Vertex (VERX) Lowers Guidance and Announces Buyback Is Its Leadership Reset a Strategic Game Changer?

- Vertex, Inc. recently reported mixed third-quarter 2025 results, with US$192.11 million in revenue, lowered full-year guidance due to customer bankruptcies and accelerated cloud platform migrations, authorized a US$150 million share repurchase program, and announced executive changes including a new incoming CEO and a senior European appointment.

- This combination of growing cloud revenue, revised outlook, and leadership changes marks a pivotal shift in Vertex's approach toward international growth and long-term shareholder value strategies.

- We'll explore how Vertex's updated earnings guidance and buyback announcement may influence the company's investment narrative going forward.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Vertex Investment Narrative Recap

For investors considering Vertex, the core belief is in the accelerating demand for cloud-based tax compliance as global regulations tighten and enterprises migrate to advanced platforms. The latest quarter’s mixed results reflect both this momentum and the risks, momentum from strong cloud revenue growth, but risks from customer bankruptcies and migration disruptions. While the revised guidance highlights near-term uncertainty, the most important catalyst remains major ERP and e-invoicing deadlines, and the biggest risk is ongoing client attrition; the news has not materially shifted these dynamics.

Among the recent updates, the US$150 million share repurchase program stands out, as it underscores management’s confidence despite short-term earnings headwinds. This buyback coincides with a period of leadership transition and heightened competition, reinforcing the company’s commitment to generating long-term value, even as volatility in customer retention metrics remains in focus.

But, while cloud momentum is promising, investors should stay mindful of the ongoing risk that...

Read the full narrative on Vertex (it's free!)

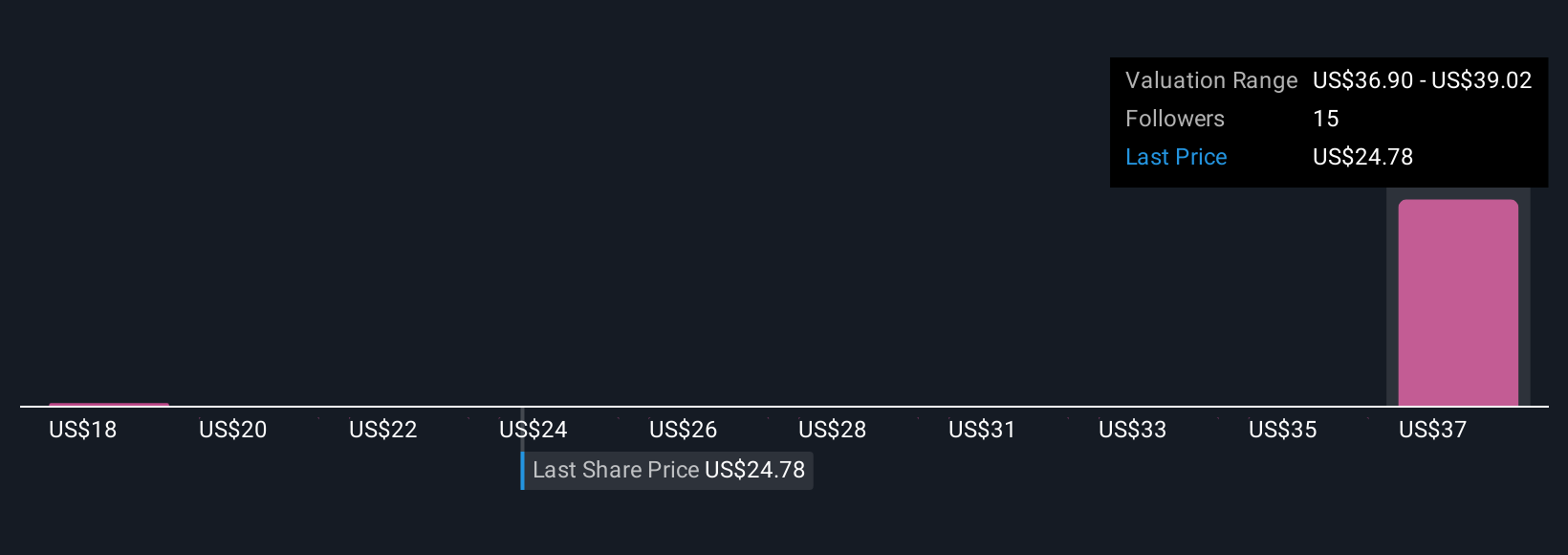

Vertex's narrative projects $1.1 billion in revenue and $71.6 million in earnings by 2028. This requires 14.6% yearly revenue growth and a $122 million increase in earnings from the current level of -$50.4 million.

Uncover how Vertex's forecasts yield a $36.79 fair value, a 83% upside to its current price.

Exploring Other Perspectives

Three retail investors in the Simply Wall St Community have provided fair value estimates ranging from US$17.84 to US$36.79. With customer retention volatility currently in focus, these varied perspectives highlight how market conditions can impact sentiment and expectations, consider comparing several viewpoints before forming your own assessment.

Explore 3 other fair value estimates on Vertex - why the stock might be worth 11% less than the current price!

Build Your Own Vertex Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vertex research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Vertex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vertex's overall financial health at a glance.

No Opportunity In Vertex?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com