Why Ivanhoe Mines (TSX:IVN) Is Down 7.4% After Mixed Quarterly and Year-to-Date Earnings Results

- Ivanhoe Mines reported third quarter 2025 results, with sales of US$129.4 million and net income dropping to US$33.06 million year-over-year, while nine-month net income rose to US$206.87 million from US$128.79 million in the previous period.

- This mixed performance highlights a sharp contrast between weaker quarterly results and improved year-to-date profitability for Ivanhoe Mines.

- We'll now examine how this combination of lower quarterly earnings but stronger nine-month income could impact Ivanhoe Mines' investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Ivanhoe Mines Investment Narrative Recap

To own shares of Ivanhoe Mines, an investor needs to believe in the long-term upside from ongoing expansion projects, increasing copper and zinc production, and the company’s ability to manage operational setbacks. The latest quarterly results did not materially change the key short-term catalyst: the drive to restore and grow output at Kamoa-Kakula after the May 2025 seismic event. However, the biggest risk remains the operational uncertainty and potential for further production disruptions that could pressure earnings in the near term.

Among recent announcements, Ivanhoe Mines reaffirmed its annual production guidance in early October, despite ongoing mine dewatering efforts and earlier disruptions. This update is directly tied to the core catalyst of operational recovery and expansion, giving investors a clearer sense of management’s confidence in achieving full-scale output across flagship assets. Yet, as production volumes rebound and new capacity is added, the effects of unit cost pressures and ore grade changes remain crucial to monitor.

In contrast, one ongoing vulnerability that investors should be aware of is the risk of additional operational disruptions, especially if dewatering takes longer or future seismic events...

Read the full narrative on Ivanhoe Mines (it's free!)

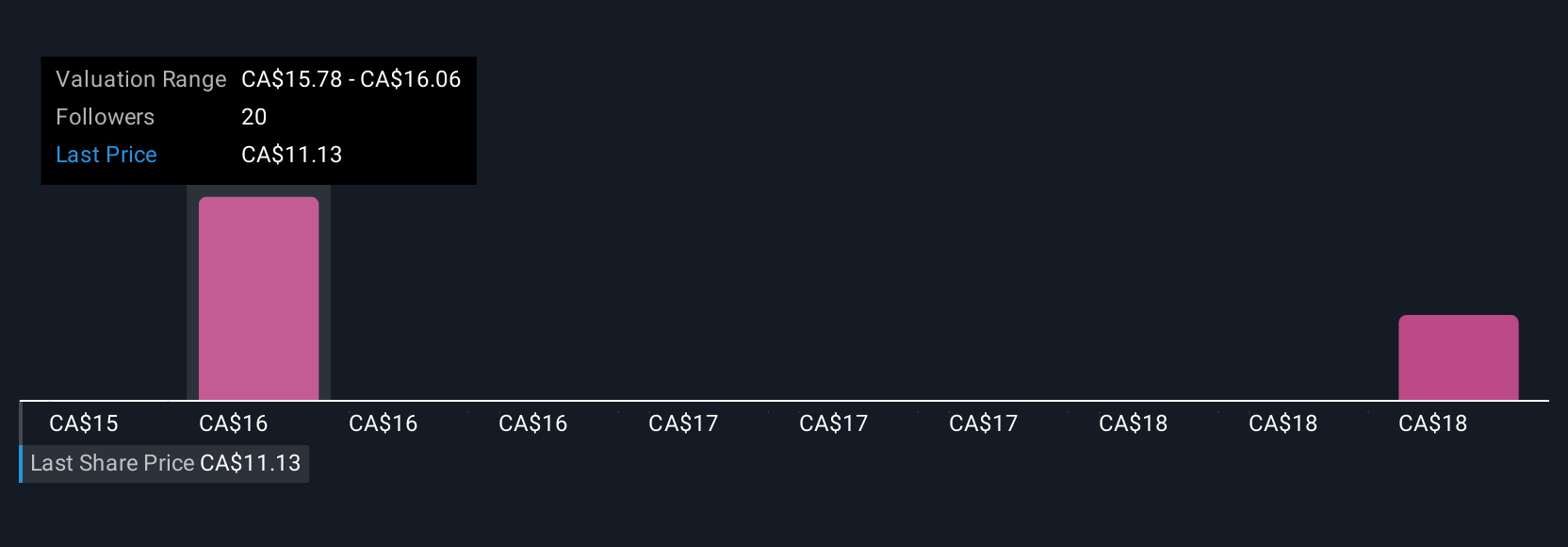

Ivanhoe Mines' narrative projects $1.1 billion revenue and $805.9 million earnings by 2028. This requires 73.9% yearly revenue growth and a $414.8 million earnings increase from $391.1 million currently.

Uncover how Ivanhoe Mines' forecasts yield a CA$18.43 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community estimate Ivanhoe Mines’ fair value between CA$12.01 and CA$20.66 per share. Operational setbacks, as seen in recent earnings, highlight why market participants can hold sharply different outlooks on both short-term profitability and longer-term performance, consider reviewing several of these viewpoints before forming your own conclusion.

Explore 3 other fair value estimates on Ivanhoe Mines - why the stock might be worth 8% less than the current price!

Build Your Own Ivanhoe Mines Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ivanhoe Mines research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Ivanhoe Mines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ivanhoe Mines' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com