ZIM Integrated Shipping Services (NYSE:ZIM): Valuation in Focus as Market Reacts to Pre-Earnings Concerns

ZIM Integrated Shipping Services (NYSE:ZIM) shares slid 6% in the latest session. Investors responded to worries about weaker earnings and revenue expected in the company's upcoming November 20 report.

See our latest analysis for ZIM Integrated Shipping Services.

Despite the recent 6.33% drop in share price, ZIM Integrated Shipping Services’ stock has struggled for momentum all year, with a year-to-date share price return of -38.44%. However, the three-year total shareholder return stands out at 47.25%. This highlights how longer-term investors have weathered recent volatility as the market reassesses the company’s growth outlook and risk profile.

If the market’s choppiness has you considering alternative opportunities, this might be the perfect time to discover fast growing stocks with high insider ownership.

With ZIM’s valuation metrics trailing its industry and sentiment remaining cautious, the question for investors is clear: is there genuine upside being overlooked here, or is the market already accounting for all the risks and future prospects?

Most Popular Narrative: 8.2% Overvalued

Despite ZIM Integrated Shipping Services last closing at $14.35, the most popular narrative puts its fair value at $13.26, just below the market price. This sets the stage for a closer look at the numbers and logic behind the bearish tilt.

The company's significant exposure to volatile Transpacific trade leaves earnings highly sensitive to tariff changes and geopolitical shifts. The current overhang of U.S. and China tariffs, unpredictable regulatory moves, and alliance restructurings threaten both volume and rate stability. These factors challenge assumptions that future earnings will be resilient or steadily expanding.

Curious what kind of revenue shifts and profit margin squeeze might drive a below-market fair value? The secret sauce in this narrative is a sharp reset of industry growth expectations and a PE ratio forecast that only the boldest analysts would defend. Want to see the full set of assumptions? The details might surprise you.

Result: Fair Value of $13.26 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if ZIM's investments in fleet modernization or successful trade lane diversification pay off, these factors could quickly shift margins and earnings back in its favor.

Find out about the key risks to this ZIM Integrated Shipping Services narrative.

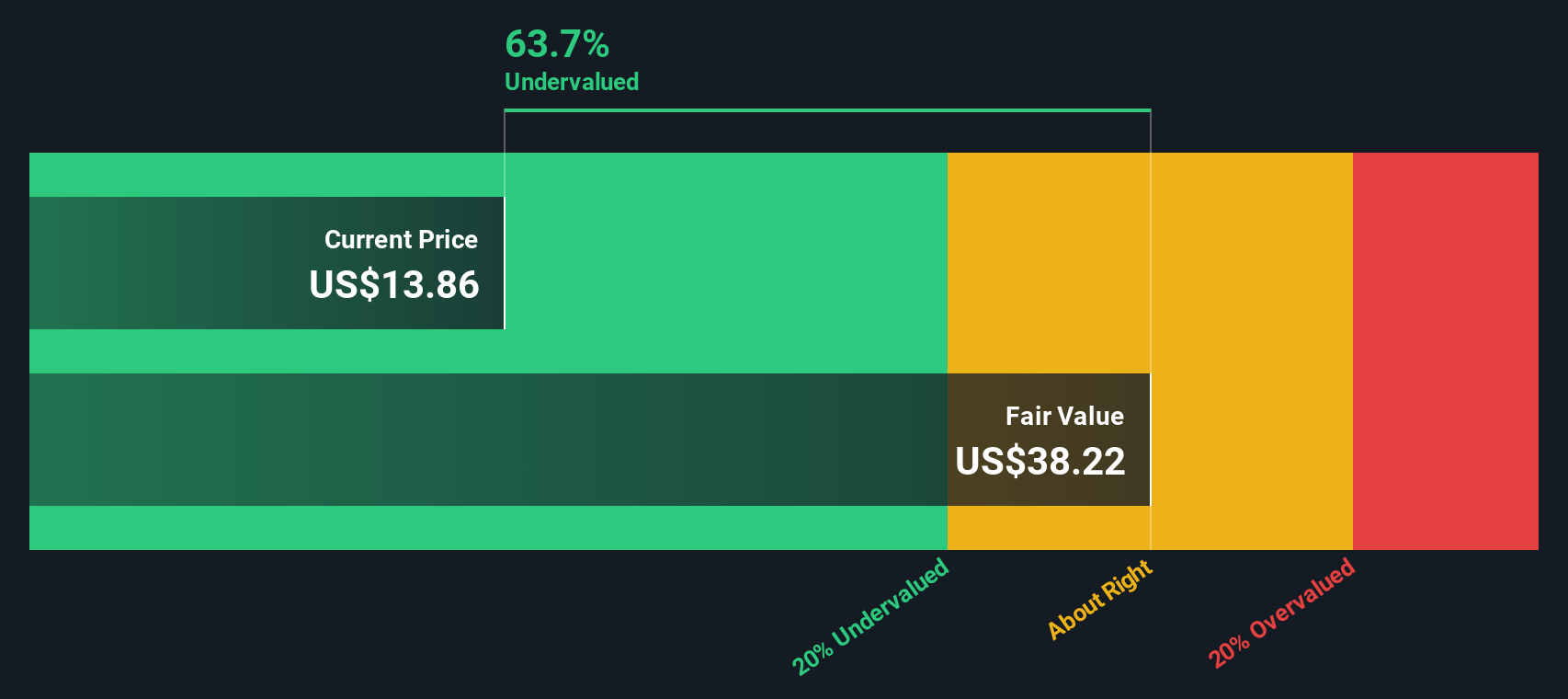

Another View: Discounted Cash Flow Sheds a Different Light

Taking a look through the lens of the SWS DCF model, ZIM Integrated Shipping Services appears significantly undervalued, trading at nearly 62.5% below our fair value estimate of $38.22. While market multiples hint at overvaluation, this approach suggests the stock could offer deep value if the assumptions hold true. Which outcome will ultimately prove right?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ZIM Integrated Shipping Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 844 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ZIM Integrated Shipping Services Narrative

Not convinced by these scenarios, or want to challenge the consensus? You can dig into the figures yourself and craft a fresh take in just minutes using Do it your way.

A great starting point for your ZIM Integrated Shipping Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Expand your horizon and lock in smarter investment moves by using the Simply Wall Street Screener to spot opportunities you won’t want to miss.

- Tap into game-changing potential by reviewing these 27 AI penny stocks, which are shaping tomorrow's markets with artificial intelligence at their core.

- Catch the next wave of passive income by targeting these 20 dividend stocks with yields > 3%, offering yields above 3% for growing your returns.

- Fuel your strategy with growth stories through these 844 undervalued stocks based on cash flows, which are trading below their projected cash flows right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com