How Should Investors View Arista Networks After Big Stock Surge and Cybersecurity Partnerships?

- Thinking about whether Arista Networks is a good value right now? You are not alone, as savvy investors are constantly asking themselves what the price tag really says about the company's future.

- Over the past year, Arista Networks' stock has soared 59.6% and is up a staggering 863.6% over the last five years, with recent momentum including a 0.5% climb in the last week and 8.3% over the past month.

- Part of this excitement comes from the company's ongoing advances in cloud networking, grabbing headlines with steady innovations in high-speed data solutions that have helped fuel optimism. Recent cybersecurity partnerships have also been in the spotlight, reinforcing Arista's role in the fast-evolving tech infrastructure space.

- However, despite the buzz, Arista Networks scores just 1 out of 6 on our valuation checks, suggesting some caution is warranted. In this article, we will break down how different valuation methods view the stock, and at the end, spotlight an approach that could help you spot opportunities others might miss.

Arista Networks scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Arista Networks Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and then discounting them back to today's value, reflecting the time value of money. This approach helps investors determine what a company's shares might truly be worth, based on how much cash the business can generate in the coming years.

For Arista Networks, the latest reported Free Cash Flow stands at approximately $4.0 Billion. According to analyst estimates and Simply Wall St extrapolations, annual Free Cash Flow is expected to grow steadily over the next decade and reach a projected $7.7 Billion by 2035. Actual analyst forecasts are available up to 2028, and projections beyond that are derived based on recent growth trends.

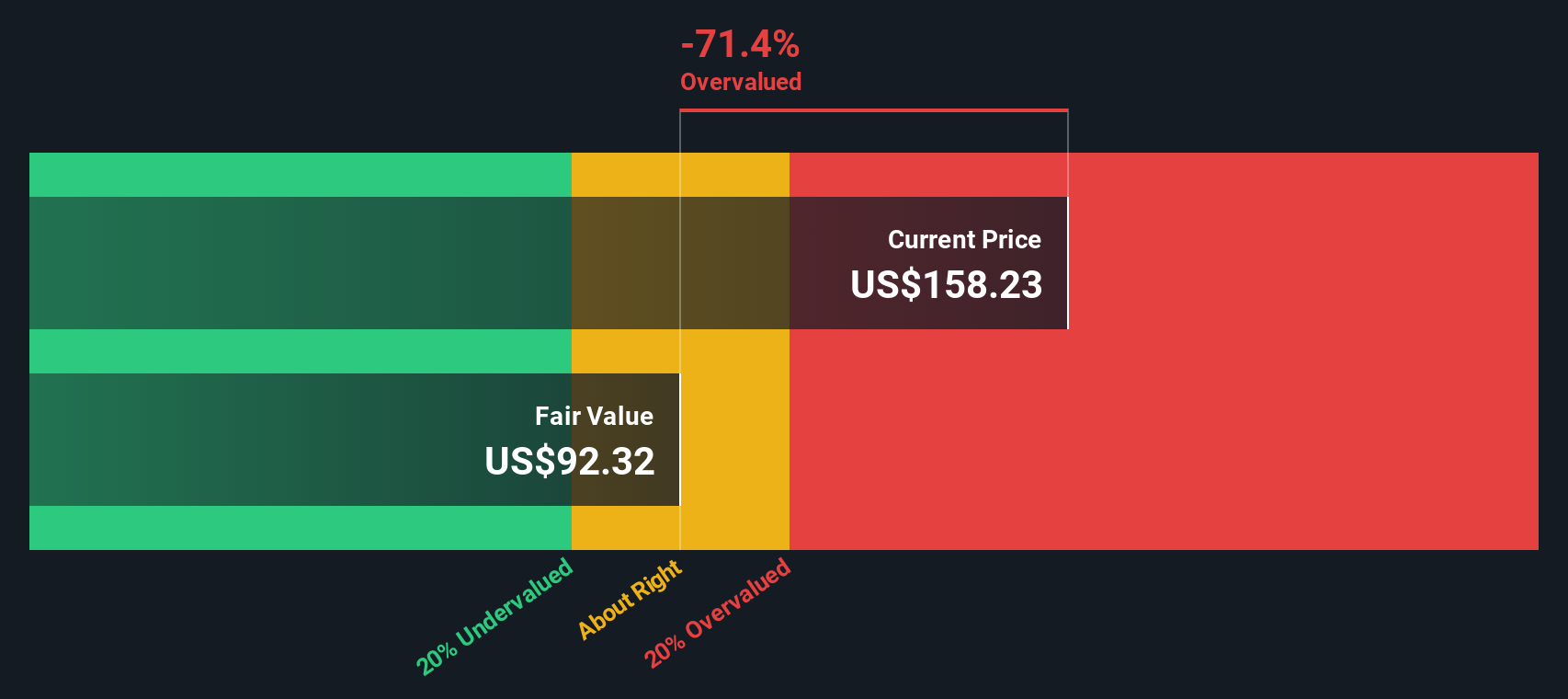

Based on this two-stage Free Cash Flow to Equity model, the intrinsic value per share is calculated at $92.27. With Arista’s stock currently trading well above this figure, the DCF model suggests the market is valuing the company at a steep premium, which implies the stock is around 70.8% overvalued.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Arista Networks may be overvalued by 70.8%. Discover 842 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Arista Networks Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric, especially for profitable companies like Arista Networks. It helps investors gauge if a stock is expensive or cheap relative to its earnings. Generally, companies with strong growth prospects or lower risk command higher PE ratios, while sluggish or riskier businesses trade at lower multiples.

