Is Volkswagen’s Recent EV Push Signaling a New Opportunity for Investors in 2025?

- Wondering if Volkswagen stock is a hidden bargain or a value trap? You are not alone, as many investors are eyeing its current price for signs of potential opportunity.

- Volkswagen’s share price has dipped slightly by 0.3% over the past week and 2.3% over the last month. However, it is up 4.4% year-to-date and 10.3% over the past twelve months, which may indicate renewed optimism or changing risk perceptions in the auto sector.

- Recent headlines have focused on Volkswagen’s ambitious push into electric vehicles and strategic partnerships. This has given markets fresh reasons to re-evaluate the company's growth prospects. At the same time, ongoing supply chain discussions and evolving regulatory landscapes are keeping investors watchful.

- With a healthy valuation score of 5 out of 6, Volkswagen appears undervalued by most standard checks. Yet there may be more to the story than these numbers suggest. The following discussion explores the main valuation approaches to help get to the heart of the company’s true worth.

Approach 1: Volkswagen Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to today, which helps assess whether the share price reflects its true worth. For Volkswagen, this model uses recent and forecasted free cash flows to determine intrinsic value.

Currently, Volkswagen’s free cash flow (FCF) is negative, at around -€10.94 Billion, reflecting recent investment and cash outflows. Analysts predict growth in FCF, with projections reaching approximately €14.16 Billion by 2029. Over the next 10 years, estimates suggest a steady climb in cash flows, potentially totaling €28.26 Billion in 2035, though many of these later figures are extrapolated beyond analyst coverage.

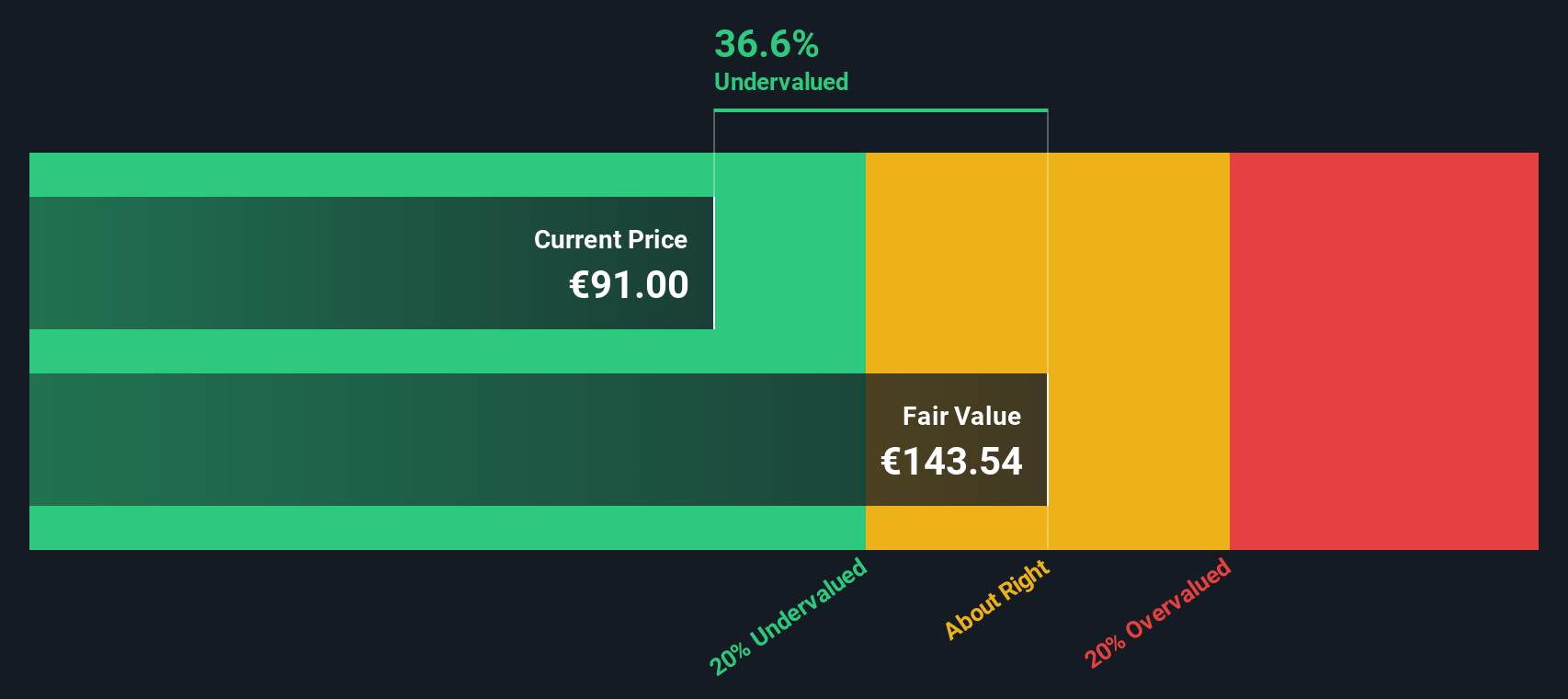

Based on this DCF analysis, Volkswagen’s intrinsic value is calculated at €458.83 per share. Given the implied 80.1% discount to current trading levels, the model suggests the stock is significantly undervalued according to future cash flow prospects.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Volkswagen is undervalued by 80.1%. Track this in your watchlist or portfolio, or discover 843 more undervalued stocks based on cash flows.

