Assessing LyondellBasell After a 44.8% Share Price Drop and Strategic Review News

- Thinking about whether LyondellBasell Industries is worth a spot in your portfolio? You're not alone; many investors are eyeing the stock, curious if there's value hiding beneath the headlines.

- The share price has dropped by 44.8% over the past year, with a further 5.9% slip in the last week. This highlights just how quickly market sentiment and risk perception can change.

- Recent news about ongoing strategic reviews and the company's announced cost-cutting initiatives have added fuel to the conversation, as management signals they are taking meaningful steps to adapt. These developments are giving investors fresh reasons to look at LyondellBasell's business fundamentals as the dust settles from the recent price swings.

- By our checks, LyondellBasell Industries currently scores 5 out of 6 on our valuation scorecard, suggesting it appears undervalued on nearly every front. Let's break down the main valuation approaches next, and stay tuned because we'll wrap up with a smarter, more holistic way to look at value.

Approach 1: LyondellBasell Industries Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model projects a company's future cash flows and discounts them back to today's value. This approach gives investors a sense of what the business is worth based on its ability to generate cash in the years ahead.

For LyondellBasell Industries, the current Free Cash Flow (FCF) stands at $933.6 Million. Analysts forecast these cash flows to grow over the coming years, with projections reaching $1.44 Billion by the end of 2027 and extrapolated to roughly $2.59 Billion by 2035. These projections are built using analyst estimates for the next five years and Simply Wall St's own growth assumptions for later years.

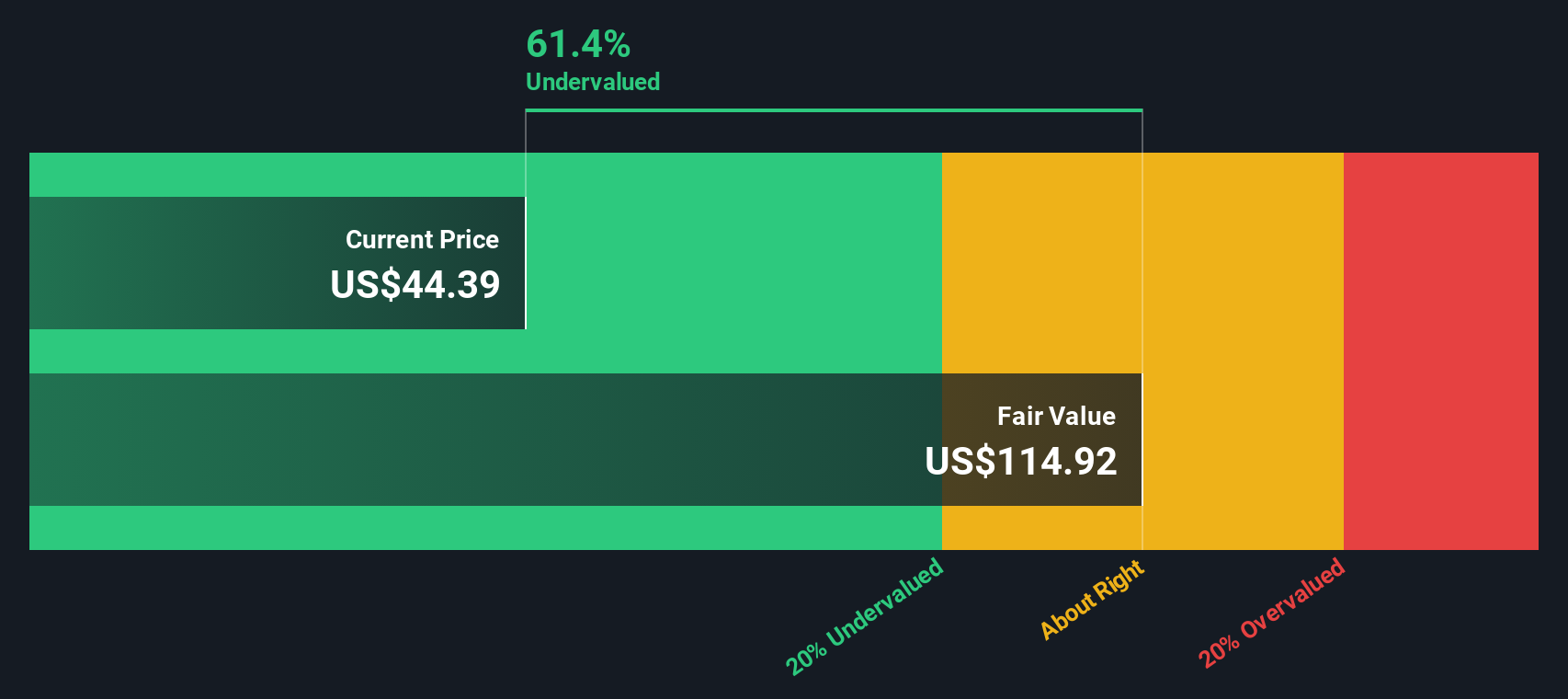

By taking all these future cash flow projections into account and discounting them to their present value, the DCF model estimates LyondellBasell Industries' intrinsic share value at $96.51. Given current market pricing, this suggests the stock is trading at a 54.4% discount to its fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests LyondellBasell Industries is undervalued by 54.4%. Track this in your watchlist or portfolio, or discover 844 more undervalued stocks based on cash flows.

