3 European Dividend Stocks To Enhance Your Portfolio

As the European market navigates a landscape of mixed stock index performances and steady interest rates from the European Central Bank, investors are keenly observing opportunities for stable returns amid these fluctuating conditions. In this context, dividend stocks can offer a compelling option for those looking to enhance their portfolios with reliable income streams.

Top 10 Dividend Stocks In Europe

| Name | Dividend Yield | Dividend Rating |

| Zurich Insurance Group (SWX:ZURN) | 4.43% | ★★★★★★ |

| Scandinavian Tobacco Group (CPSE:STG) | 9.83% | ★★★★★★ |

| Holcim (SWX:HOLN) | 4.42% | ★★★★★★ |

| HEXPOL (OM:HPOL B) | 5.00% | ★★★★★★ |

| freenet (XTRA:FNTN) | 6.77% | ★★★★★☆ |

| Evolution (OM:EVO) | 4.94% | ★★★★★★ |

| DKSH Holding (SWX:DKSH) | 4.21% | ★★★★★★ |

| Cembra Money Bank (SWX:CMBN) | 4.69% | ★★★★★★ |

| Bravida Holding (OM:BRAV) | 4.77% | ★★★★★★ |

| Banque Cantonale Vaudoise (SWX:BCVN) | 4.67% | ★★★★★☆ |

Click here to see the full list of 228 stocks from our Top European Dividend Stocks screener.

We'll examine a selection from our screener results.

