Is Bank of Montreal’s U.S. Acquisitions Driving Real Value After a 42.7% Rally?

- Curious if Bank of Montreal is as undervalued as some investors think? Let’s break down what’s really happening with the stock’s pricing and long-term outlook.

- The stock has seen impressive growth over the past year, climbing 42.7%, and is up a striking 23.6% since the start of the year. However, recent weeks have brought some pullback.

- Much of the market’s buzz relates to Bank of Montreal’s recent strategic acquisitions in the U.S. banking sector and ongoing efforts to bolster its digital capabilities. These factors are grabbing headlines and fueling both optimism and caution among analysts.

- Currently, Bank of Montreal scores a 2 out of 6 on our valuation checks, so there’s room for a deeper dive. Let's explore traditional approaches and, at the end, reveal an even better way to judge the stock's value.

Bank of Montreal scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Bank of Montreal Excess Returns Analysis

The Excess Returns model evaluates whether a stock adds meaningful value above the cost of capital by looking at its ability to generate returns on invested equity. For Bank of Montreal, this approach weighs its projected profit-generating power against the cost of funding its operations to estimate intrinsic value per share.

Here is how the numbers stack up. The bank’s Book Value stands at CA$118.63 per share, and analysts see a Stable Earnings Per Share (EPS) of CA$14.18 going forward. This projection is based on weighted future Return on Equity data from 11 analysts, pointing to an average ROE of 12.09%. After accounting for the Cost of Equity at CA$8.35 per share, Bank of Montreal is generating an Excess Return of CA$5.83 per share. The Stable Book Value is projected at CA$117.28 per share, sourced from consensus estimates by 9 analysts.

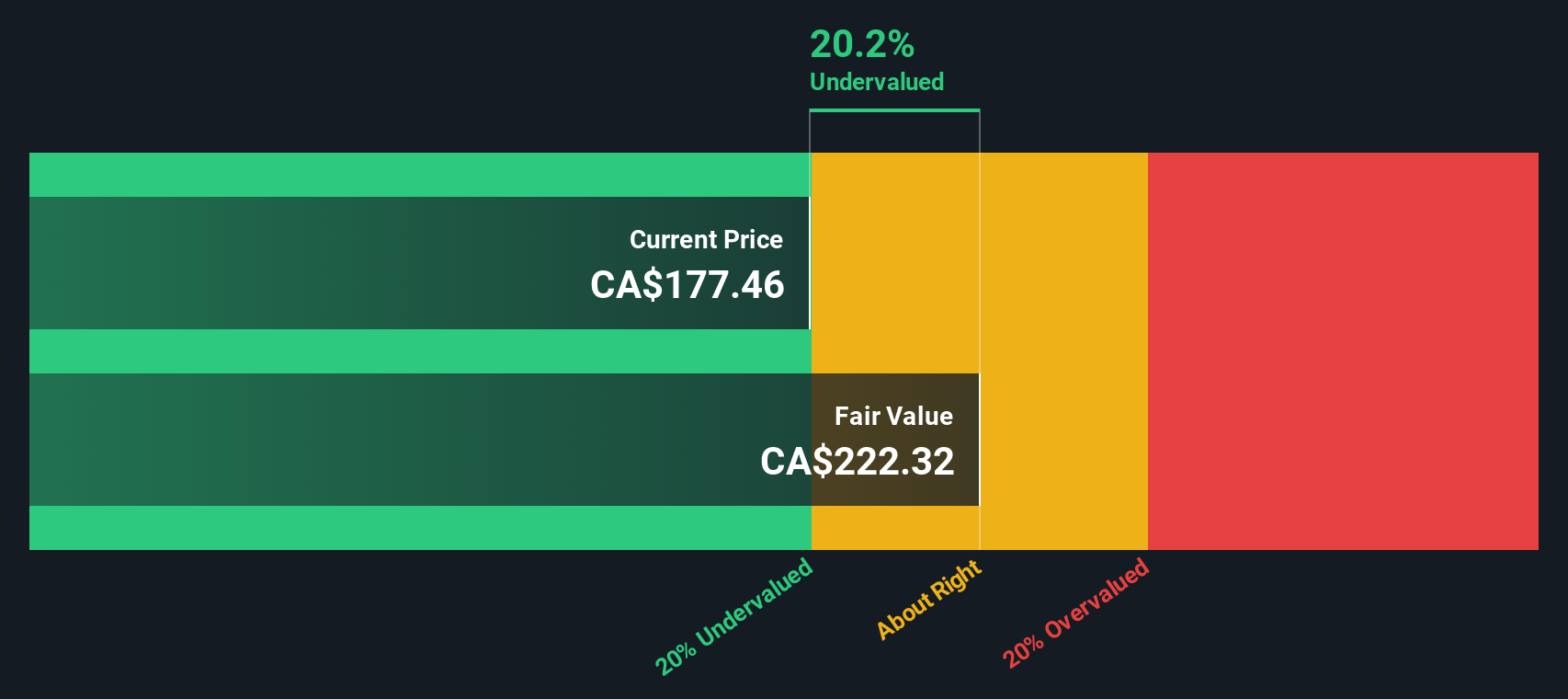

With these figures, the Excess Returns model calculates Bank of Montreal’s intrinsic value as being 29.9% above its current market price, meaning the stock appears meaningfully undervalued through this lens.

