A Look at Prada (SEHK:1913) Valuation Following Strong Nine-Month 2025 Revenue Growth

Prada (SEHK:1913) just released its unaudited revenue results for the first nine months of 2025, showing total net revenues of EUR 4,069.7 million. This represents an increase of 9% over the same period last year.

See our latest analysis for Prada.

Following the upbeat revenue announcement, Prada’s share price has shown signs of renewed optimism, climbing 14.6% over the last 90 days despite a challenging year-to-date price return of -25.4%. Short-term price movements remain volatile, but its 5-year total shareholder return of 45.6% highlights the brand’s ability to deliver for long-term investors, even amid shifting sector dynamics.

If luxury’s resilience has you thinking beyond fashion, now is a perfect time to discover fast growing stocks with high insider ownership.

The question for investors now is whether Prada’s recent rally leaves the shares undervalued and poised for further gains, or if today’s price already reflects the market’s expectations for future growth.

Most Popular Narrative: 24.7% Undervalued

With Prada's last close at HK$46.90 and the most widely followed narrative fair value sitting at HK$62.32, the market has yet to fully price in expected growth and margin improvements. This wide gap in price targets reflects a strong belief in upcoming catalysts and strategic transformations within the business.

Prada's ongoing investment in new product collections, broadening price points and enhancing personalization (for example, make-to-measure and bespoke in flagship stores) positions the group to capture growth from both affluent core clients and younger, aspirational demographics globally, supporting long-term revenue and gross margin expansion.

Curious what market shifts and bold growth assumptions are driving such a big gulf between share price and potential value? This narrative hints at a blueprint involving premium brand strategy, digital transformation, and ambitious earnings projections. If you want to discover how analysts expect Prada's numbers to evolve and what could really justify that premium, explore the full story now.

Result: Fair Value of $62.32 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if affluent tourism declines or Prada's retail improvements fail to keep pace with rivals, these risks could challenge the company's current growth projections and valuation narrative.

Find out about the key risks to this Prada narrative.

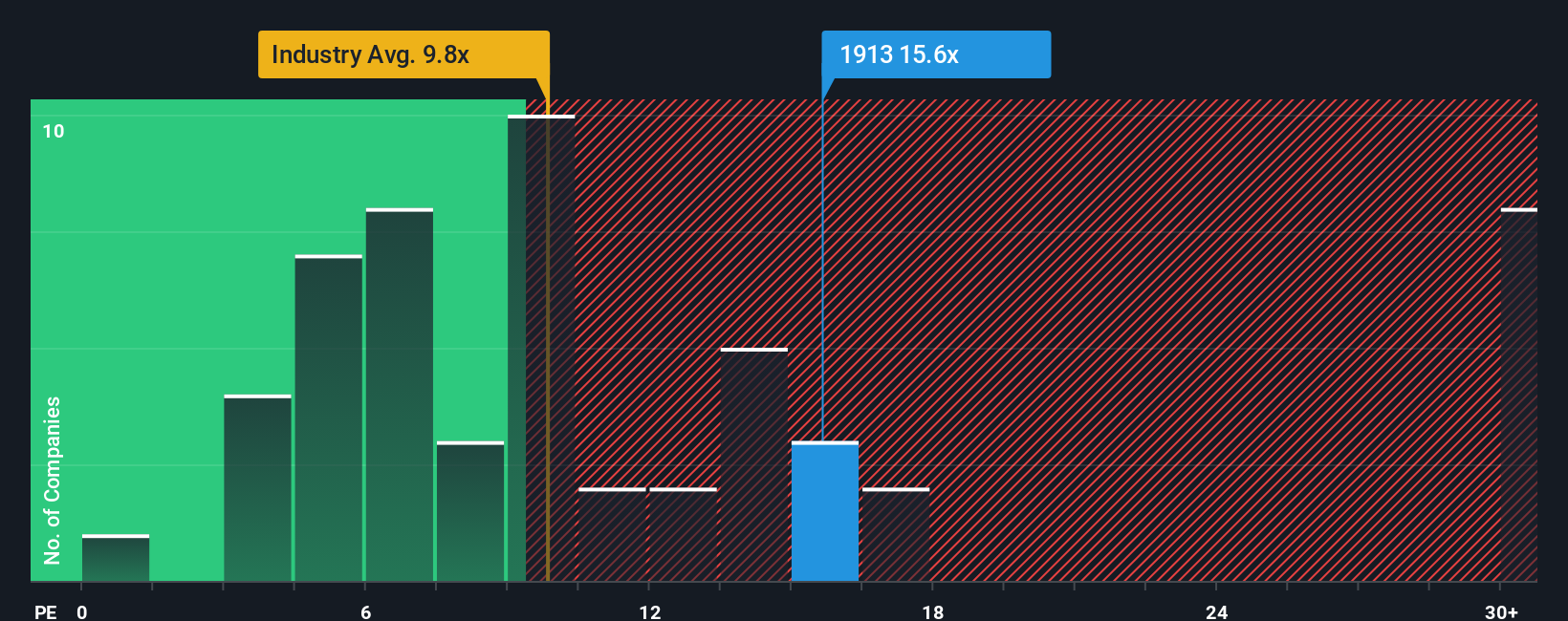

Another View: Multiples Tell a Different Story

While fair value estimates suggest Prada is undervalued, a look at its price-to-earnings ratio reveals a more cautious picture. Shares trade at 16x earnings, which is pricier than both the Hong Kong luxury sector average (9.6x) and the fair ratio of 11.9x. This gap hints at higher valuation risk. Could investor expectations be running ahead of reality?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Prada Narrative

Not convinced by these narratives, or looking to dig deeper into the numbers yourself? You can shape your own view in just a few minutes by Do it your way.

A great starting point for your Prada research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never limit themselves to just one opportunity. Open up new possibilities by targeting stocks with unique growth engines, high yield, or future-ready technology. Here are three shortcuts worth your attention:

- Multiply your income potential with high-yielding companies by tapping into these 20 dividend stocks with yields > 3% offering exceptional payouts in uncertain times.

- Capitalize on the artificial intelligence surge and spot undervalued disruptors through these 27 AI penny stocks designed to pinpoint tomorrow’s AI leaders before the crowd catches on.

- Seize the momentum in fast-changing digital assets by checking out these 82 cryptocurrency and blockchain stocks and get ahead with breakthrough opportunities in blockchain innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com