What Do Recent Price Swings Signal for Brown-Forman’s True Value in 2025?

- Thinking about whether Brown-Forman stock is a genuine bargain or just looks cheap on paper? You're not alone. It's a good time to take a closer look at what drives its current value.

- The stock has experienced a whirlwind of ups and downs lately, with a 1.0% gain over the last week but still down 33.2% for the past year. This has made investors wonder if change is in the air.

- Some of this volatility has been shaped by shifting industry dynamics and evolving consumer preferences, which have attracted new attention to Brown-Forman's portfolio and strategy. Recent headlines discuss the impact of global demand trends and strategic shifts in the spirits sector, all of which set the stage for re-evaluating the company's worth.

- When it comes to valuation, Brown-Forman scores a solid 5 out of 6 on our value checks. This suggests it stacks up well on almost every metric. We'll dig into those traditional valuation methods next, but make sure you stick around to the end for a fresh and arguably smarter way to look at the company's true value.

Find out why Brown-Forman's -33.2% return over the last year is lagging behind its peers.

Approach 1: Brown-Forman Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by forecasting a company’s expected future cash flows and then discounting them back to today’s value. This provides an estimate of the business's intrinsic worth, independent of current market sentiment.

For Brown-Forman, the DCF approach uses a 2 Stage Free Cash Flow to Equity model. The company's most recent annual Free Cash Flow sits at $556 million, with analyst forecasts expecting this to grow over the next five years. Projections estimate that by 2028, annual Free Cash Flow could reach $782 million. Beyond this, further growth is extrapolated at a steady rate, leading to an estimated Free Cash Flow of $975 million in 2035. This steady climb reflects ongoing business resilience.

