Has Volvo’s Electric Truck Strategy Created a New Opportunity for Investors in 2025?

- Wondering if AB Volvo is a hidden value opportunity or just riding a cycle? You are not alone, especially with many investors eager to know how the stock stacks up today.

- While the share price has slipped by 0.3% over the last week and is down 1.7% over the past year, the bigger picture is strong with nearly 98% returns over five years and a 64% gain in just three years.

- Recent attention in the capital goods sector, especially around supply chain resilience and sustainability initiatives, has fueled conversations about Volvo's market strength. Notably, discussions about Volvo’s strategic investments in electric truck development have added both excitement and optimism to the mix.

- With a valuation score of 5 out of 6 (where a higher score indicates more undervalued metrics), AB Volvo clearly passes most tests. Still, is there more nuance worth exploring? Next, we will break down the usual approaches for valuing a stock like this, and later, show you how a more complete picture can make all the difference.

Find out why AB Volvo's -1.7% return over the last year is lagging behind its peers.

Approach 1: AB Volvo Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by estimating a company's future cash flows and then discounting those amounts back to today, to determine what the business is intrinsically worth right now. This approach helps investors see if a company's share price reflects its real underlying value.

For AB Volvo, the most recent twelve months’ Free Cash Flow stands at SEK 22.4 billion. Analysts forecast continued growth, projecting that Free Cash Flow could reach SEK 44.3 billion by the end of 2029. While analyst estimates go out five years, later years are modeled through conservative extrapolations. Simply Wall St applies a two-stage approach, which captures both short-term analyst views and longer-term expectations.

