Does the Kenvue Spinoff Signal a New Opportunity for Johnson & Johnson in 2025?

- Ever wondered if Johnson & Johnson is actually worth what it's trading for? You're in the right place to get the real story behind the price tag.

- While the stock has slipped 2.1% over the last week and 1.3% over the past month, it's up an impressive 29.3% year-to-date and 21.5% over the last year. This hints at both growth potential and shifting investor sentiment.

- In recent weeks, Johnson & Johnson has made headlines for its continued innovation in the pharmaceutical and consumer health space, including the spinoff of its consumer health unit Kenvue and new regulatory approvals for key therapies. These moves have helped fuel speculation about its future business mix and ability to drive shareholder value.

- By our numbers, the company earns a valuation score of 4 out of 6, suggesting that it looks undervalued on most of our quantitative checks. Next up, we will break down the different approaches to valuing the business and show you why there is an even better way to cut through the noise at the end of this article.

Approach 1: Johnson & Johnson Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model calculates a company's intrinsic value by taking future cash flow projections and discounting them back to today's value. This approach lets investors estimate what a business is truly worth based on how much cash it is expected to generate going forward.

For Johnson & Johnson, the most recent trailing twelve-month Free Cash Flow sits at $19.47 Billion. Analyst estimates project strong growth, with annual FCF expected to rise steadily. By 2029, cash flows are forecast to reach $35.5 Billion, and long-term projections by Simply Wall St suggest FCF could surpass $53.9 Billion by 2035. These figures reflect not just near-term analyst outlooks but also extrapolations based on the company’s historic growth rates and sector dynamics.

