Is Dropbox Fairly Priced After Recent AI-Powered Product Push?

- Wondering if Dropbox stock is a deal right now? You are not alone. The answer might surprise you if you look past just the headline price.

- Despite a subtle dip of 1.4% over the past month, Dropbox has posted an impressive 11.6% return in the past year and 51.5% growth over five years. This performance has caught the attention of both growth seekers and cautious optimists.

- Recently, Dropbox has been in the news for its continued push into AI-powered features and strategic partnerships. These efforts are aimed at keeping its platform front and center for businesses. These developments are exciting investors, as they suggest the company could be positioning itself for another stage of expansion.

- When it comes to valuation, Dropbox scores a solid 5 out of 6 on our major value checks, indicating that the stock looks compelling against several key metrics. There are different ways to assess a stock’s true value, and we will explore these approaches next, including one perspective you may not have considered.

Find out why Dropbox's 11.6% return over the last year is lagging behind its peers.

Approach 1: Dropbox Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates the intrinsic value of a company by projecting its future cash flows and discounting them back to today's dollars. This approach aims to capture the true worth of a business by looking at the money it is expected to generate for shareholders over time, rather than simply focusing on recent earnings or market moves.

For Dropbox, the DCF model uses its most recent annual Free Cash Flow (FCF) of $878.6 million as the starting point. Analyst predictions suggest modest growth ahead, with FCF projected to reach $955.4 million by 2027. Since detailed estimates are only available for the next few years, Simply Wall St has extrapolated the company’s cash flows through 2035, with steady increases anticipated each year. All values are reported in US dollars.

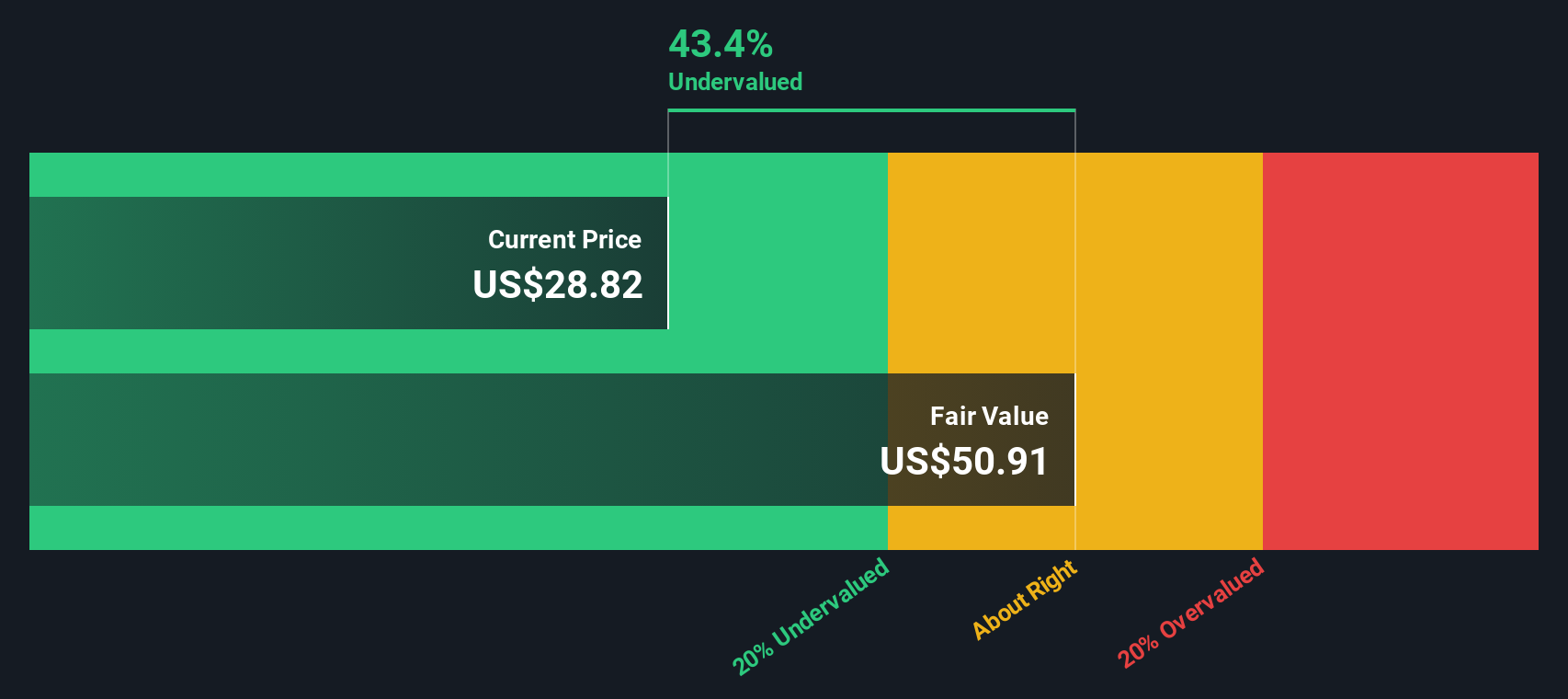

Based on these projections, the DCF model calculates Dropbox’s fair value at $51.05 per share. With Dropbox currently trading at a notable 43.2% discount to this estimate, the model signals the stock may be significantly undervalued relative to its future cash-generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dropbox is undervalued by 43.2%. Track this in your watchlist or portfolio, or discover 840 more undervalued stocks based on cash flows.

