Aozora Bank (TSE:8304) Valuation Check: Is the Recent Slide Creating Opportunity?

Aozora Bank (TSE:8304) shares have seen some movement recently. Investors are keeping an eye on the stock’s performance over the past month, particularly in light of its year-to-date decline and the broader economic environment facing Japanese banks.

See our latest analysis for Aozora Bank.

Aozora Bank’s share price has faced real pressure lately, notching a 6.2% decline over the past month and leaving its year-to-date return at -11.7%. That ongoing drop follows several challenging quarters for the broader Japanese banking sector. Even with its five-year total shareholder return still up 56.3%, recent momentum seems to be fading rather than building.

If you’re on the lookout for a fresh opportunity, now is the perfect moment to expand your search and discover fast growing stocks with high insider ownership

With shares down double digits this year despite rising net income, investors now face a key question: is Aozora Bank currently undervalued, or has the recent dip simply matched expectations for its future growth?

Price-to-Earnings of 15.8x: Is it justified?

Aozora Bank is currently trading at a price-to-earnings (P/E) ratio of 15.8x, which stands notably above the average for Japanese banks. At its last close of ¥2205.5, investors are paying a premium compared to both industry standards and implied fair value multiples.

The price-to-earnings ratio measures how much investors are willing to pay today for a unit of the company’s earnings. In banking, it is a quick gauge of market expectations for future profit growth and risk.

Despite turning profitable this year and forecasted earnings growth, Aozora is priced not only above sector peers (11.5x P/E for the Japanese banks industry) but also above its estimated fair P/E (13.6x). This suggests a heightened market optimism that may be outpacing the company’s recent track record and industry trends. Should sentiment revert to sector norms, the stock could face further downward pressure.

Explore the SWS fair ratio for Aozora Bank

Result: Price-to-Earnings of 15.8x (OVERVALUED)

However, slower revenue growth and a recent drop below analyst targets remain risks that could challenge any near-term rebound for Aozora Bank shares.

Find out about the key risks to this Aozora Bank narrative.

Another View: What Does a DCF Model Say?

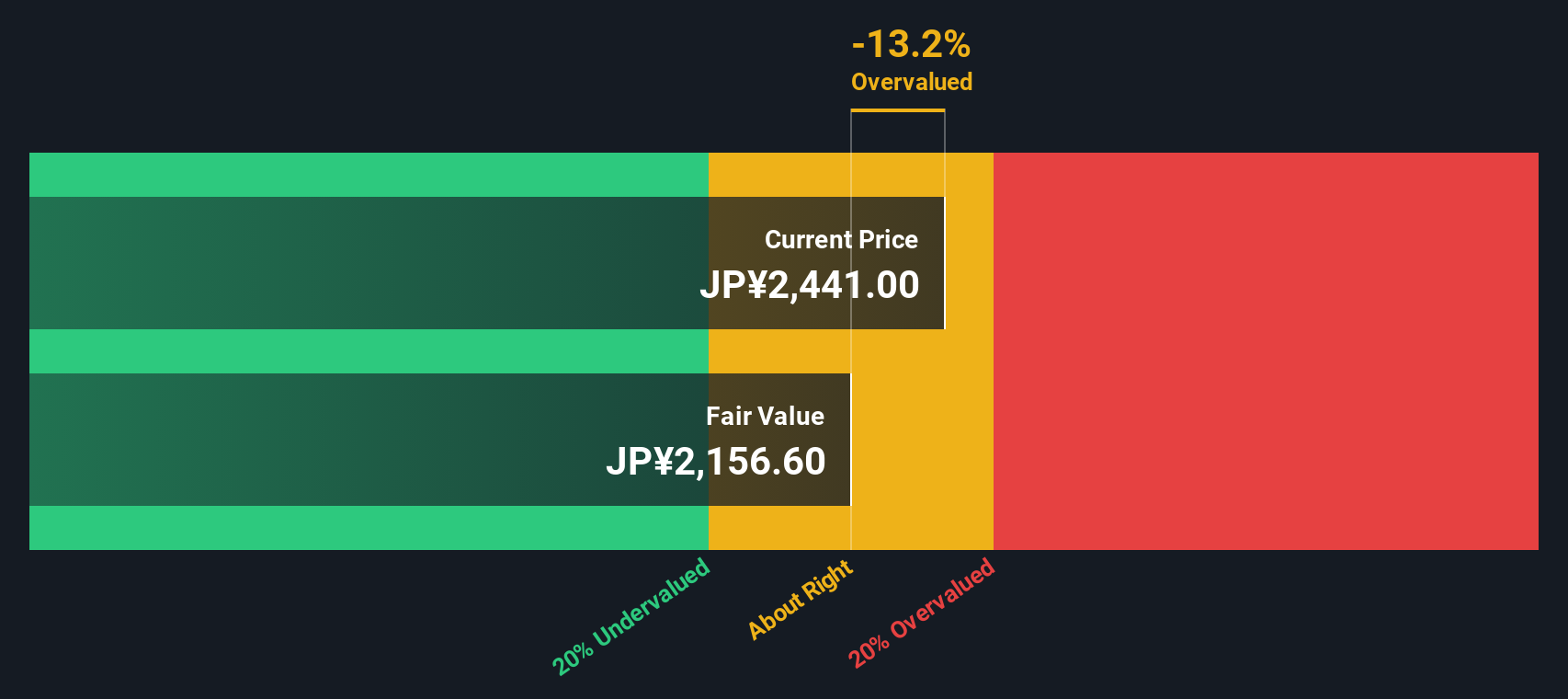

Taking a different approach, our SWS DCF model estimates Aozora Bank’s fair value at ¥2,058.26. This is below the current share price of ¥2,205.5, which suggests the stock may actually be overvalued. This offers a different perspective compared to traditional multiples. Which lens gives you more confidence for the road ahead?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aozora Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 840 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Aozora Bank Narrative

If you see the story differently, or prefer to dig into the numbers yourself, you can craft your own view in just a few minutes. Do it your way

A great starting point for your Aozora Bank research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Strike while opportunities are hot by tapping into top-performing themes. Don’t risk missing quality stocks that smart investors are tracking right now.

- Cement your portfolio’s foundation with income by accessing these 22 dividend stocks with yields > 3% delivering strong yields well above market averages.

- Ride the momentum in innovation by evaluating these 27 AI penny stocks at the forefront of artificial intelligence breakthroughs with real-world impact.

- Seize undervalued gems before the crowd catches on and secure growth potential with these 840 undervalued stocks based on cash flows based on the latest cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com