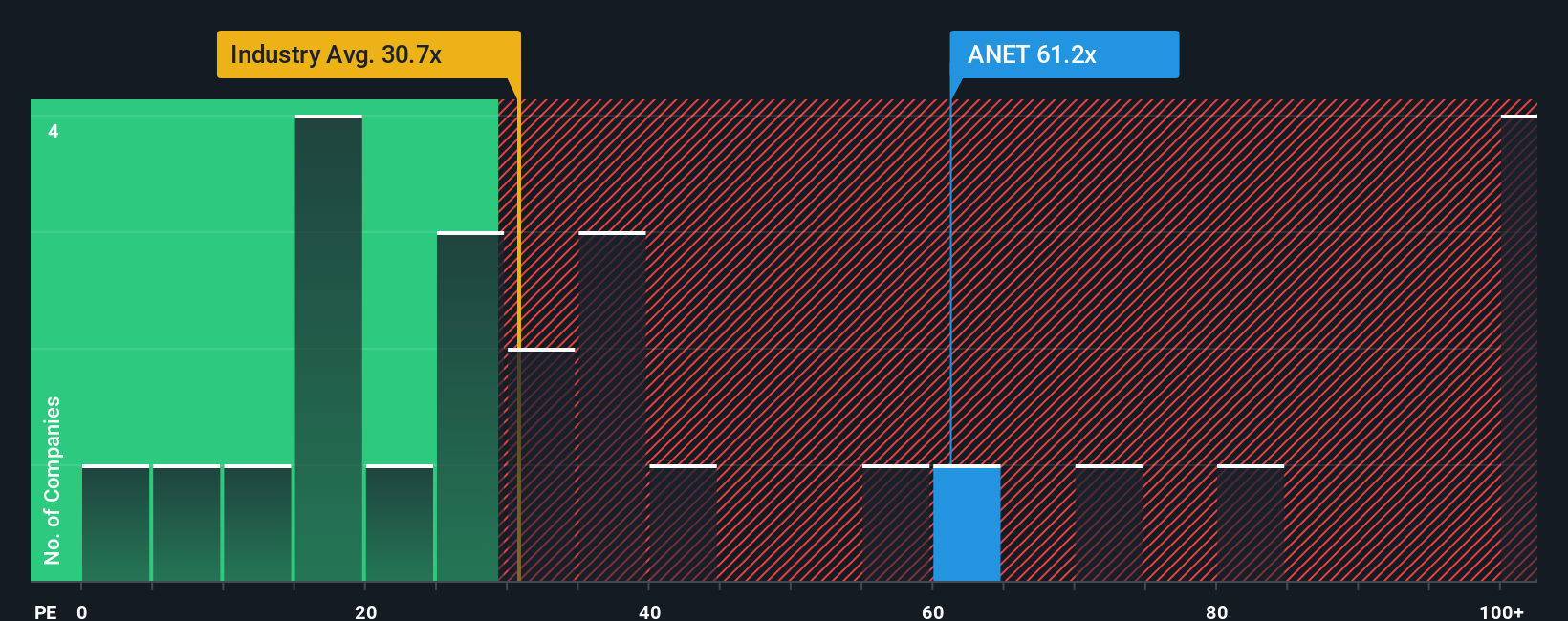

Currently, Arista Networks is trading at a PE ratio of 60.9x. This is well above the industry average for communications companies, which is 31.1x, and higher than the average among its direct peers at 78.8x. However, simple peer or industry comparisons can be misleading, since both growth expectations and business risks affect what constitutes a “fair” PE for any company.

Simply Wall St's Fair Ratio for Arista is 46.1x. Unlike plain benchmarks, this proprietary metric incorporates factors like Arista’s earnings growth, profit margins, market cap, industry dynamics, and company-specific risks to determine an appropriate multiple. Because it weighs what makes Arista unique, it offers a sharper lens than peer or sector averages alone.

Arista’s actual PE of 60.9x is noticeably higher than its Fair Ratio of 46.1x, signaling that the stock is currently trading at a premium based on its fundamentals and expected growth profile.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Arista Networks Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, a powerful, story-driven framework that connects what you believe about a company to the numbers behind its valuation.