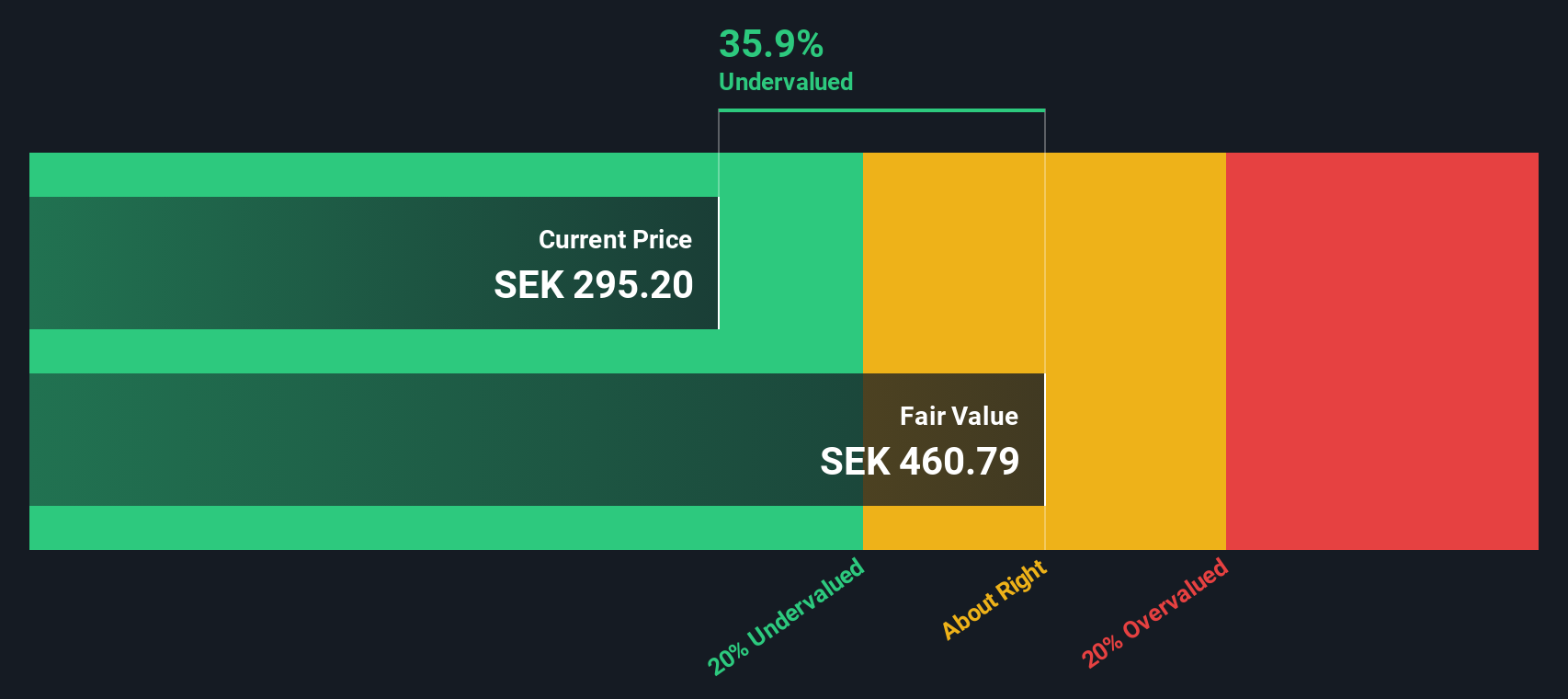

Applying the DCF calculation, these future cash flows are discounted to SEK 362.8 per share. This reflects the value in today’s terms. Based on this analysis, AB Volvo shares are trading at a 28.0% discount to their intrinsic value. This suggests the market has not yet fully recognized the company’s earnings power and cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AB Volvo is undervalued by 28.0%. Track this in your watchlist or portfolio, or discover 869 more undervalued stocks based on cash flows.

Approach 2: AB Volvo Price vs Earnings (PE)

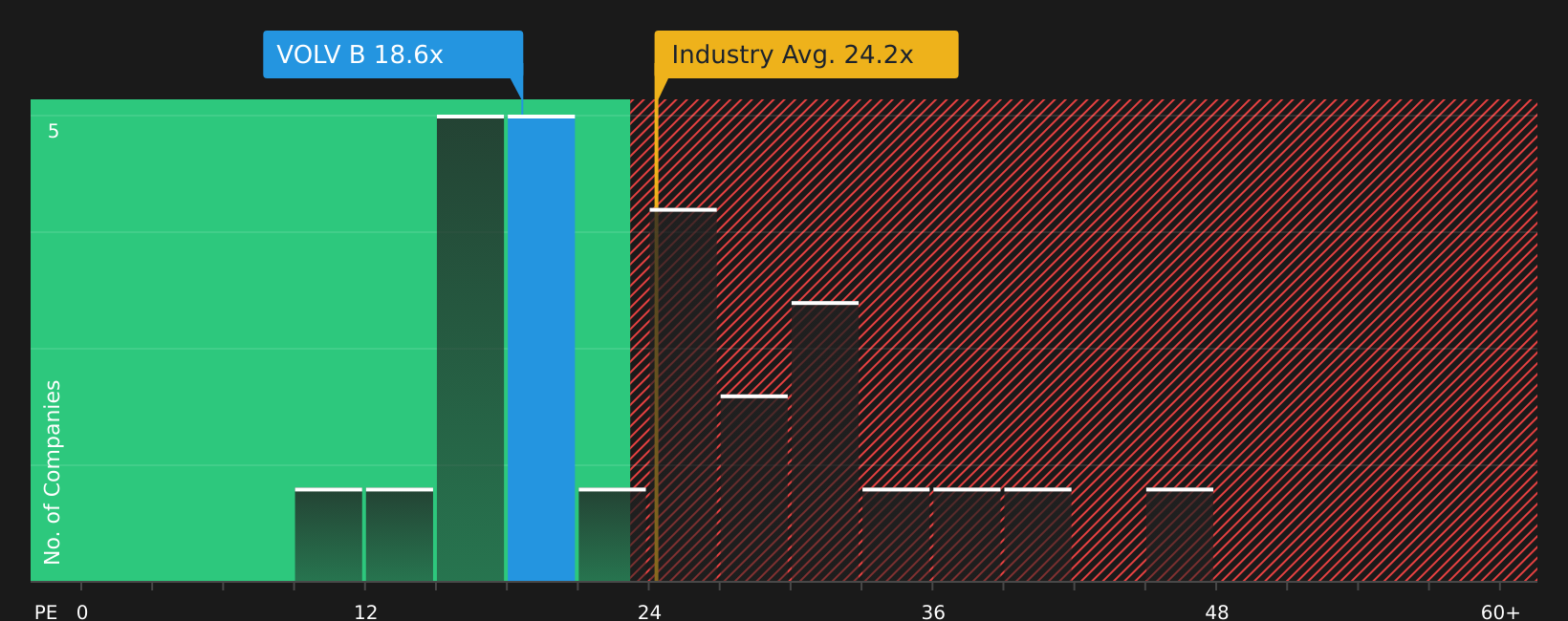

The Price-to-Earnings (PE) ratio is widely considered one of the best ways to value profitable companies, as it quickly shows how much investors are willing to pay for each kroner of earnings. For established names like AB Volvo, a PE ratio also builds in market growth expectations and perceptions of risk. Companies with solid future prospects or lower risk profiles often command higher multiples.