Approach 2: Volkswagen Price vs Earnings (PE Ratio)

The price-to-earnings (PE) ratio is often a reliable way to value large, profitable companies like Volkswagen, as it directly links the share price to the company's actual earnings. For industries with steady profits, the PE ratio gives investors a quick snapshot of how much they are paying for each euro of earnings, which can be helpful when comparing companies or tracking historical value.

What constitutes a "normal" or "fair" PE ratio is influenced by factors such as growth potential, business risks, and expected profit margins. Higher-growth companies or those with strong balance sheets typically command higher PE ratios, while higher risks or volatile earnings can pull that number lower.

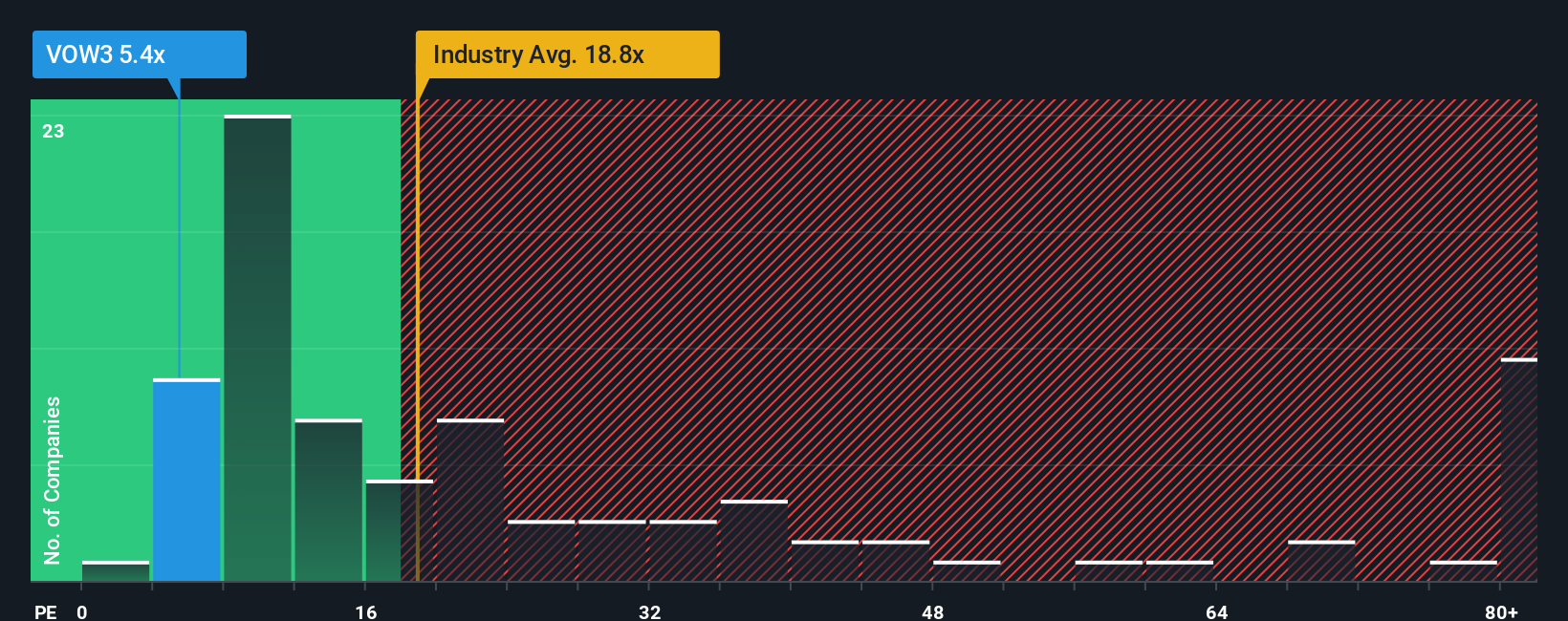

Volkswagen’s current PE ratio sits at 6.79x, noticeably lower than the auto industry average of 18.22x and the average for its closest peers, which is 18.02x. At first glance, this steep discount suggests Volkswagen might be undervalued compared to its competitors.

This is where Simply Wall St’s proprietary "Fair Ratio" comes in. Unlike standard benchmarks, the Fair Ratio reflects Volkswagen’s individual profile by factoring in expected earnings growth, risks, profit margins, size, and the realities of its industry. This tailored approach offers a more nuanced benchmark than a simple industry or peer comparison.

For Volkswagen, the Fair Ratio stands at 17.85x, well above the current multiple. The sizable gap between the Fair Ratio and Volkswagen’s trailing PE suggests the stock could be significantly undervalued on earnings fundamentals alone.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Volkswagen Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is more than just numbers; it is your story or perspective about a company, based on your own assumptions around its future revenue, earnings and margins, and the corresponding fair value you derive from them.

