COSCO SHIPPING Holdings (SEHK:1919): Evaluating Valuation After Lower Revenue and Profit in Q3 Results

COSCO SHIPPING Holdings (SEHK:1919) has just published its unaudited third quarter earnings, showing declines in both revenue and net income for the nine months ending September 30, 2025. Investors are watching these results closely.

See our latest analysis for COSCO SHIPPING Holdings.

Despite posting softer revenue and profit figures, COSCO SHIPPING Holdings has maintained some positive momentum, with a 1-month share price return of nearly 12% and a 1-year total shareholder return of over 22%. The stock’s performance points to growing interest, even as long-term growth remains a key focus for investors.

If this shift has you curious about broader trends in transport and logistics, now is an ideal time to broaden your search and discover fast growing stocks with high insider ownership

With earnings trending down and the share price still climbing, investors are left to wonder if COSCO SHIPPING Holdings is undervalued or if the market has already factored in the company’s future prospects. Is there a compelling buying opportunity here?

Price-to-Earnings of 5x: Is it justified?

COSCO SHIPPING Holdings trades at a price-to-earnings (P/E) ratio of 5x, which is well below both the peer average and the wider industry. The most recent close was HK$13.49, supporting the view that the shares currently present strong value on this measure.

The price-to-earnings ratio shows how much investors are willing to pay for each dollar of earnings. This is a popular valuation gauge, especially for established companies like COSCO SHIPPING Holdings in the shipping sector, where profit cycles can be volatile but meaningful. A low P/E relative to peers may indicate the market is underestimating the company’s future earnings potential or pricing in too much risk.

Compared to the Asian Shipping industry, where the average P/E stands at 10.9x, COSCO SHIPPING Holdings looks outright inexpensive. Even against its peers’ average P/E of 8.1x, the valuation gap is clear. Relative to the estimated fair P/E of 6.4x, the current multiple leaves ample headroom for sentiment to improve and the stock to re-rate upwards if earnings stabilize or recover.

Explore the SWS fair ratio for COSCO SHIPPING Holdings

Result: Price-to-Earnings of 5x (UNDERVALUED)

However, softer revenue growth and sharply lower annual net income may weigh on sentiment if recovery remains slow. This could test confidence in a value thesis.

Find out about the key risks to this COSCO SHIPPING Holdings narrative.

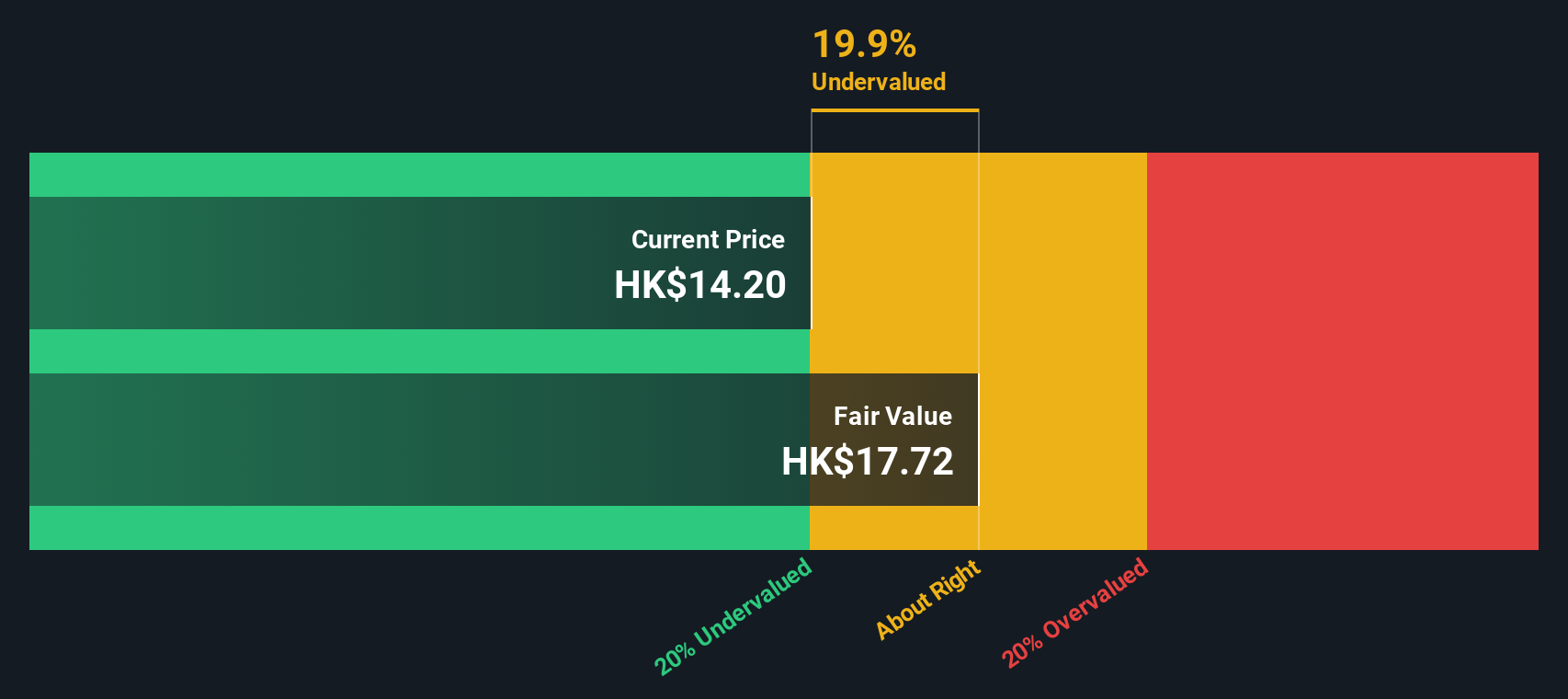

Another View: SWS DCF Model

While the P/E ratio suggests COSCO SHIPPING Holdings is undervalued, our SWS DCF model presents an even starker picture. The current share price sits well below our estimated fair value of HK$33.12, which implies the market may be overlooking significant long-term upside. Could this gap be an opportunity, or is there something the DCF model misses?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out COSCO SHIPPING Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 836 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own COSCO SHIPPING Holdings Narrative

If you see things differently or want to dig deeper on your own, you can easily construct your own take in just a few minutes. Do it your way

A great starting point for your COSCO SHIPPING Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Give your strategy a serious upgrade by tapping into some of the most compelling stock themes identified by our powerful Simply Wall St Screener. Uncover new opportunities others might miss, and take control of your investing future before the next big move happens.

- Maximize your income potential and target reliable yields by tracking these 20 dividend stocks with yields > 3% that consistently offer strong financial returns.

- Position yourself for leadership in tomorrow's healthcare breakthroughs by examining these 33 healthcare AI stocks that leverage artificial intelligence in medicine and biotech innovation.

- Accelerate your portfolio’s growth story with these 836 undervalued stocks based on cash flows that appear overlooked based on cash flow fundamentals and show promise for strong upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com