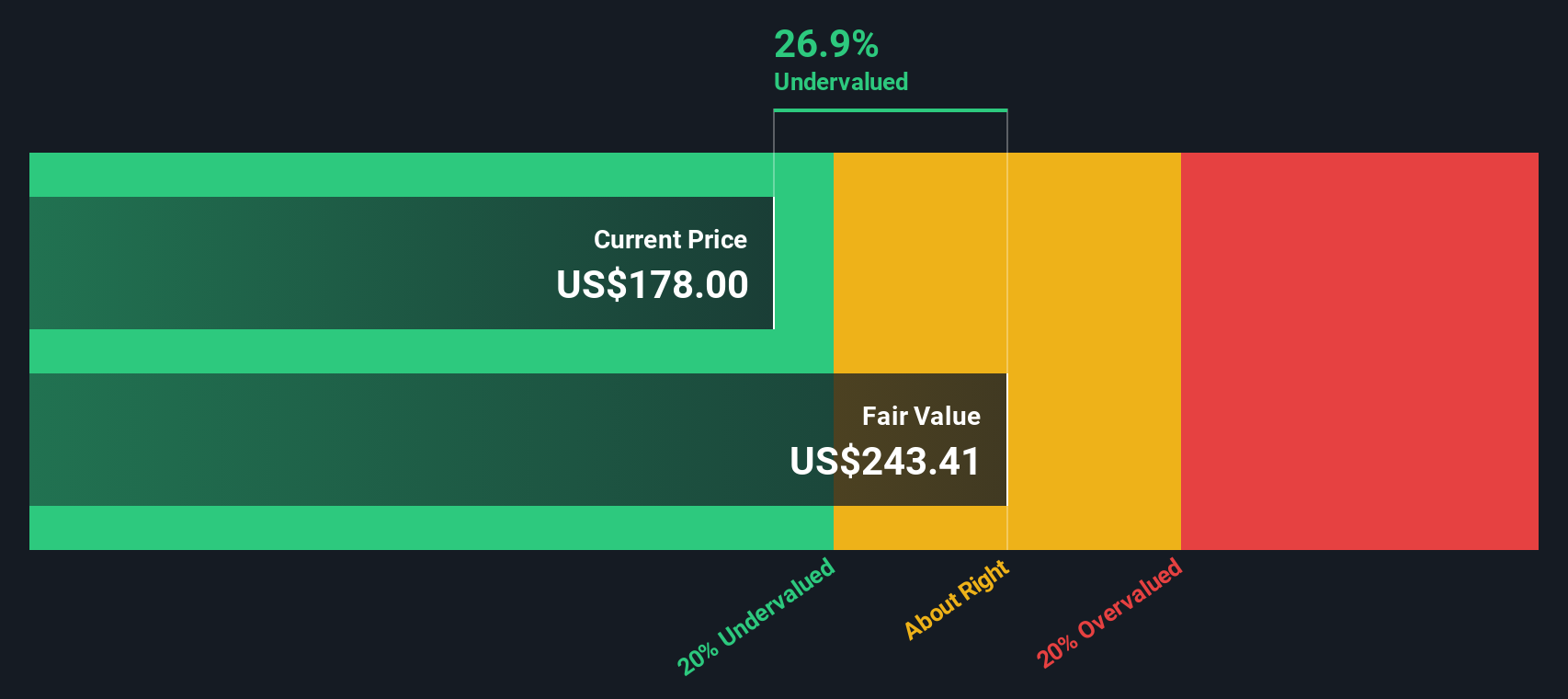

Based on these projections, the DCF model estimates Johnson & Johnson’s intrinsic value at $432.38 per share. Given the current share price, this valuation implies the stock is trading at a 56.9% discount. According to traditional cash flow analysis, the stock appears significantly undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Johnson & Johnson is undervalued by 56.9%. Track this in your watchlist or portfolio, or discover 843 more undervalued stocks based on cash flows.

Approach 2: Johnson & Johnson Price vs Earnings

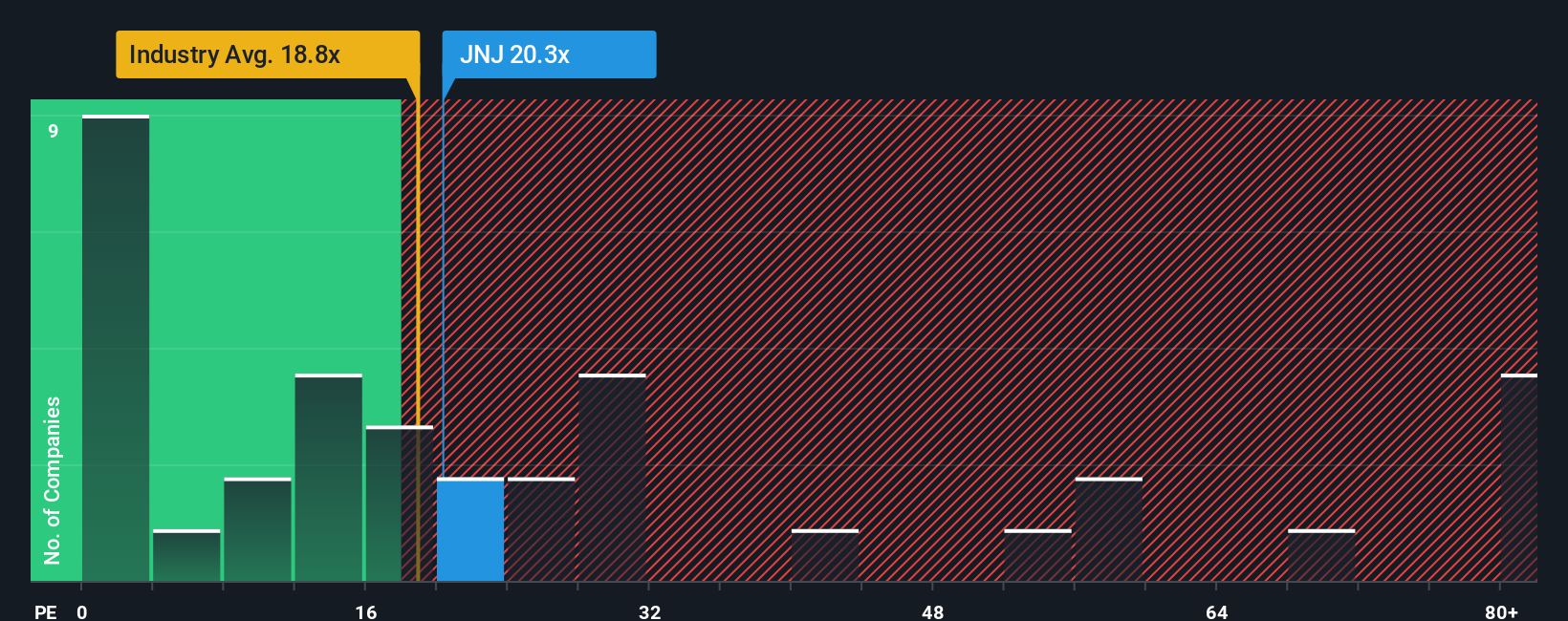

For profitable companies like Johnson & Johnson, the Price-to-Earnings (PE) ratio is a powerful tool for gauging valuation. The PE ratio shows how much investors are willing to pay per dollar of company earnings, making it relevant for mature businesses with consistent profits like Johnson & Johnson.

What makes a “fair” PE ratio depends on a company’s expected growth and its risks. Generally, higher growth and lower risk justify a higher PE, while slower growth or elevated risks should pull the ratio lower. Industry context and comparison with similar companies are also important for context.

