- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalShould Investors Rethink IREN After Its 630% Rally and Microsoft Contract News?

- Curious if IREN stock is the real deal or just another name catching headlines? Here is what investors should know before considering an investment.

- IREN has seen its share price increase by 26.5% in the past week and 630.5% year-to-date, indicating strong momentum and changing viewpoints on risk and opportunity.

- Some of this significant growth is linked to positive developments in the cryptocurrency and tech sectors, with IREN often noted in industry coverage as benefiting from rising demand for digital infrastructure. Recent merger speculation and new data center projects have also boosted market attention, raising its profile with both analysts and retail investors.

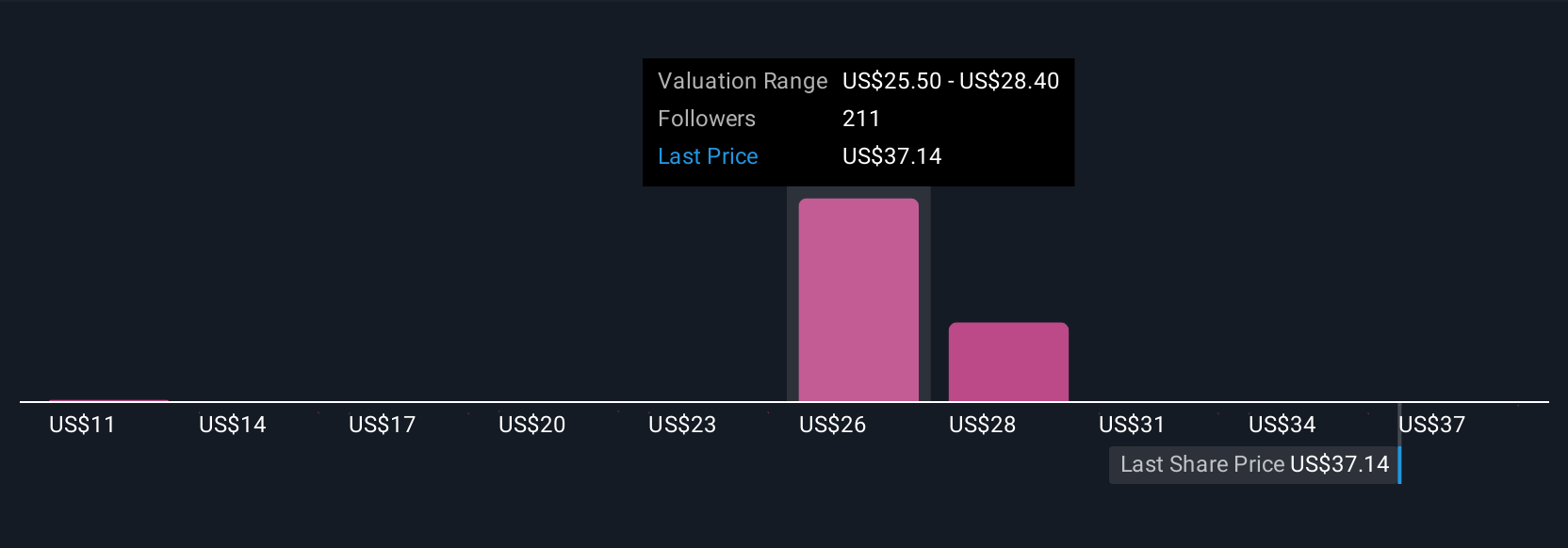

- In terms of value, IREN scores a 2 out of 6 in our valuation checks. See the full breakdown here. So, how should you think about what IREN is worth? Consider classic valuation methods, and there is also an approach that even experienced investors sometimes overlook.

IREN scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: IREN Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by taking its future projected cash flows and discounting them back to today’s dollars. This approach helps investors gauge what a business might really be worth and goes beyond recent headlines or short-term market shifts.

For IREN, the DCF analysis relies on cash flow projections extending out ten years. The company's latest reported Free Cash Flow (FCF) stands at a deficit of $1,045.57 million. Forecasters expect this number to turn positive by 2027, reaching $525 million, then accelerating steadily with projections of over $2.18 billion by 2035. Estimates beyond 2027 are derived from extrapolations by Simply Wall St, as analysts usually provide up to five years of data.