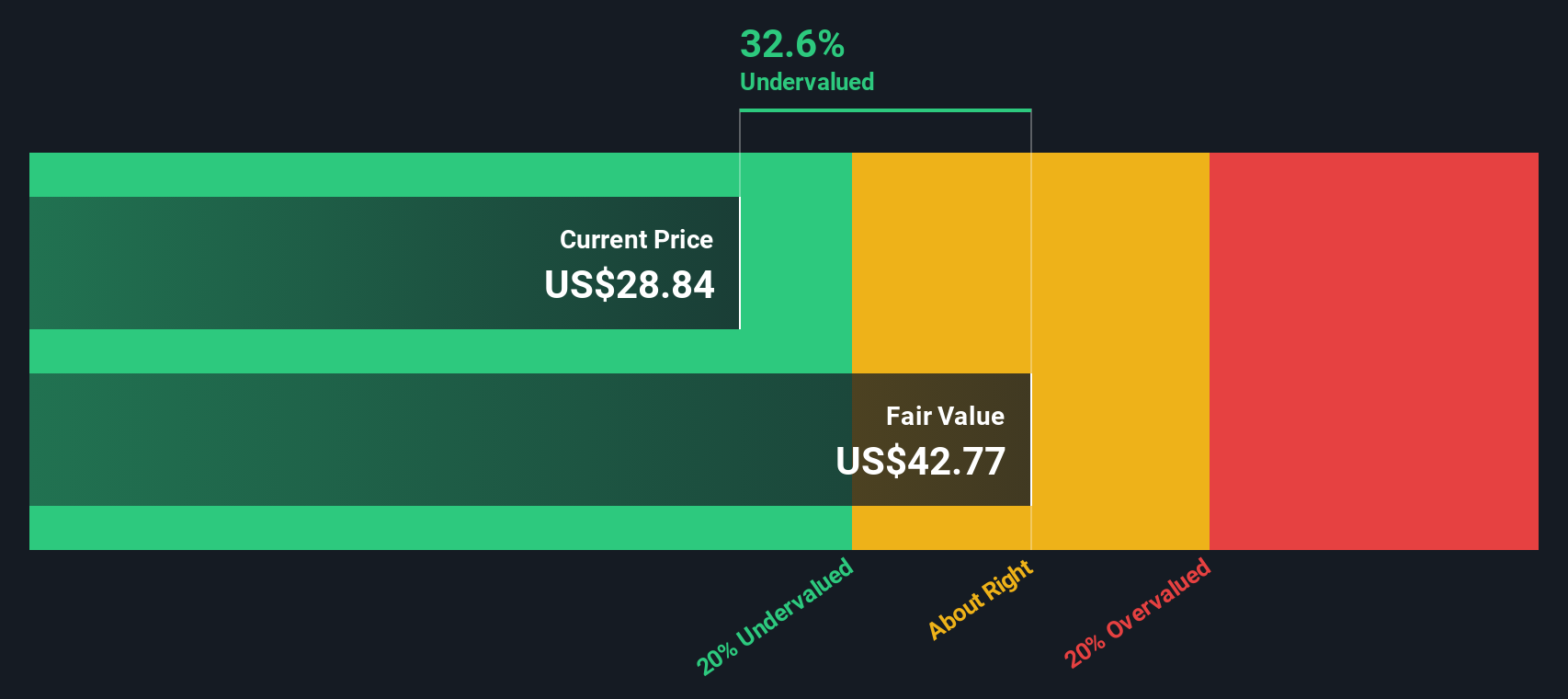

After factoring in all projected cash flows and discounting them to present value, the DCF model arrives at an intrinsic value of $42.45 per share. This estimate puts the stock at a 36.2% discount to its current trading price, implying that Brown-Forman shares are presently undervalued by the market.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Brown-Forman is undervalued by 36.2%. Track this in your watchlist or portfolio, or discover 836 more undervalued stocks based on cash flows.

Approach 2: Brown-Forman Price vs Earnings

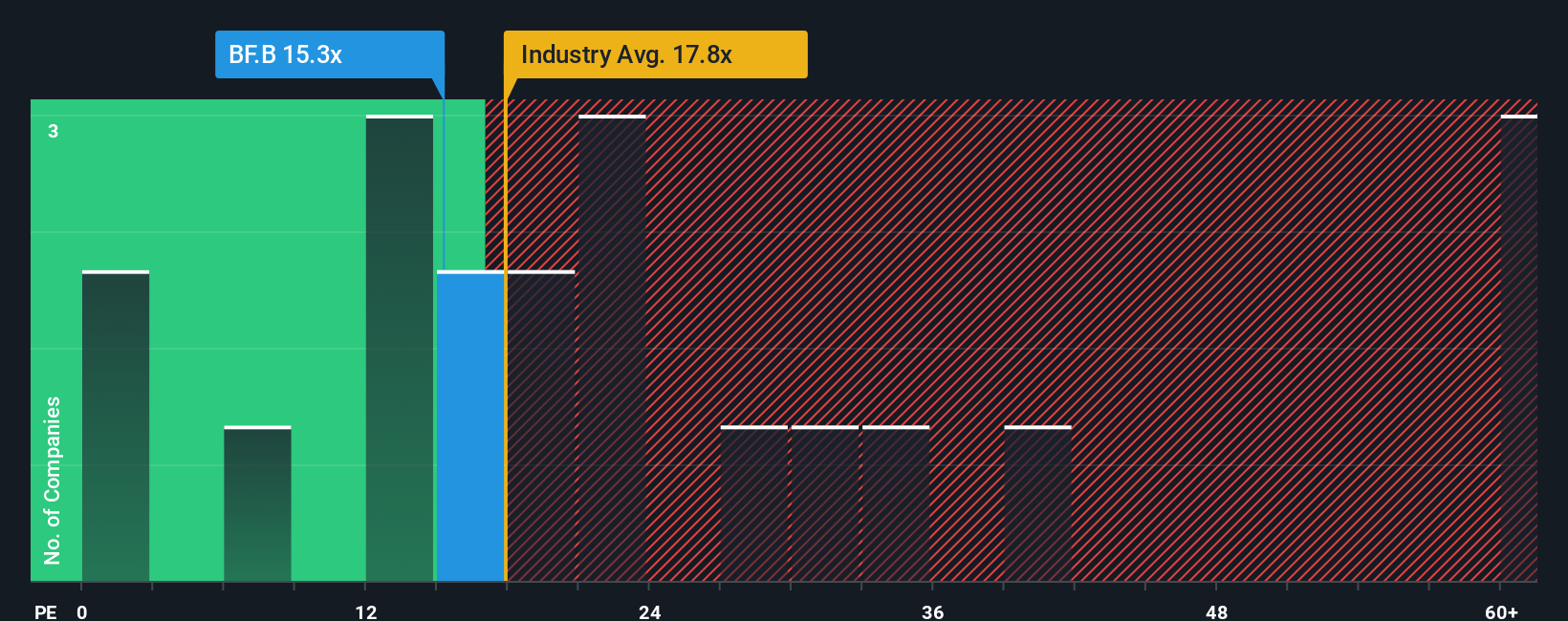

Price-to-Earnings (PE) is the go-to valuation measure for profitable companies like Brown-Forman, because it connects the stock price to the actual earnings being generated. For investors, the PE ratio offers quick insight into how the market is valuing current profits, making it especially useful for stable, revenue-generating businesses.

Growth prospects and business risks play a big role in determining what a "normal" or “fair” PE ratio should be. If a company’s earnings are expected to grow quickly and its risks are low, investors are usually willing to pay a higher multiple. By contrast, slower growth or higher risks pull the fair PE lower. The benchmark always depends on more than just the raw number; it’s about the outlook and the level of certainty around profits continuing.

