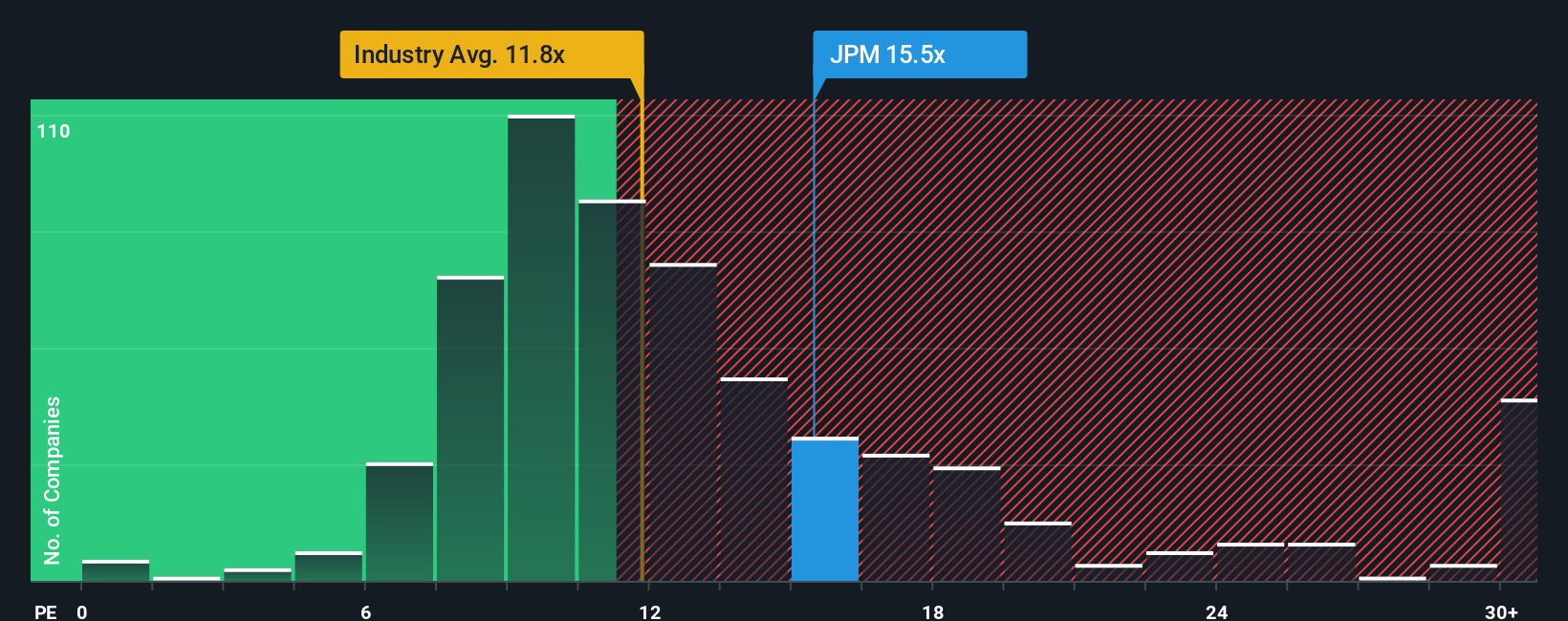

Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like JPMorgan Chase because it connects the market price of a stock to its earnings power. For banks, which typically have more stable earnings than companies in other industries, the PE ratio offers investors a straightforward way to assess if they are paying a reasonable amount for each dollar of profit.

The "right" PE ratio for a company depends on several factors, including expectations for future earnings growth and the overall risk profile. Companies with higher growth prospects or lower risk typically command higher PE ratios. The reverse is true for slower-growing or riskier firms.

JPMorgan Chase is currently trading at a PE ratio of 15.1x. For context, the average PE ratio of its industry peers is 12.8x, and the overall banks industry sits at 11.1x. This means JPMorgan is priced at a premium to both its immediate peers and the broader sector, reflecting perhaps its scale, stability, or recent momentum.

However, Simply Wall St’s proprietary "Fair Ratio" for JPMorgan Chase is 13.9x. The Fair Ratio is designed to give a more tailored benchmark by factoring in not just sector averages but also the company’s specific growth prospects, profit margins, risk factors, and market capitalization. This approach provides a smarter yardstick for valuation than simply comparing to peers because it aligns more closely with what investors should reasonably expect, given JPMorgan’s own strengths and risks.

Comparing the Fair Ratio (13.9x) with the current PE (15.1x), JPMorgan Chase is trading slightly above its fair value estimate, suggesting the stock is a bit overvalued by this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1396 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your JPMorgan Chase Narrative

Earlier, we mentioned there is an even better way to understand valuation. Let us introduce you to Narratives.