Approach 2: Dropbox Price vs Earnings

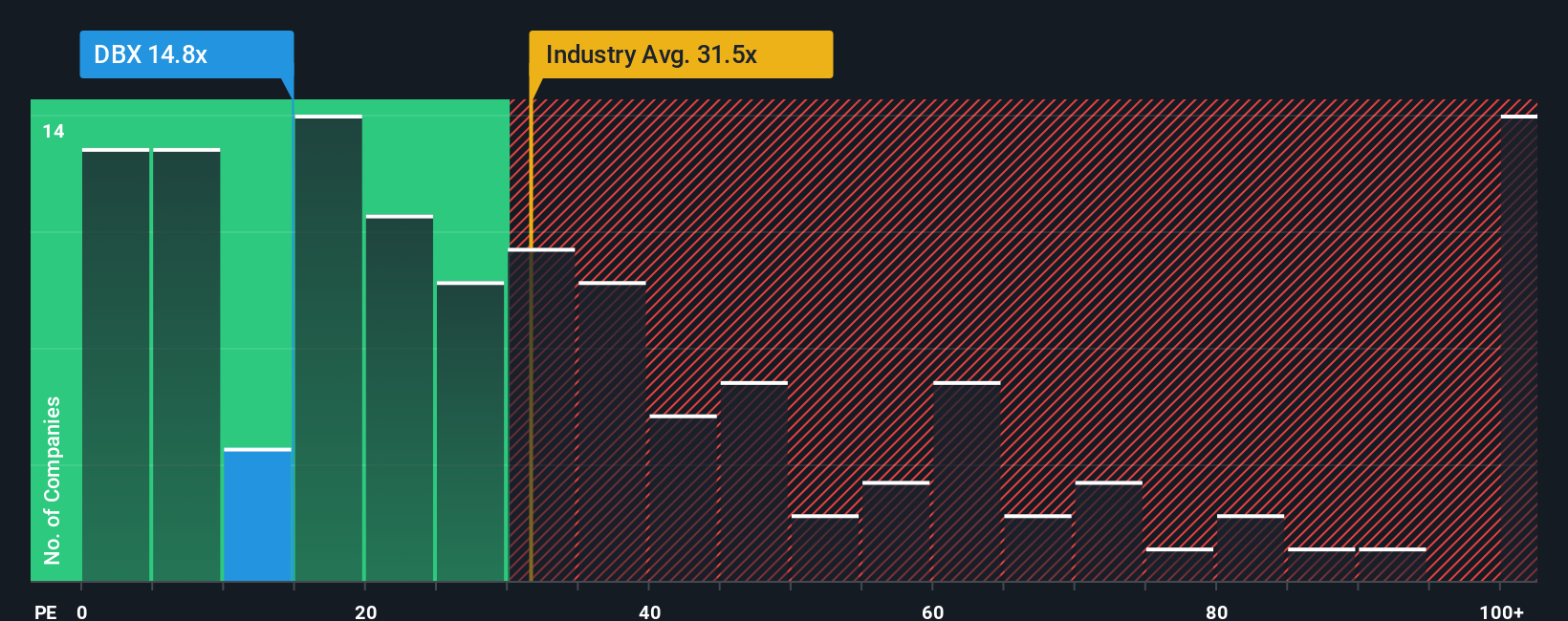

The price-to-earnings (PE) ratio is a widely used valuation metric for profitable technology companies like Dropbox. It tells investors how much they are paying for each dollar of a company's current earnings, making it especially relevant for businesses that are consistently posting profits. A PE ratio helps gauge whether a stock is priced attractively compared to its earnings power.

It is important to remember that what counts as a "normal" or "fair" PE ratio is shaped by several factors. Higher growth expectations or lower perceived risks typically command higher PE multiples, while slower growth or higher risk can suppress them. The state of the broader software industry and recent market trends can also sway what investors view as fair.

Dropbox is currently trading at a PE ratio of 16.1x, which is considerably below both the industry average of 34.9x and the peer average of 32.8x. At first glance, this discount might suggest the stock is undervalued compared to other software companies. However, Simply Wall St’s proprietary “Fair Ratio” refines this view by calculating what Dropbox’s PE should be, given its unique mix of growth prospects, risk factors, profit margins, industry, and size. For Dropbox, this Fair Ratio is set at 25x.

By weighing all these important factors, the Fair Ratio metric gives a much more precise reading on valuation than just stacking the company against industry benchmarks or competitors. In Dropbox’s case, with a market PE of 16.1x and a Fair Ratio of 25x, the stock appears undervalued, trading at a notable discount to what would be justified given its fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1414 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Dropbox Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple yet powerful approach that lets investors tell the story behind a company using their own assumptions about Dropbox’s future growth, profitability, and risks to estimate fair value and chart expected outcomes. Rather than sticking to just a single set of numbers, a Narrative links your perspective of Dropbox’s business drivers to a forecast and then directly to a calculated fair value, offering a bridge from "what you believe" to "what Dropbox might be worth."

Narratives are an easy-to-use feature, available to everyone on Simply Wall St within the Community page, and relied upon by millions of investors. They help you decide the right time to buy or sell by letting you compare the Fair Value resulting from your Narrative with Dropbox’s current share price, and the experience is fully dynamic because your valuation updates whenever new information or earnings become available.

For example, one Dropbox Narrative reflects a bullish view that growing AI-powered features and product innovation will push fair value as high as $35.00 per share, while a more cautious Narrative sees pricing pressure and competition limiting fair value to just $20.00. This empowers you to choose which story makes the most sense to you.

Do you think there's more to the story for Dropbox? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com