Approach 2: LyondellBasell Industries Price vs Sales

For companies like LyondellBasell Industries, which are established and consistently profitable, the Price-to-Sales (P/S) ratio is a useful valuation tool. It helps investors assess whether the value assigned by the market to each dollar of revenue makes sense, especially in industries where earnings can swing with market cycles.

Market expectations for growth and risk directly affect what is considered a “normal” or “fair” P/S ratio. Faster-growing, lower-risk companies often command higher multiples. In contrast, market uncertainty or sluggish growth typically results in a lower ratio.

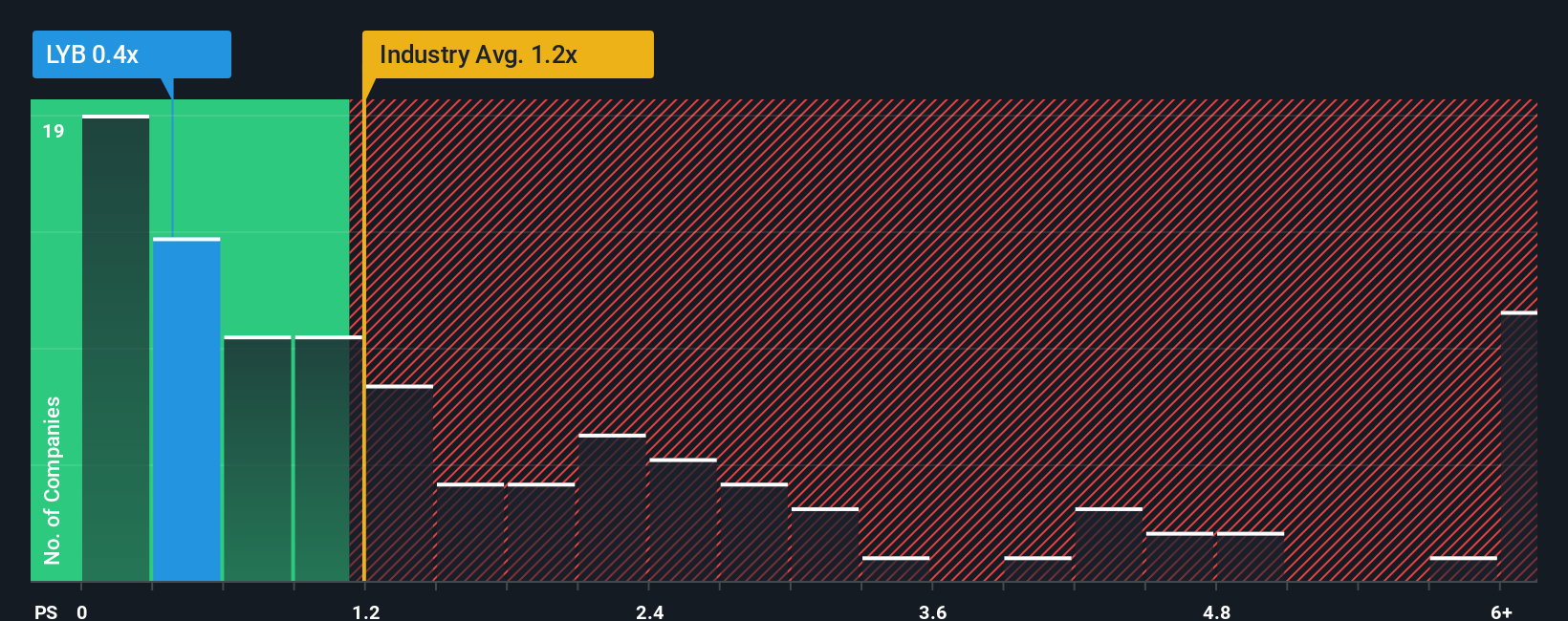

Currently, LyondellBasell Industries trades at a P/S ratio of 0.37x. This compares favorably to both the chemicals industry average of 1.23x and the peer group average of 0.58x, suggesting the stock is priced well below where most similar companies are valued on this metric.

Simply Wall St introduces the “Fair Ratio,” a proprietary gauge reflecting the P/S multiple most appropriate for a company given its growth prospects, profitability, risk profile, industry, and size. Unlike straightforward comparisons to industry averages or direct peers, the Fair Ratio factors in nuances like below- or above-average growth or unique risks that might otherwise be overlooked.

For LyondellBasell, the Fair Ratio is set at 0.60x. With the current P/S at 0.37x, the stock is trading noticeably below what one would expect based on its fundamentals and sector context. This supports the case that LyondellBasell Industries remains undervalued on a sales basis.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1405 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your LyondellBasell Industries Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, structured way to capture your personal perspective on a company by weaving together your expectations for its story, future revenue, earnings, and margins to arrive at your own view of fair value. Narratives link the company’s “big picture” (such as strategic shifts, industry trends, or risks) directly to the numbers in a financial forecast and ultimately to a fair value per share.

On Simply Wall St, Narratives make it easy for anyone, not just professional analysts, to express their view and see how it stacks up against others. Found on the Community page used by millions of investors, Narratives update automatically as fresh news or events emerge so your investment thesis is always up to date. They help you decide when to buy or sell by letting you compare your Fair Value to the current market Price at a glance.

For example, some investors believe LyondellBasell Industries will achieve a fair value close to $90 based on expectations of a rebound driven by recycling innovation and global market expansion, while others focus on headwinds and set far lower fair values, such as $44, reflecting a more cautious outlook. Your Narrative puts your thesis front and center, tailored to real-time developments that matter to you.

Do you think there's more to the story for LyondellBasell Industries? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com