Currently, AB Volvo trades on a PE ratio of 14.9x. This is notably lower than the average for its Machinery industry peers, which stands at 24.4x, and much below the peer group average of 32.6x. While comparing against these benchmarks is helpful, it is important to note that multiples can reflect a range of factors, from varying growth trajectories to different risk exposures.

This is where Simply Wall St’s "Fair Ratio" steps in. The Fair Ratio represents the multiple AB Volvo would typically deserve based on a blend of important factors, including its earnings growth outlook, industry type, profit margins, size, and market risks. Because this measure is tailored, it is far more telling than just a simple industry average or peer comparison.

In AB Volvo’s case, the Fair Ratio is calculated at 33.7x. Comparing this with the current PE of 14.9x, it appears the shares are trading at a significant discount to what they could be worth based on the company's fundamentals and outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1401 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AB Volvo Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, intuitive way to express your perspective on a company's future by turning your assumptions about its revenue, margins, and fair value into a story that links its business outlook to what you believe the stock is truly worth.

By connecting a company's story to a custom financial forecast, Narratives let you explore different scenarios and instantly see what a fair price could be. Narratives are a popular feature on Simply Wall St's Community page, where millions of investors share their own views. This makes it easy for anyone to compare, learn, and make data-driven decisions with confidence.

This tool helps you decide whether to buy or sell by showing you how your Fair Value compares to the current share price, and it dynamically updates as new information, such as company earnings or industry news, becomes available.

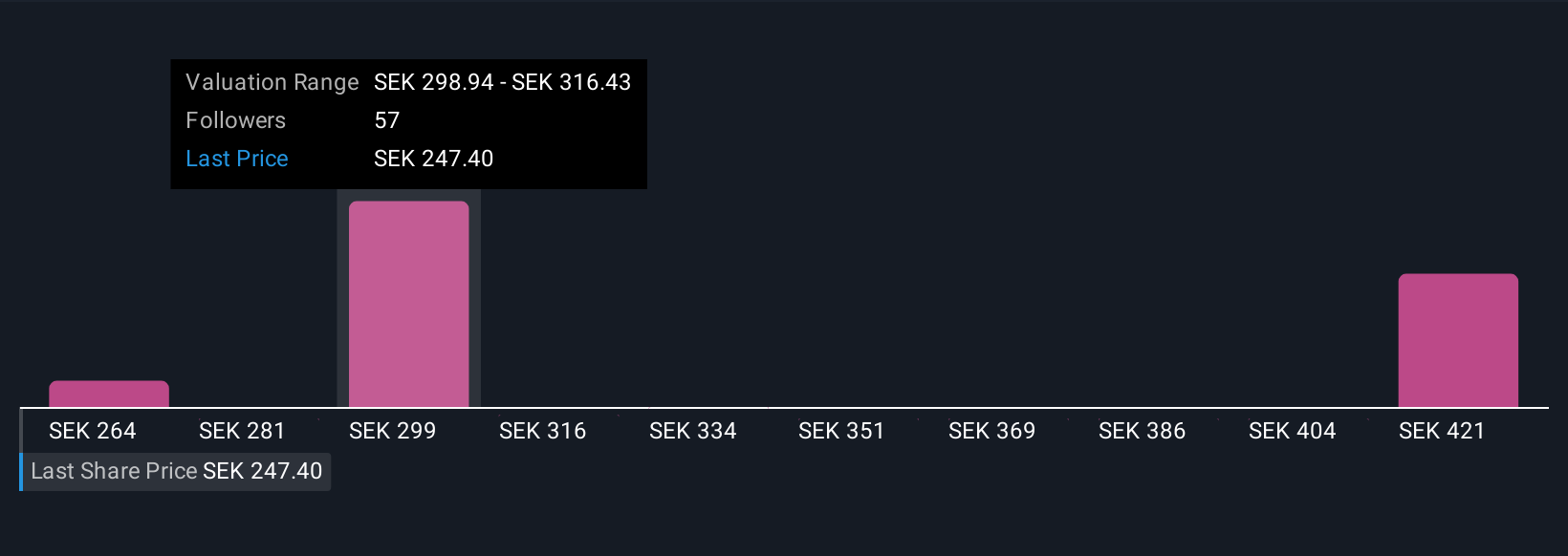

For example, among recent AB Volvo Narratives, one investor’s fair value estimate is SEK 270, based on expectations of steady dividend growth and strong fundamentals. Another investor’s estimate is as high as SEK 438.8, reflecting a belief in Volvo’s rapid electrification and profit margin expansion. This demonstrates how Narratives help you understand the full spectrum of what the stock could be worth.

Do you think there's more to the story for AB Volvo? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com