Is BMW Attractively Priced After Recent Gains and Electric Vehicle Investments in 2025?

- Wondering if Bayerische Motoren Werke is a smart buy right now? You are not alone, and there is a lot to unpack when it comes to figuring out whether the stock offers genuine value.

- The stock’s performance has been a mix of short-term volatility and longer-term growth, with a 16.7% gain over the past year and a 2.8% climb so far in 2024, despite recent dips in the last month.

- Recent headlines have focused on BMW’s ongoing investments in electric vehicles and strategic global partnerships, generating both optimism and debate among investors. New developments in sustainability and technology adoption have clearly influenced how the market is thinking about the company's long-term trajectory.

- Across our six key valuation checks, Bayerische Motoren Werke scores a 4 out of 6 for being undervalued. Here is how these valuation methods compare and a look at an even more comprehensive way to assess the stock’s real value by the end of this article.

Approach 1: Bayerische Motoren Werke Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a widely used method for estimating a company's intrinsic value by forecasting its future cash flows and discounting them back to the present. This approach aims to capture what the business is truly worth, based on projected cash it is expected to generate.

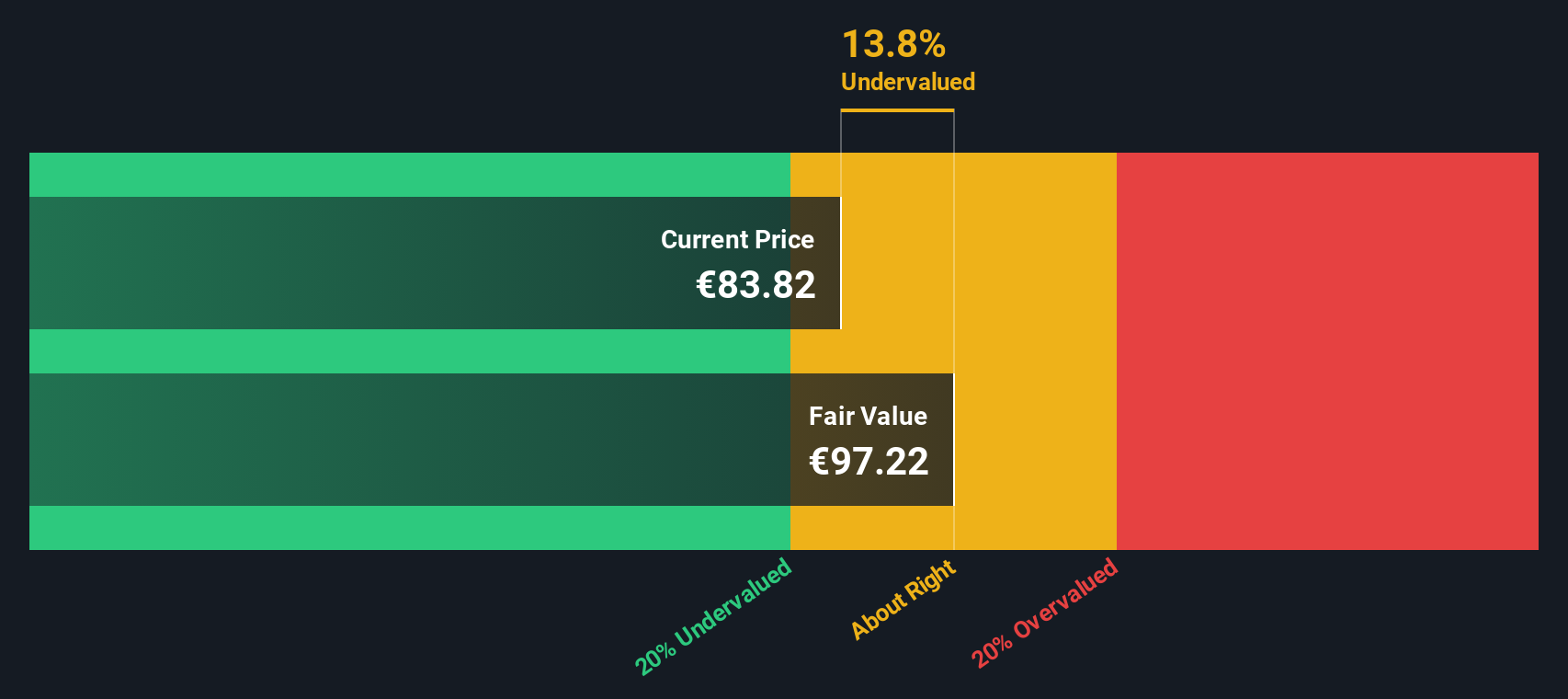

For Bayerische Motoren Werke, analysts use a 2 Stage Free Cash Flow to Equity model. The company reported a last twelve months free cash flow (FCF) of -€1.19 billion. Despite this recent negative figure, forecasts anticipate a recovery, with analyst estimates and extrapolated projections showing FCF growing to approximately €5.4 billion annually by 2029. The ten-year FCF outlook is based initially on analyst consensus and then on Simply Wall St’s own extrapolation beyond the available estimates.

By discounting these forecasted euro cash flows to their present value, the model calculates an intrinsic value of €95.99 per share. This figure is currently about 16.3% above the share price, suggesting the stock trades below its estimated fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Bayerische Motoren Werke is undervalued by 16.3%. Track this in your watchlist or portfolio, or discover 841 more undervalued stocks based on cash flows.