A Narrative is your personal investment story. It is a simple, intuitive way to tie your expectations about a company’s future to financial forecasts and ultimately a fair value estimate.

Rather than only looking at past performance or comparing simple ratios, Narratives ask you to state your perspective on how JPMorgan Chase will grow, what its earnings and margins might be, and what all that means for the share price.

Narratives turn these beliefs into numbers, linking the company’s story to projected revenue, profit, and future multiples, so you can see a calculated fair value and confidently compare it to today’s price.

Best of all, Narratives are easy to create and track for free on Simply Wall St’s Community page, where millions of investors share their views in real time.

As new news or earnings reports emerge, Narratives update dynamically so your investment thesis always stays current.

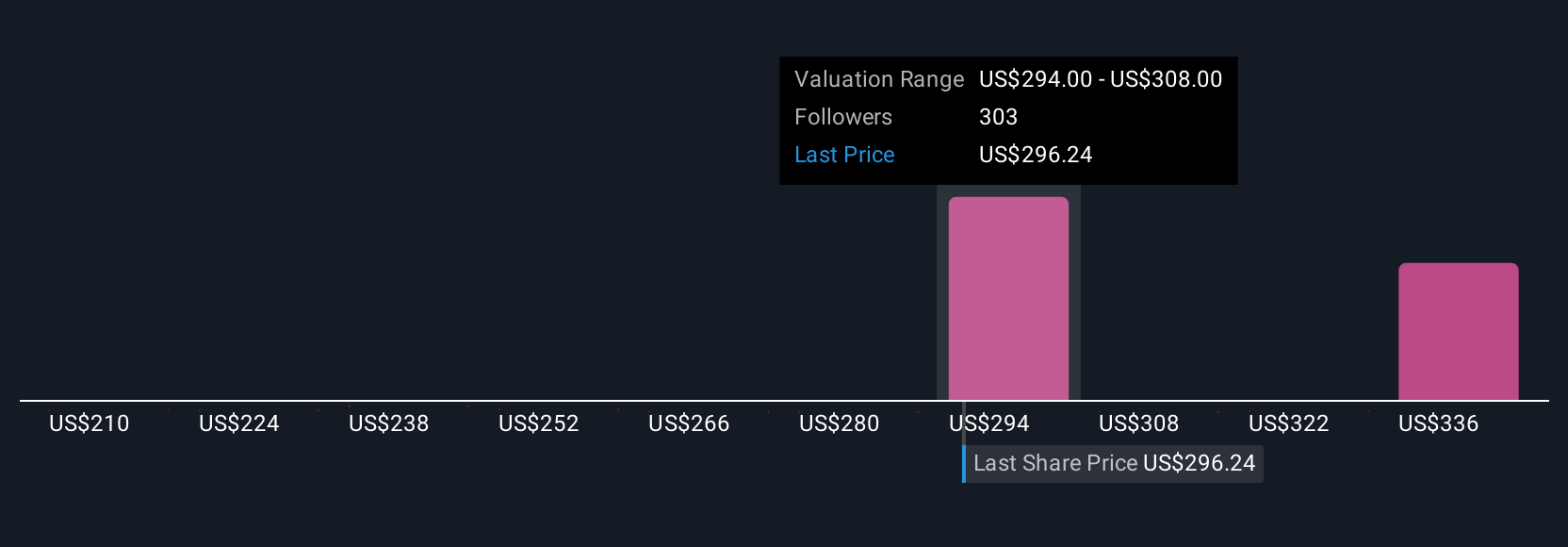

For example, one investor with a bullish Narrative sees JPMorgan reaching $350 per share based on rapid digital banking growth. Another with a more cautious view thinks $235 is more realistic if margins shrink and credit risks increase.

With Narratives, you have the tools to make smarter, story-driven investment decisions and know exactly when the stock fits your own view of "fair value."

For JPMorgan Chase, however, we'll make it really easy for you with previews of two leading JPMorgan Chase Narratives:

Fair Value: $327.70

Undervalued by 4.1%

Forecast Revenue Growth: 6.1%

- Strong growth projected in wealth management, payments, and digital banking, with technology investments driving fee revenue and margins.

- JPMorgan is expected to see sustained resilience and competitive gains due to diversified business expansion and innovation in digital finance.

- Analyst consensus price target is $306.17, only 2.7% above current price, suggesting the stock is fairly priced based on robust but stable near-term growth forecasts.

Fair Value: $247.02

Overvalued by 27.3%

Forecast Revenue Growth: 4.1%

- Rising credit loss allowances and increasing expenses are seen as dragging on future margins and profitability.

- Anticipated rate cuts and a cautious investment banking outlook could constrain growth in net interest and advisory revenue.

- Bearish analysts expect earnings to contract and that the current share price reflects market optimism not justified by the more challenging outlook.

Do you think there's more to the story for JPMorgan Chase? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com