Right now, Johnson & Johnson trades at a PE ratio of 17.87x. This is in line with the pharmaceuticals industry average of 17.87x and lower than the average for its peers at 20.75x. While these benchmarks provide useful context, the traditional approach of just comparing to industry and peers can sometimes miss important company-specific factors.

This is where Simply Wall St’s Fair Ratio comes in. The Fair Ratio for Johnson & Johnson is currently estimated at 26.12x, a proprietary assessment that incorporates specific factors like the company’s expected earnings growth, profitability, scale, industry, and risk profile. This goes beyond simple industry averages and provides a more tailored view of valuation.

Comparing the Fair Ratio of 26.12x to the current PE of 17.87x suggests Johnson & Johnson is trading well below what would be expected for a company of its caliber and outlook. This may indicate that the stock is undervalued at present.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Johnson & Johnson Narrative

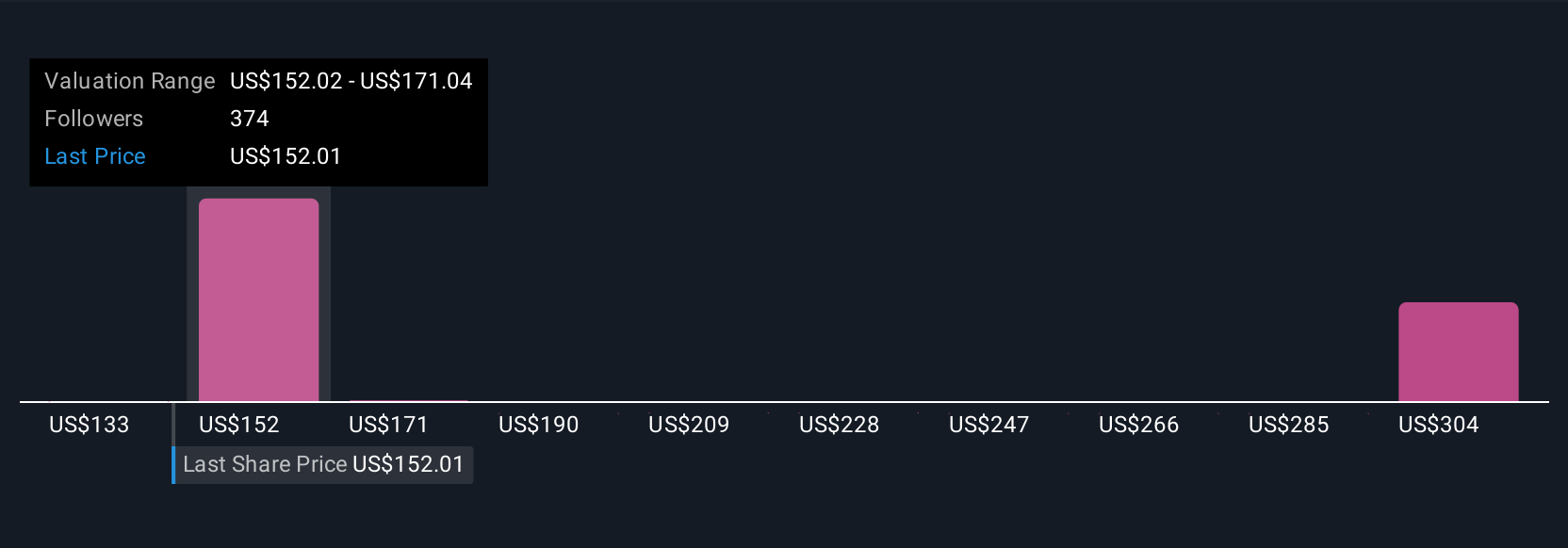

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your story, your perspective on what drives Johnson & Johnson’s future, turned into a concrete forecast of revenue, earnings, and margins that connects directly to a specific fair value for the stock.

Narratives let you go beyond just the numbers by linking your view of the business, such as expected drug launches, upcoming risks, or regulatory wins, to the financial data and a resulting fair price. This tool, available on Simply Wall St’s Community page and used by millions of investors, makes it quick and easy for anyone to build, share, or follow investment stories layered over up-to-date financial models.

What makes Narratives powerful is how they help you decide if the stock is a buy or sell by automatically comparing your fair value estimate to the latest market price, and updating whenever news or earnings announcements hit. For example, one Johnson & Johnson Narrative assumes ongoing success in innovative therapies and improving profit margins, leading to a bullish fair value of $200 per share, while a more cautious Narrative sees legal headwinds and pricing risk, resulting in a fair value closer to $155.

This means you can clearly see how different assumptions drive different outlooks, so you can invest with conviction in the story that best matches your view.

Do you think there's more to the story for Johnson & Johnson? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com