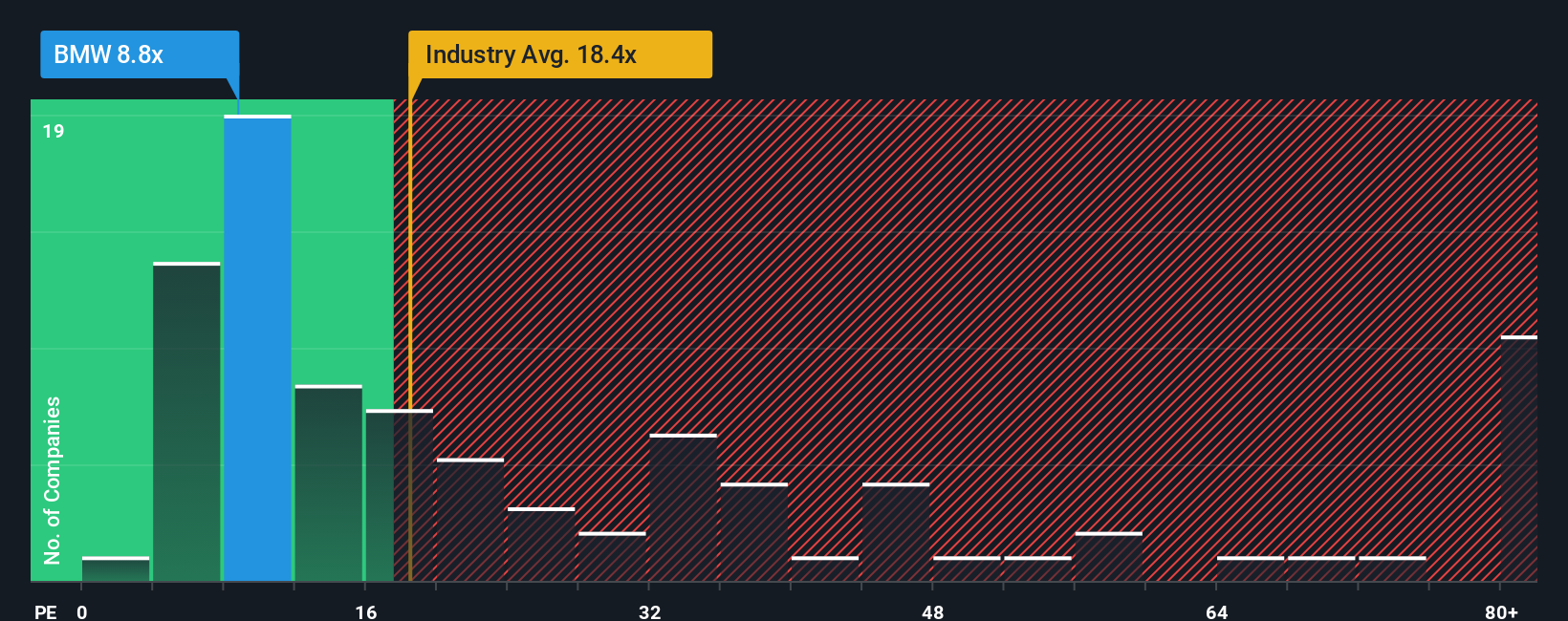

Approach 2: Bayerische Motoren Werke Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a popular valuation measure for profitable companies because it compares a stock’s current price to its per-share earnings, providing a straightforward snapshot of how much investors are willing to pay now for each euro of earnings.

Typically, companies with higher earnings growth potential or lower risk command a higher "normal" PE ratio. This reflects investors’ willingness to pay a premium for future growth and stability. Conversely, lower growth prospects or greater risks usually translate to a lower fair PE.

Bayerische Motoren Werke currently trades at a PE ratio of 8.6x. This is well below both the Auto industry average of 18.0x and the peer group average of around 17.6x. On the surface, this gap could suggest undervaluation, but benchmarks only tell part of the story.

Simply Wall St’s proprietary “Fair Ratio” provides a more nuanced view and estimates a PE of 12.1x for Bayerische Motoren Werke. This fair value takes into account not just industry and market averages, but also factors like the company’s expected earnings growth, business risks, profit margins, and market capitalization. This approach aims to reflect the unique qualities and circumstances of the business, which simpler peer comparisons can miss.

Since the company's actual PE ratio (8.6x) is notably lower than its Fair Ratio (12.1x), this analysis implies that Bayerische Motoren Werke is undervalued based on its fundamentals and outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1411 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bayerische Motoren Werke Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple and powerful tool that lets you craft a story about a company, outlining your assumptions about its fair value, future revenue, earnings, and margins, and see how this story stacks up against the numbers. By connecting the company’s business outlook to a forecast and resulting fair value estimate, Narratives link the “why” behind your view with what the figures say.

Narratives are available on Simply Wall St’s Community page and are used by millions of investors to simplify decision making. They help you quickly assess whether a stock such as Bayerische Motoren Werke is under- or over-valued, by constantly comparing your fair value to the current market price. Whenever there is new information, like fresh news or updated earnings, Narratives automatically adjust, keeping your perspective as up-to-date as the market itself. For example, some BMW Narratives see fair value above €135 based on robust profit margins and EV leadership, while others are more cautious, landing as low as €68 due to risks in China and regulatory headwinds.

Do you think there's more to the story for Bayerische Motoren Werke? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com