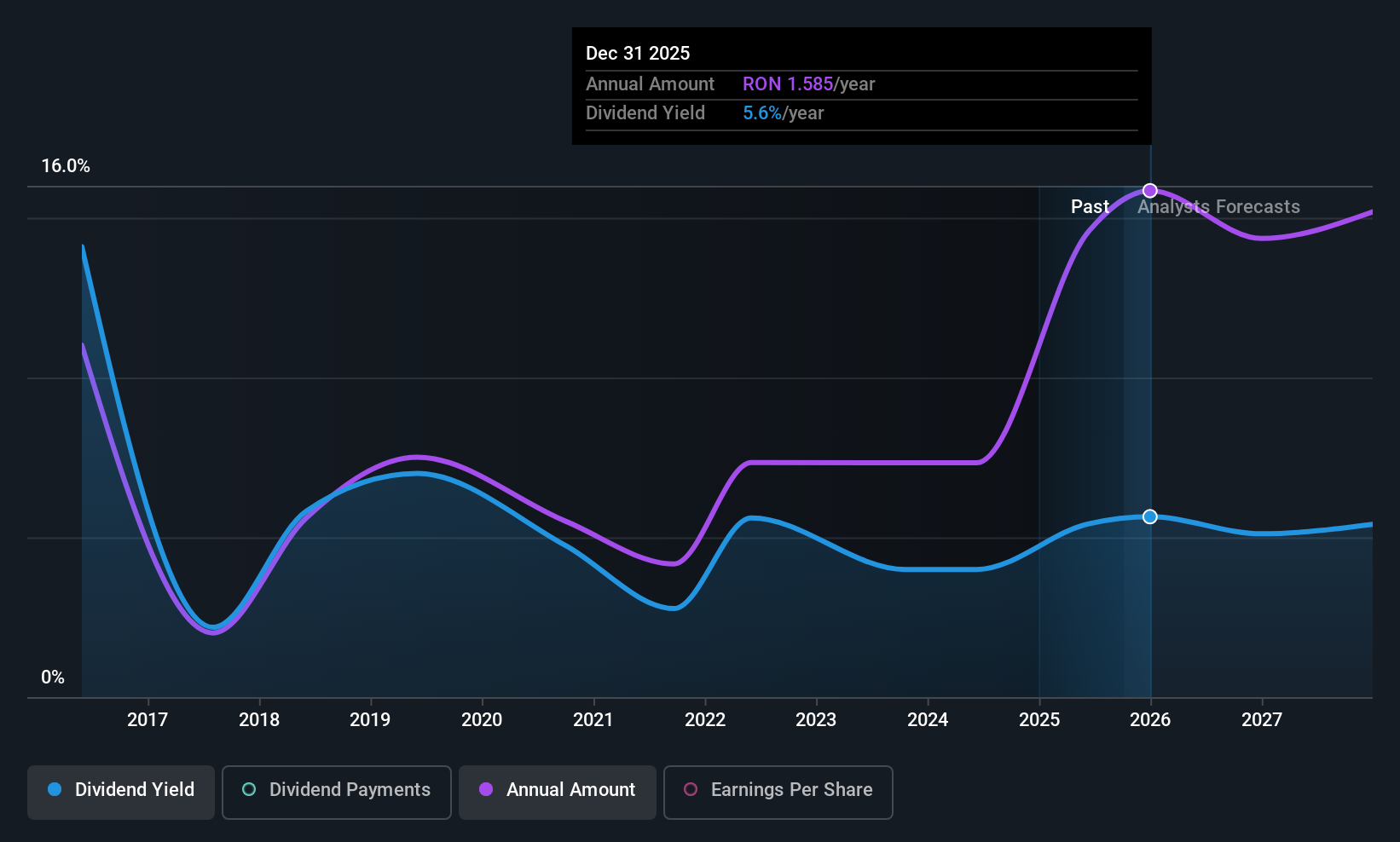

Banca Transilvania (BVB:TLV)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Banca Transilvania S.A. offers a range of banking products and services across Romania, Italy, and the Republic of Moldova, with a market capitalization of RON31.36 billion.

Operations: Banca Transilvania's revenue segments include SME (RON566.40 million), Micro (RON1.47 billion), Retail (RON3.74 billion), Treasury (RON1.31 billion), Mid Corporate (RON685.41 million), Large Corporate (RON802.68 million), and Leasing and Consumer Loans from Non-Bank Financial Institutions (RON826.52 million).

Dividend Yield: 5.1%

Banca Transilvania's dividends are well-covered by earnings, with a payout ratio of 35.6%, and this is expected to remain sustainable in the coming years. While its dividend yield of 5.07% is below top-tier payers in Romania, it offers good value compared to peers. Despite a volatile dividend history, recent approvals for a RON 700 million cash dividend distribution from past reserves highlight the bank's commitment to rewarding shareholders.

- Click here and access our complete dividend analysis report to understand the dynamics of Banca Transilvania.

- Our expertly prepared valuation report Banca Transilvania implies its share price may be lower than expected.