After incorporating these projections and discounting them to present value, IREN's estimated intrinsic value is $106.43 per share. Given the current share price, this suggests the stock is trading at a 28.2% discount and is considered undervalued by this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests IREN is undervalued by 28.2%. Track this in your watchlist or portfolio, or discover 849 more undervalued stocks based on cash flows.

Approach 2: IREN Price vs Sales

The price-to-sales (P/S) ratio is often a useful metric when evaluating technology companies like IREN, especially when profits are volatile or when the company is in a rapid growth phase. This measure compares a company’s market value to its revenue, which is less impacted by one-off charges, and helps investors evaluate how much they are paying for each dollar of sales.

Growth expectations play a key role in what constitutes a “normal” or “fair” P/S ratio. Companies with higher projected growth or scalable business models often justify higher multiples. Those perceived as riskier may trade at a discount. Risk, profitability, and market conditions also factor into how these ratios should be interpreted.

Currently, IREN’s P/S ratio stands at 41.78x, which is significantly higher than the software industry average of 5.11x and above the average of peers at 29.68x. At first glance, this suggests IREN may be richly valued compared to both its industry and other similar companies. However, Simply Wall St’s proprietary Fair Ratio for IREN is 20.11x. The Fair Ratio incorporates a range of important company-specific considerations, such as IREN’s revenue growth, profit margin potential, industry position, market cap and company-specific risks. This makes it a more holistic benchmark than just comparing with peers or industry averages.

Comparing IREN’s current P/S ratio (41.78x) to its Fair Ratio (20.11x), the stock trades well above where fundamentals suggest it ought to be. This indicates that significant growth is already priced in by the market.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1407 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your IREN Narrative

Earlier we mentioned there is an even better way to understand what IREN is worth, so let's introduce you to the power of Narratives. A Narrative is your own story or perspective about a company. It's how you tie together the facts, your assumptions about future revenue, earnings, margins, and the company’s fair value to express what you believe is truly happening beyond the numbers.

Narratives link a company’s story to a financial forecast and then connect that directly to a fair value, giving you a clear and actionable investment view. Using Simply Wall St’s Community page, any investor can create, view, or update their IREN Narrative, making this approach accessible and interactive for millions of users. Narratives help you decide whether to buy or sell by comparing your own Fair Value against the current market price. Because they are updated dynamically as new news or earnings data comes in, they keep your investment thinking current and evidence-based.

For IREN, for example, some investors’ Narratives forecast a fair value as high as $98 per share, while more cautious Narratives put fair value near $11, reflecting different expectations for Bitcoin, AI growth, and execution risk. By creating or choosing your Narrative, you get to see the market through your own lens in a systematic and intelligent way.

For IREN, however, we'll make it really easy for you with previews of two leading IREN Narratives:

Fair Value: $98.21

IREN is currently trading at approximately 22.2% below this fair value.

Projected Revenue Growth Rate: 40%

- Highlights IREN's transformation from a renewable-powered Bitcoin miner to a pioneer in AI cloud infrastructure, validated by a $9.7 billion multi-year contract with Microsoft.

- Points to rapid execution and scaling of energy-efficient operations, with strong cash reserves and no debt, positioning the company as a core AI infrastructure play.

- Emphasizes significant upside potential if IREN continues to deliver on AI and mining expansion, but cautions around execution risk and recurring dilution.

Fair Value: $57.00

IREN is currently trading at approximately 34.1% above this fair value.

Projected Revenue Growth Rate: 73.19%

- Argues the federal government's recent AI infrastructure and incentives policy has turbocharged IREN's prospects but also led to aggressive valuation multiples.

- Notes IREN sits at the heart of US data center expansion with gigawatt-scale projects in Texas, but expansion plans require flawless execution and face competition from larger peers.

- Warns that the stock is priced for perfection in policy support, rapid buildout, and sustained profitability, and that any misstep or policy reversal could trigger sharp downside.

Do you think there's more to the story for IREN? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com