A Narrative is your own perspective about a company's future, combining your view of the business, its strengths, opportunities, and risks, with specific financial forecasts like future revenue, profit margins, and fair value.

Instead of viewing financial models in isolation, Narratives let you anchor your investing decisions in the “why” behind the numbers: your assumptions, expectations, and the real-world trends you see shaping the company’s trajectory.

On Simply Wall St’s Community page (trusted by millions of investors), you can quickly browse and create Narratives for Arista Networks, comparing not only analysts’ and other investors’ fair value estimates, but also the story and assumptions driving each one.

Narratives update automatically with each new earnings report or breaking news, helping you stay up to date and confident about your view, whether you’re deciding to buy, hold, or sell as the gap between fair value and price shifts.

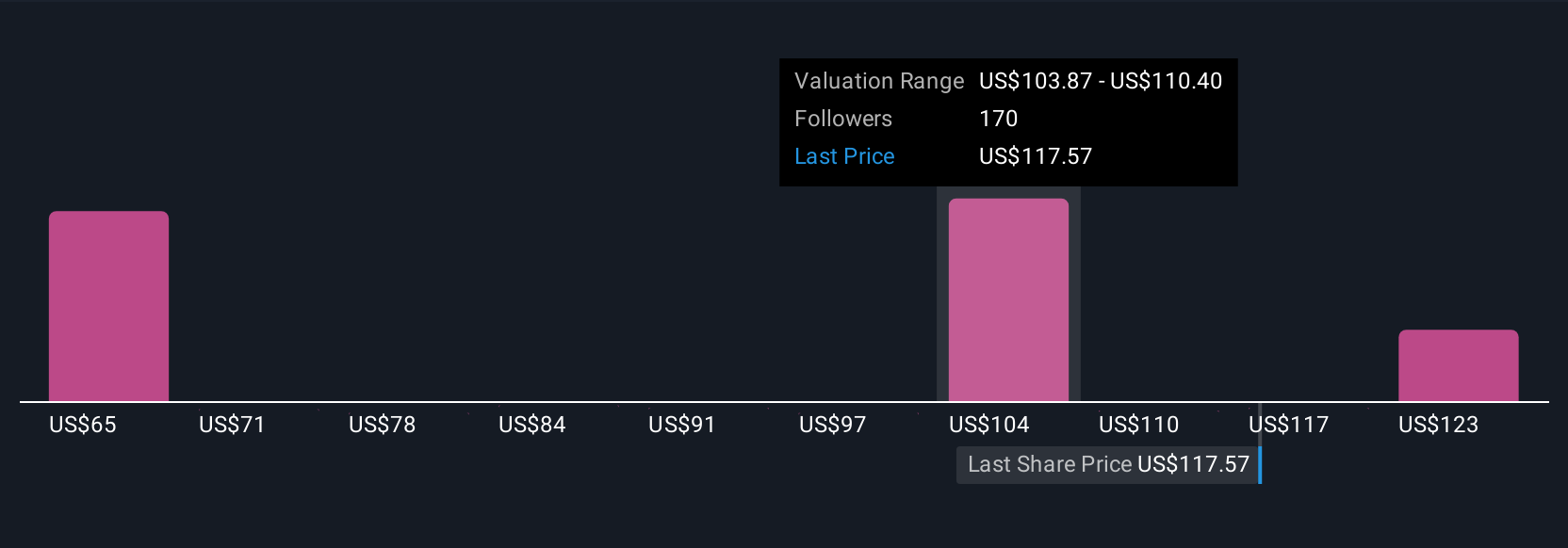

For example, some investors see Arista Networks as fairly valued at around $76, citing realistic but ambitious free cash flow growth and near-zero debt, while others project a much higher fair value of $160 by assuming accelerated AI-driven revenue growth and robust market leadership.

For Arista Networks, we'll make it really easy for you with previews of two leading Arista Networks Narratives:

Fair Value: $159.80

Currently trading at about 1.4% below this fair value

Revenue Growth Assumption: 20.8%

- Arista’s leadership in high-bandwidth, AI-focused networking is expected to drive sustained share gains as the industry shifts toward open standards and scalable architectures.

- Expansion into enterprise markets and a growing focus on software-driven solutions are seen boosting recurring revenues and long-term earnings stability.

- Key concerns include dependence on a few large customers and intensifying competition from major rivals, along with geopolitical and supply chain risks that could impact growth.

Fair Value: $127.06

Currently trading at about 24.1% above this fair value

Revenue Growth Assumption: 15.0%

- Arista has quickly disrupted legacy competition in high-speed internet switches, maintaining high customer satisfaction through strong alignment of hardware and software.

- Financial discipline is a highlight, with zero debt and a strong return on equity, reinforcing the argument that it is a robust, well-run company.

- Despite strengths, the current market price implies an aggressive growth trajectory. Some observers believe the stock is trading at a premium to realistic fair value estimates based on free cash flow growth targets.

Do you think there's more to the story for Arista Networks? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com