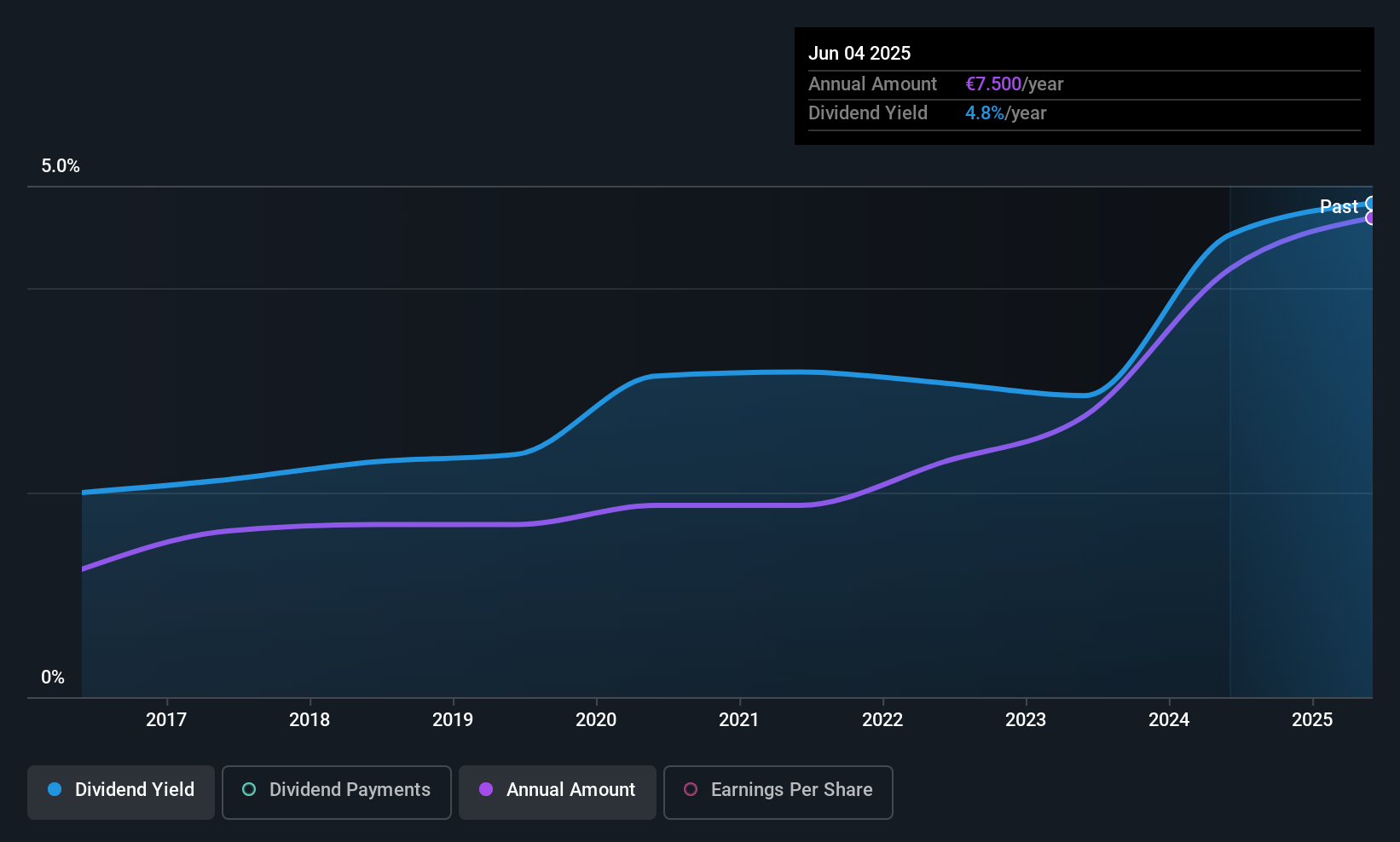

Exacompta Clairefontaine (ENXTPA:ALEXA)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Exacompta Clairefontaine S.A. is involved in the production, finishing, and formatting of papers across France, Europe, and internationally with a market cap of €194.61 million.

Operations: Exacompta Clairefontaine S.A. generates revenue through its Paper segment, which contributes €352.79 million, and its Transformation segment, which adds €596.53 million.

Dividend Yield: 4.4%

Exacompta Clairefontaine's dividends have been stable and growing over the past decade, supported by a low payout ratio of 39.5% and a cash payout ratio of 29.1%, indicating sustainability. Despite trading at 22% below estimated fair value, its dividend yield of 4.36% is lower than the top quartile in France. Recent executive changes could impact strategic direction, as operating income guidance suggests challenges ahead after reporting a drop in net income for H1 2025 compared to last year.

- Click to explore a detailed breakdown of our findings in Exacompta Clairefontaine's dividend report.

- The valuation report we've compiled suggests that Exacompta Clairefontaine's current price could be quite moderate.

