Southwest Airlines (LUV): Exploring Valuation After Recent Share Price Fluctuations

Southwest Airlines (LUV) shares have seen some movement recently, catching the attention of investors interested in the airline sector. With shifting travel demand and industry-wide changes, many are considering how the company’s stock could perform in this environment.

See our latest analysis for Southwest Airlines.

The latest moves in Southwest’s share price reflect a cautious sentiment, with a 1-day lift of 0.70% contrasted by a 7-day dip of nearly 6%. While the stock’s 1-year total shareholder return sits just above break-even, longer-term returns still lag. This suggests recent momentum is not yet translating into a sustained turnaround.

If you want to see which other airline and travel stocks might be showing stronger signals, check out our complete list with the See the full list for free..

With its stock still lagging over longer timeframes and trading below many analyst price targets, the question arises: Is Southwest Airlines undervalued at current levels, or is the market already pricing in any rebound in growth?

Most Popular Narrative: 10% Undervalued

With Southwest Airlines’ widely followed fair value estimate at $33.76, the stock’s last close of $30.30 points to noticeable upside if the narrative plays out. The story behind this difference centers on expectations that margin and revenue growth will outpace industry trends.

Streamlined operations through a decrease in turn time at 19 major stations, alongside a leading industry on-time performance, suggests potential operational efficiency improvements. This should help optimize costs and lead to an improvement in net margins and earnings.

Here’s what the narrative doesn’t reveal upfront: a pivotal set of financial projections underpin this valuation, involving margin transformation and a future earnings leap. Want to see the bold assumptions and divisive forecasts that analysts rely on to set this fair value? Dive in to uncover the details shaping Southwest’s investment case.

Result: Fair Value of $33.76 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain, including uncertain booking trends and possible aircraft delivery delays. These factors could challenge Southwest’s margin recovery and long-term growth prospects.

Find out about the key risks to this Southwest Airlines narrative.

Another View: Multiples Raise Caution

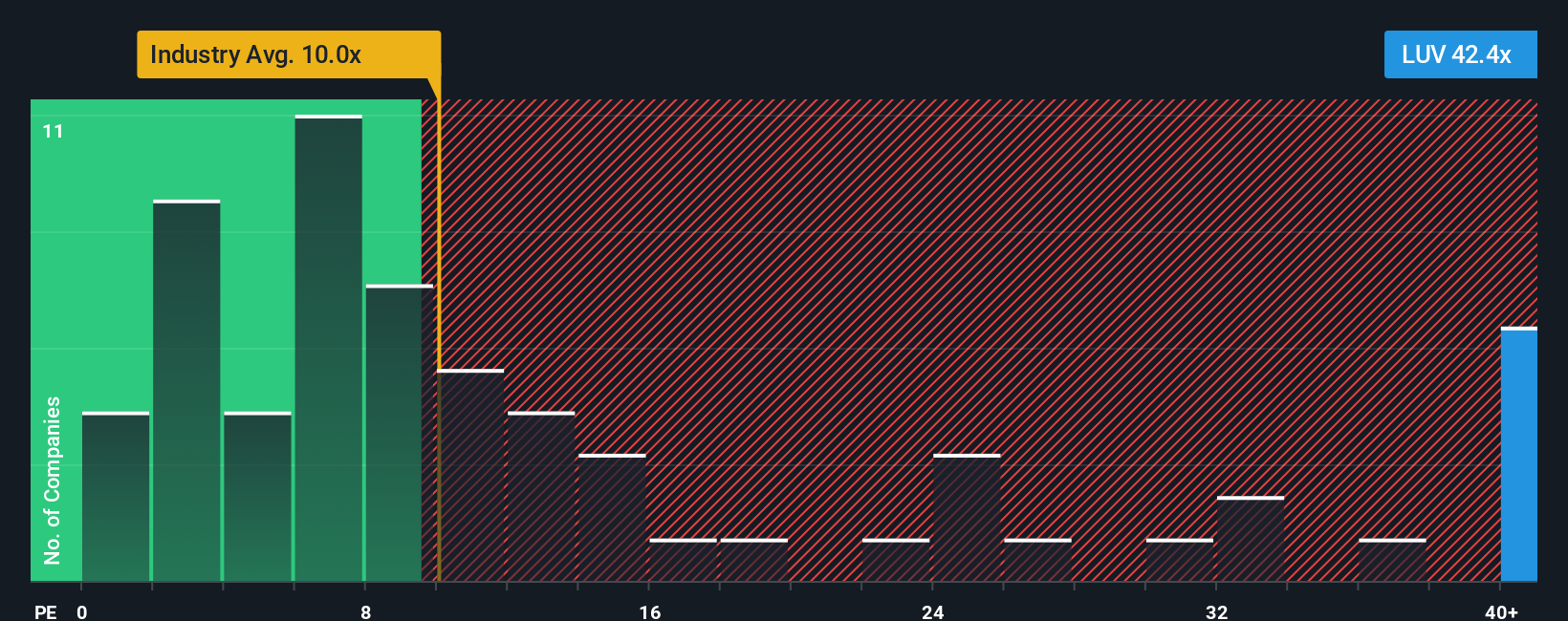

Looking at Southwest Airlines through the lens of earnings multiples paints a different picture. The stock trades at a lofty 41.3 times earnings, while both the industry and its peers average under 10 times earnings. The fair ratio is even lower at 27.9. This big gap means investors are paying a premium, which could signal extra risk or hidden resilience.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Southwest Airlines Narrative

If you think there’s more to the story or want to dig into the numbers yourself, you can craft your own take in just a few minutes. Do it your way.

A great starting point for your Southwest Airlines research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for Even More Smart Investment Ideas?

Don’t just stop at Southwest. Seek out exceptional growth, hidden value, or future trends with a few minutes in the Simply Wall Street Screener. You’ll thank yourself later for not missing out!

- Capitalize on tomorrow’s tech revolution by jumping into the world of artificial intelligence with these 26 AI penny stocks poised for explosive advancement.

- Catch strong cash flow bargains by sizing up these 839 undervalued stocks based on cash flows that the market may have overlooked.

- Build steady income streams and strengthen your portfolio with these 22 dividend stocks with yields > 3% offering attractive yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com