Pony AI (PONY): Evaluating Valuation Risks and Opportunities After Recent Share Price Declines

Pony AI (PONY) shares have come under pressure recently, dropping 5% in the past day and falling 40% for the month. Investors are taking note of these declines and considering what factors may be driving sentiment.

See our latest analysis for Pony AI.

Pony AI’s share price return has been especially volatile lately, capped by a sharp 1-month decline of 40% that overshadows a more modest decrease over the past quarter. Momentum is clearly fading as investors reassess risk and growth prospects. The company is navigating a challenging stretch of news and sentiment.

If you’re on the lookout for interesting shifts in the tech and AI sector, it’s a perfect time to discover See the full list for free.

With shares trading well below analyst targets, but recent financial data reflecting both rapid revenue growth and sustained losses, the question remains for investors: is Pony AI undervalued at these levels, or is the market already factoring in the company’s future trajectory?

Price-to-Book Ratio of 7.1x: Is It Justified?

Pony AI's shares currently trade at a price-to-book (P/B) ratio of 7.1x, which stands out as significantly higher than both the US software industry average and its direct peer group. At a last close of $14.04, investors are paying a hefty premium relative to Pony AI's net assets.

The price-to-book ratio compares a company's market value to its book value, offering a quick way to gauge whether the stock is valued cheaply or expensively on an asset basis. For asset-light, high-growth sectors like software, a higher multiple can be justified by rapid expansion or future potential. However, it signals market optimism that may not be shared by fundamentals.

Pony AI's 7.1x price-to-book ratio is nearly double the industry average of 3.7x and is also more expensive than its peer group average of 5.2x. This substantial gap underlines the market's higher expectations or a premium placed on Pony AI over its software industry counterparts.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book Ratio of 7.1x (OVERVALUED)

However, sustained net losses and ongoing share price volatility remain key risks that could rapidly shift sentiment around Pony AI’s premium valuation.

Find out about the key risks to this Pony AI narrative.

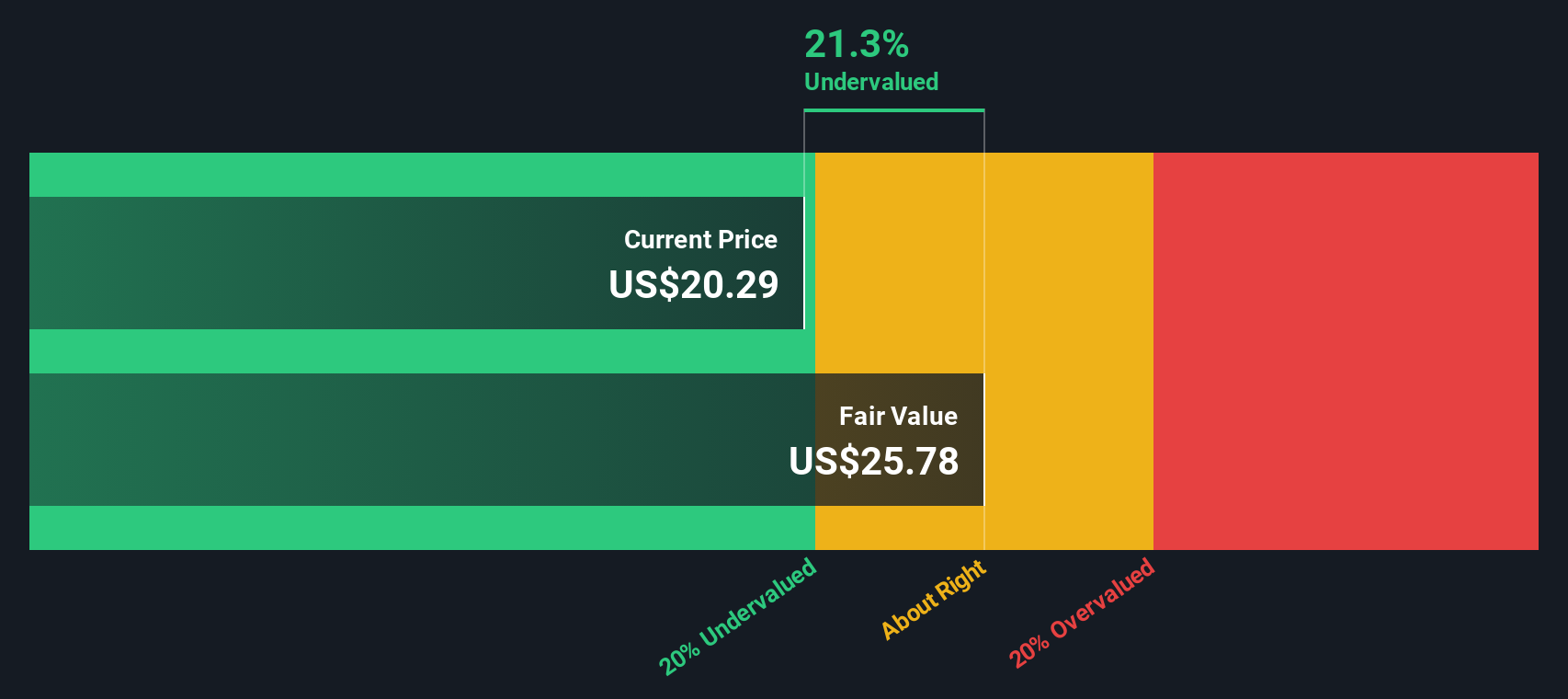

Another View: SWS DCF Model Suggests Undervaluation

While Pony AI appears expensive compared to peers on its price-to-book ratio, our DCF model takes a different approach. Based on projected cash flows, the SWS DCF model estimates a fair value of $21.74 per share, which is about 35% higher than the current price. Is the market missing something, or is this optimism unwarranted?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Pony AI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Pony AI Narrative

If you have your own perspective or want to dig deeper into the numbers, it only takes a few minutes to build and share your own viewpoint. Do it your way

A great starting point for your Pony AI research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Ready to uncover your next big opportunity? Don’t just watch from the sidelines. The Simply Wall Street Screener brings new strategies and standout stocks right to your fingertips.

- Maximize your returns by targeting high-yield sectors. Check out these 16 dividend stocks with yields > 3% offering consistently strong payouts.

- Take advantage of growth in groundbreaking medical innovation and see which leaders are emerging in AI-enhanced healthcare through these 32 healthcare AI stocks.

- Spot the trendsetters in digital assets and blockchain by tapping into these 82 cryptocurrency and blockchain stocks shaping the future of finance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com