Why Westlake (WLK) Is Down 13.7% After a $782 Million Loss and Goodwill Impairment

- Westlake Corporation recently reported a third-quarter 2025 net loss of US$782 million, largely due to a US$727 million goodwill impairment in its North American chlorovinyls business and reduced sales in its Performance and Essential Materials segment.

- Despite ongoing investments in growth projects and cost reduction efforts, Westlake continues to face near-term challenges from lower demand, falling sales prices, and restructuring costs.

- We’ll explore how Westlake’s significant goodwill impairment and third-quarter loss reshape its investment narrative and future prospects.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Westlake Investment Narrative Recap

To hold Westlake shares today, you need to believe its core advantages in infrastructure and diversified materials can overcome sharp chemical price headwinds, cost pressures, and ongoing restructuring. The recent US$727 million goodwill impairment and disappointing earnings reaffirm softness in the Performance and Essential Materials segment but do not materially alter the main long-term driver: US municipal infrastructure spending supporting the Housing and Infrastructure Products business; however, persistent weak global demand for core chemicals remains the most pressing risk.

Among recent announcements, Westlake’s Q3 2025 results show a 9% year-on-year drop in revenue and a net loss of US$782 million, underscoring the operational drag from oversupply and demand challenges. This weak performance aligns closely with the key short-term risks identified, bringing renewed focus to structural margin pressures in chemicals while highlighting the relative resiliency of infrastructure-linked business lines.

By contrast, what investors might miss is how prolonged chemical overcapacity could continue to pressure earnings and...

Read the full narrative on Westlake (it's free!)

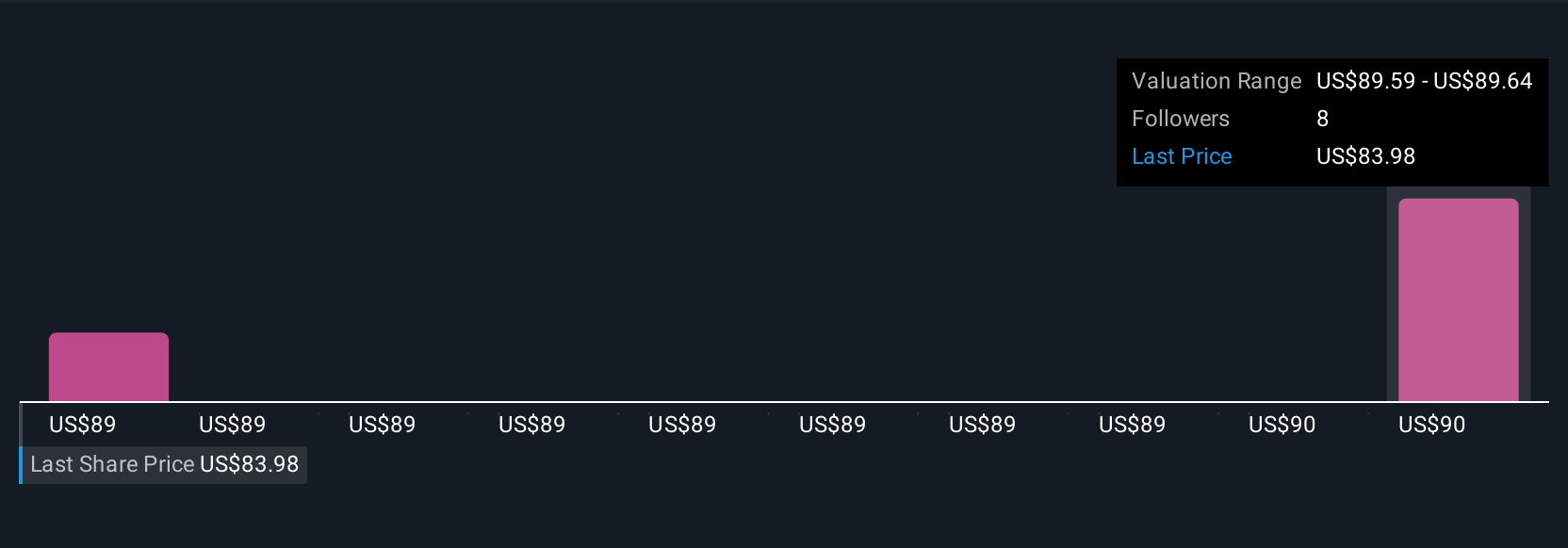

Westlake's narrative projects $13.0 billion in revenue and $893.8 million in earnings by 2028. This requires 3.5% yearly revenue growth and a $960.8 million earnings increase from -$67.0 million today.

Uncover how Westlake's forecasts yield a $88.43 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members submitted two fair value estimates for Westlake ranging from US$88.43 to US$98.88. While these opinions point to a significant discount to current levels, the ongoing global oversupply in core chemical chains could have broad impacts on future returns, explore these alternative viewpoints to see how opinions differ.

Explore 2 other fair value estimates on Westlake - why the stock might be worth as much as 44% more than the current price!

Build Your Own Westlake Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Westlake research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com