Result: UNDERVALUED

Our Excess Returns analysis suggests Bank of Montreal is undervalued by 29.9%. Track this in your watchlist or portfolio, or discover 844 more undervalued stocks based on cash flows.

Approach 2: Bank of Montreal Price vs Earnings

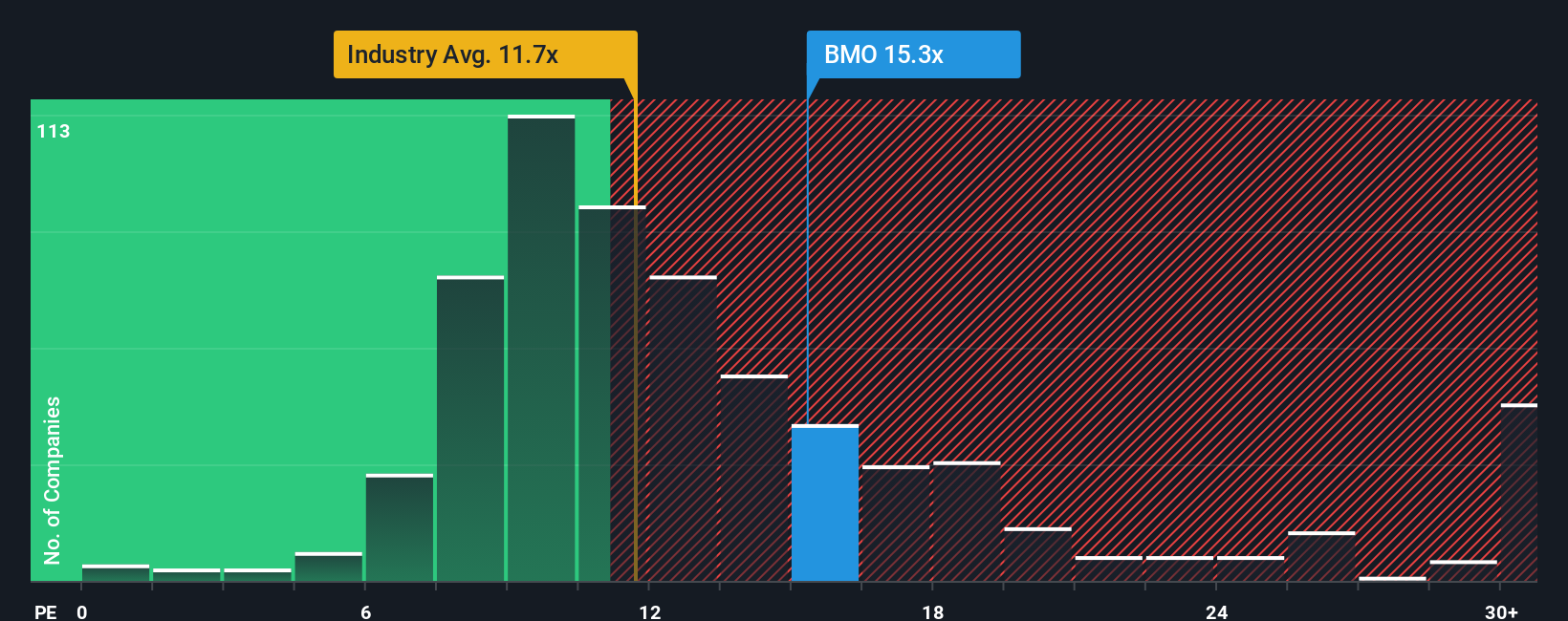

The Price-to-Earnings (PE) ratio is a favored metric for valuing profitable companies, like Bank of Montreal, because it directly relates the company's share price to its underlying earnings power. A low PE can signal a bargain, but what is considered “fair” depends on the company’s expected future growth and the perceived risks in its industry.

Currently, Bank of Montreal trades at a PE ratio of 14.91x. That is a bit higher than the average PE of Canadian banks, which sits at 10.16x, and slightly above the peer average of 14.31x. This suggests that the market assigns a premium to Bank of Montreal, likely reflecting investor optimism about its growth prospects and sustained profitability.

However, instead of only judging against industry or peer averages, the Fair Ratio offers a more nuanced perspective. Simply Wall St’s Fair Ratio for Bank of Montreal is 13.95x. This is calculated by considering the company’s own growth forecasts, profit margins, market cap, and specific risk profile. This approach is more comprehensive, capturing factors that simple averages miss, such as how much faster (or slower) the bank is growing compared to its peers, or whether it faces unique risks.

With Bank of Montreal’s current PE ratio just slightly above its Fair Ratio, the stock appears fairly valued based on its earnings potential.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Bank of Montreal Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story about a company—your own view of what drives its future—from how much it will grow revenue to what profit margins and fair value you expect, all based on your reading of its business, news, and trends.

Narratives bridge the gap between the numbers and the bigger picture, linking your belief in Bank of Montreal’s strategy, operations, and risks to a financial forecast and a calculated fair value. On Simply Wall St’s Community page, Narratives are simple to use, available to millions of investors, and help you track whether your story says the stock is undervalued or overvalued as news and results come in.

By building your own Narrative, you can quickly see if now is the right time to buy or sell, since your assumed Fair Value updates alongside real-world changes and new analyst data. For example, one investor’s Narrative, confident about the future of digital banking, might justify a price target as high as CA$180, while another, wary of credit risks and expenses, may set their fair value closer to CA$151.

Do you think there's more to the story for Bank of Montreal? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com