Currently, Brown-Forman trades at a PE ratio of 15.16x. This is below the Beverage industry average of 17.64x and also below the average of its peers at 16.96x, indicating the market values it somewhat conservatively right now. However, benchmarks like industry and peer averages only tell part of the story. Simply Wall St’s proprietary “Fair Ratio” digs deeper. It is set at 16.04x for Brown-Forman and is uniquely calibrated by factors beyond earnings, such as growth potential, profit margin strength, sector trends, company size, and risk profile. This tailored benchmark avoids the pitfalls of broad comparisons and helps investors account for what truly drives value in Brown-Forman's unique context.

When you match Brown-Forman’s current PE (15.16x) against its Fair Ratio (16.04x), the difference is less than 0.10, suggesting that the stock price is in line with what you’d expect for the company’s profile.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1402 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Brown-Forman Narrative

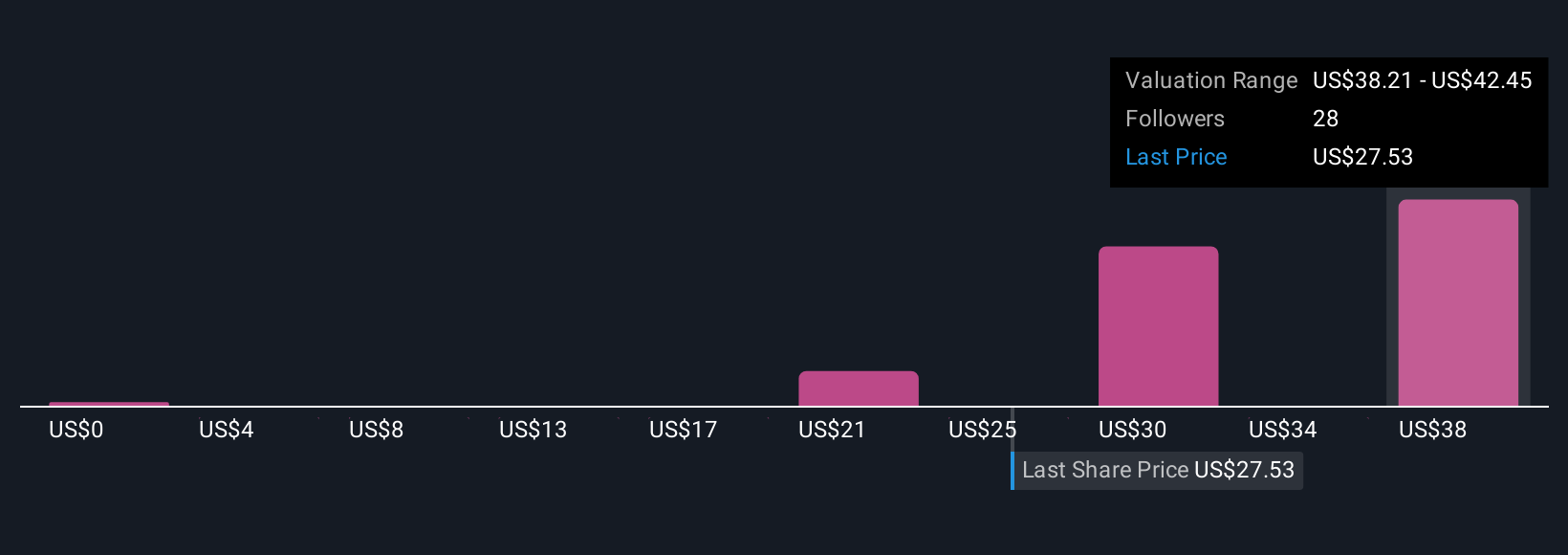

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple way to build your own story about a company that makes the numbers truly meaningful by deciding what you believe about Brown-Forman’s future. You can set your own assumptions for fair value, future revenue, earnings, and margins, then see how your outlook compares to both the current price and what others expect.

Rather than sticking only to static ratios or consensus targets, Narratives help you connect the “why” behind the numbers to your unique view of Brown-Forman. This approach automatically links your thesis to a financial forecast and the resulting fair value. It is fast and accessible, available for free within Simply Wall St’s Community page. Millions of investors use this tool to create, share, and debate perspectives as new news or earnings reports are released.

With Narratives, you can make buy or sell decisions by directly comparing your Fair Value (from your assumptions) to the market Price, and you’ll see your story update dynamically as market conditions change. For Brown-Forman, you might be bullish and forecast a Fair Value close to $40 if you expect booming international growth, or more cautious and closer to $25 if you see risks outweighing opportunity, all based on how you see the company's future playing out.

Do you think there's more to the story for Brown-Forman? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com