Narratives connect the dots between Volkswagen’s real-world situation, your personal investment thesis, and financial forecasts, making it clear whether your expectations align with the current market price. This approach is designed to be accessible to every investor and is available right now on Simply Wall St’s Community page, where millions of investors craft and share their own outlooks.

With Narratives, you can quickly see when Volkswagen’s fair value, calculated from your expectations or the community’s, differs from its current price, helping inform buy or sell decisions. Plus, since Narratives are updated automatically with every major news story or earnings release, your outlook stays as current as possible.

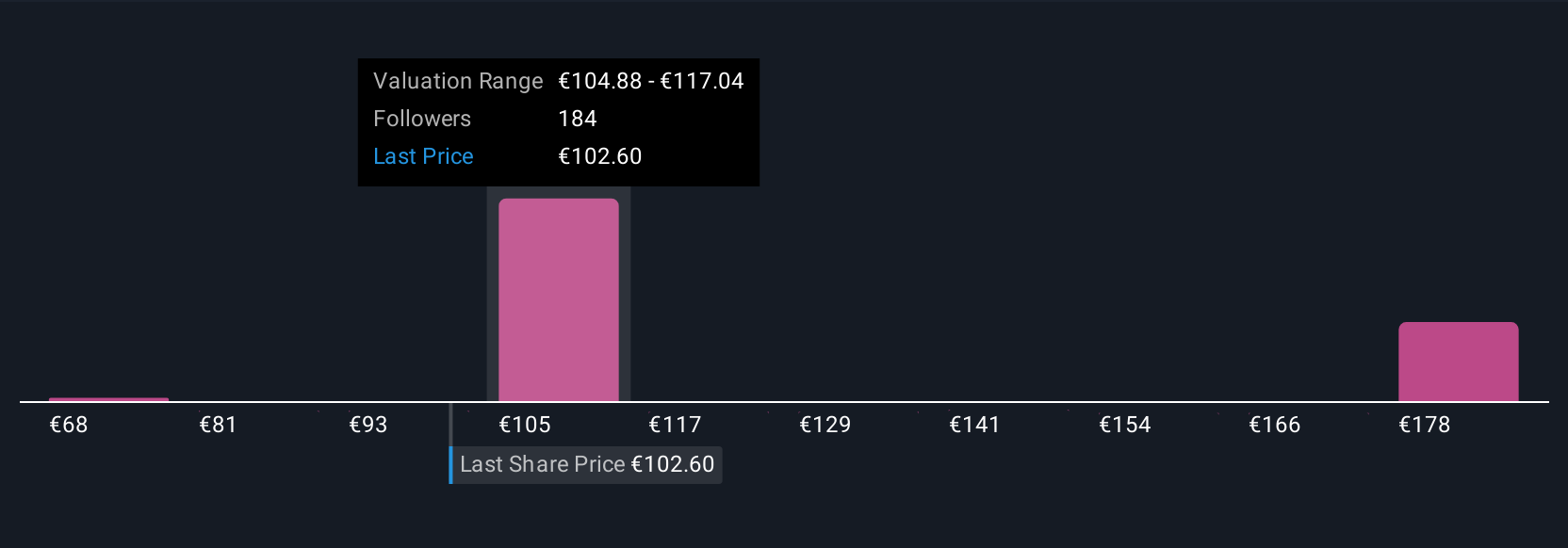

For example, one Narrative for Volkswagen sees the stock as significantly undervalued, with a fair value of €111 based on continued electrification, margin recovery, and global expansion. Another views it as a value trap, with a low fair value of €68 on the basis of strategic missteps, market pressure, and muted profit outlook, reminding us that every investor’s “story” can have a very different ending.

For Volkswagen, we’ll make it really easy for you with previews of two leading Volkswagen Narratives:

- 🐂 Volkswagen Bull Case

Fair Value: €111.13

Undervalued by: 17.96%

Expected Revenue Growth: 2.97%

- Expansion into electrified vehicles, digital services, and operational restructuring is positioning Volkswagen for renewed growth and improved margins.

- Strategic local production, partnerships, and cost optimization are mitigating geopolitical and supply chain risks. This supports profitability and resilience.

- Analysts' consensus price target is 12.8% above the current share price. This reflects optimism about margin recovery, premium brand focus, and new recurring revenue streams.

- 🐻 Volkswagen Bear Case

Fair Value: €68.40

Overvalued by: 33.38%

Expected Revenue Growth: 1.0%

- Volkswagen faces sustained strategic headwinds, including organizational complacency, excessive reliance on China, and missed opportunities in the EV market.

- Recent profit declines, lackluster non-German market share, and management’s decision to delay margin improvement targets raise doubts over future growth.

- Near-term negative outlook is compounded by regulatory challenges and delayed new segment launches. This makes the current price appear too high relative to more conservative fair value estimates.

Do you think there's more to the story for Volkswagen? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com