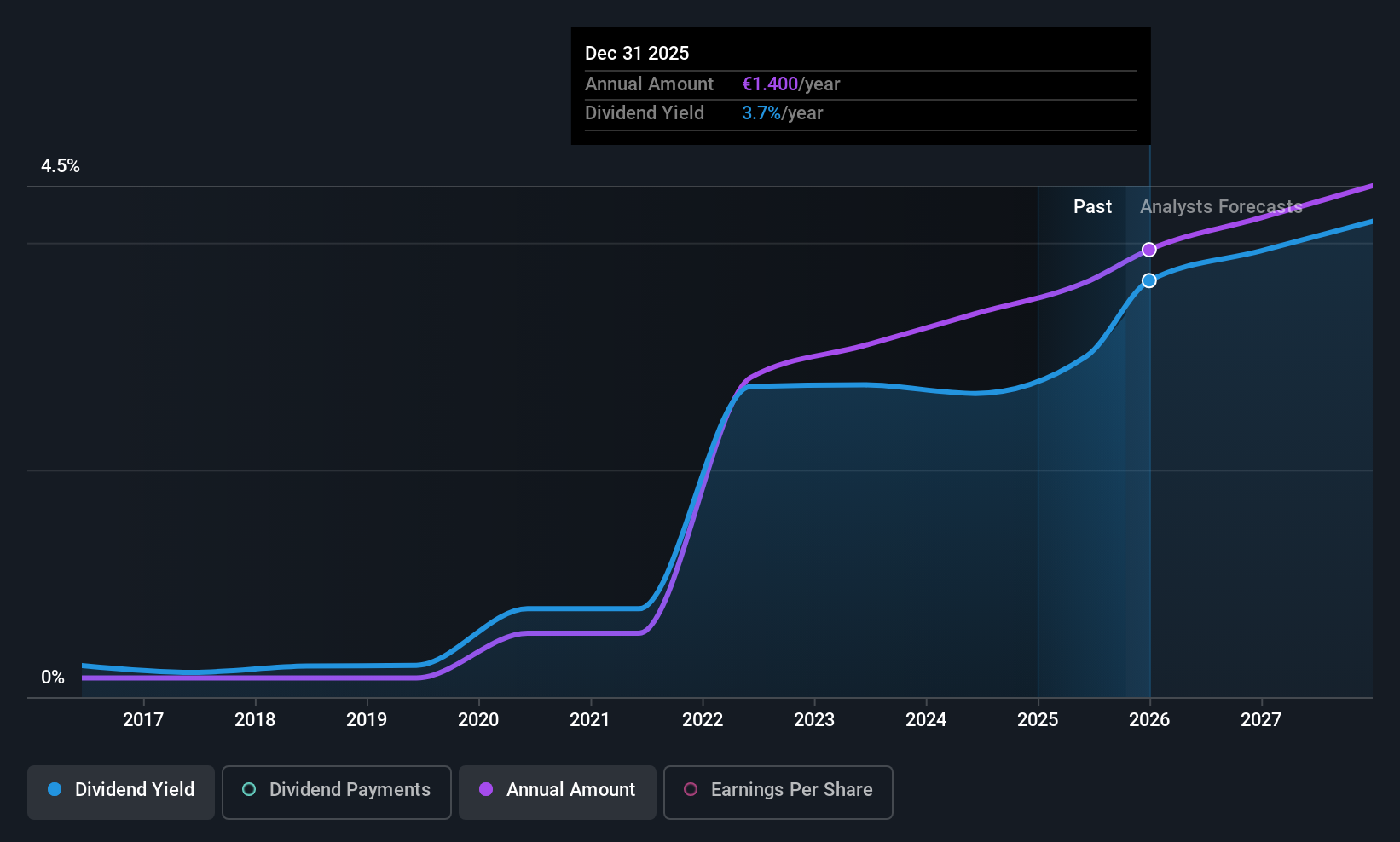

Neurones (ENXTPA:NRO)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Neurones S.A. offers infrastructure, application, and consulting services in France with a market cap of €1 billion.

Operations: Neurones S.A.'s revenue is primarily derived from Infrastructure Services (€510.40 million), Application Services (€271.70 million), and Council (€50.08 million).

Dividend Yield: 3.2%

Neurones offers reliable dividends, with payments increasing and remaining stable over the past decade. The dividend yield of 3.16% is modest relative to top-tier French payers, but sustainability is underscored by a payout ratio of 62.2% and cash payout ratio of 47.6%. Recent earnings guidance confirms expected revenues near €850 million for 2025 despite a slight dip in net income for H1 compared to the previous year, reflecting resilience amid uncertainties.

- Click here to discover the nuances of Neurones with our detailed analytical dividend report.

- The analysis detailed in our Neurones valuation report hints at an inflated share price compared to its estimated value.

Make It Happen

- Click this link to deep-dive into the 228 companies within our Top European Dividend Stocks screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com