Where Does Hilton Stand After Five-Year 180% Rally and Recent Strategic Partnerships?

- Wondering if Hilton Worldwide Holdings is a bargain or overpriced after all its recent moves? You are not alone. Let us dig in and find out what is really driving its value.

- The stock is up 8.9% over the past year and a remarkable 180.1% over five years. However, it slipped by 4.0% this past week, highlighting both strong long-term momentum and some recent volatility.

- Market watchers have pointed to Hilton’s global expansion and a flurry of strategic partnerships as key drivers of both the rally and its recent pullback. In particular, renewed travel demand and ongoing investments in new properties have caught the attention of investors seeking growth stories in the hospitality space.

- Despite all this activity, Hilton scores just 0 out of 6 on our valuation checks. This suggests there is more to the story than meets the eye. We are about to break down the main valuation approaches, and at the end, we will reveal a smarter way to judge whether Hilton is really worth its current price tag.

Hilton Worldwide Holdings scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Hilton Worldwide Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and then discounting those amounts back to today’s dollars. This approach provides an intrinsic value based on how much cash Hilton Worldwide Holdings is expected to generate over the long run.

For Hilton, the latest available Free Cash Flow is $2.29 billion. Analyst forecasts project annual Free Cash Flow remaining above $2 billion through at least 2027. Beyond that, Simply Wall St’s model extrapolates continued healthy cash generation, with ten-year forward estimates still hovering around $2 billion per year. All values are reported in US dollars.

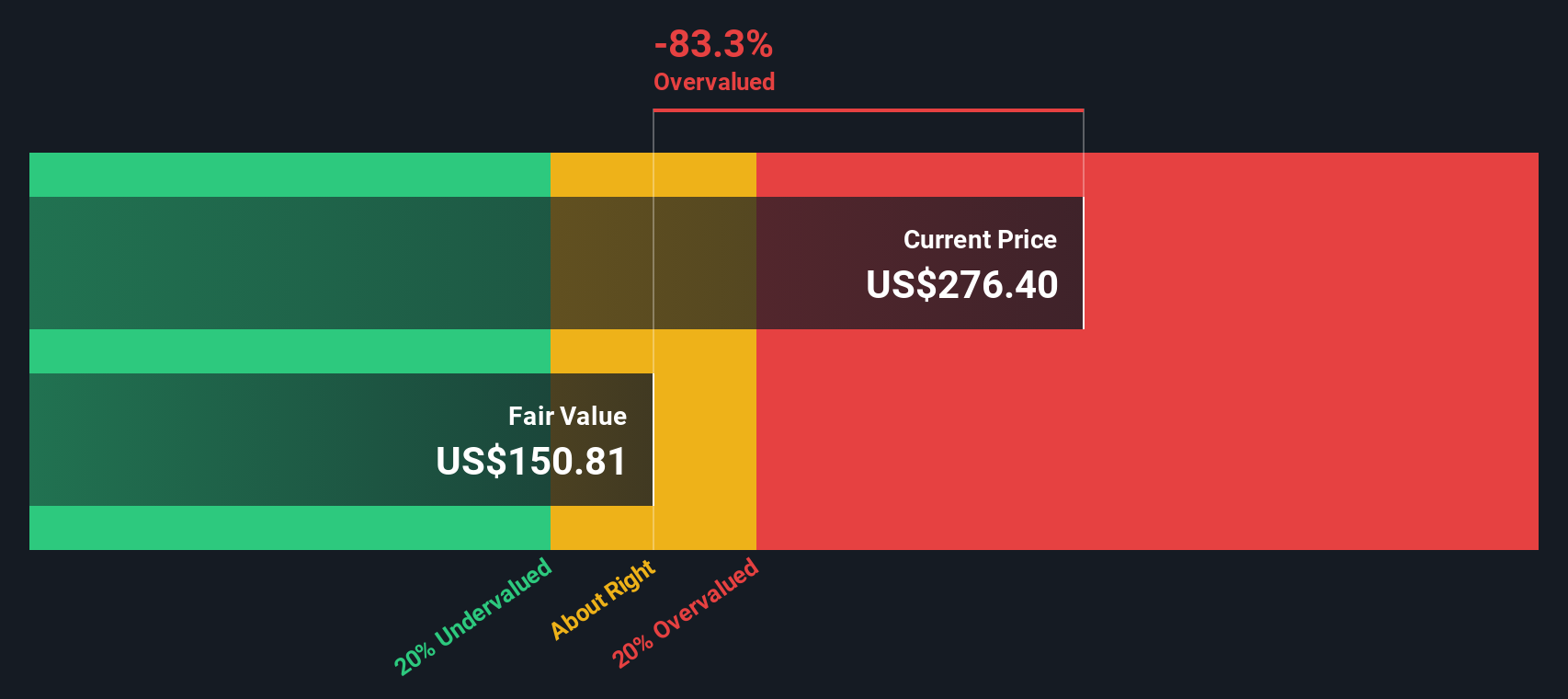

When these future cash flows are discounted using a standard two-stage Free Cash Flow to Equity model, we arrive at an intrinsic value of $123.50 per share. However, compared to Hilton’s current market price, this points to the stock trading about 108.1% above its fair value based on DCF analysis, which suggests it may be significantly overvalued by this measure.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hilton Worldwide Holdings may be overvalued by 108.1%. Discover 839 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Hilton Worldwide Holdings Price vs Earnings

For companies that generate substantial, consistent profits like Hilton Worldwide Holdings, the Price-to-Earnings (PE) ratio is a widely respected method to assess value. The PE ratio connects a company's share price to its net income and helps investors understand how much they are paying for each dollar of current earnings.

Generally, a higher PE ratio is justified for companies with strong growth potential or lower risk profiles, while lower PE ratios are reserved for companies facing more uncertainty or slower growth. It is important to weigh a company's PE not only against competitors, but also alongside risk and growth prospects.

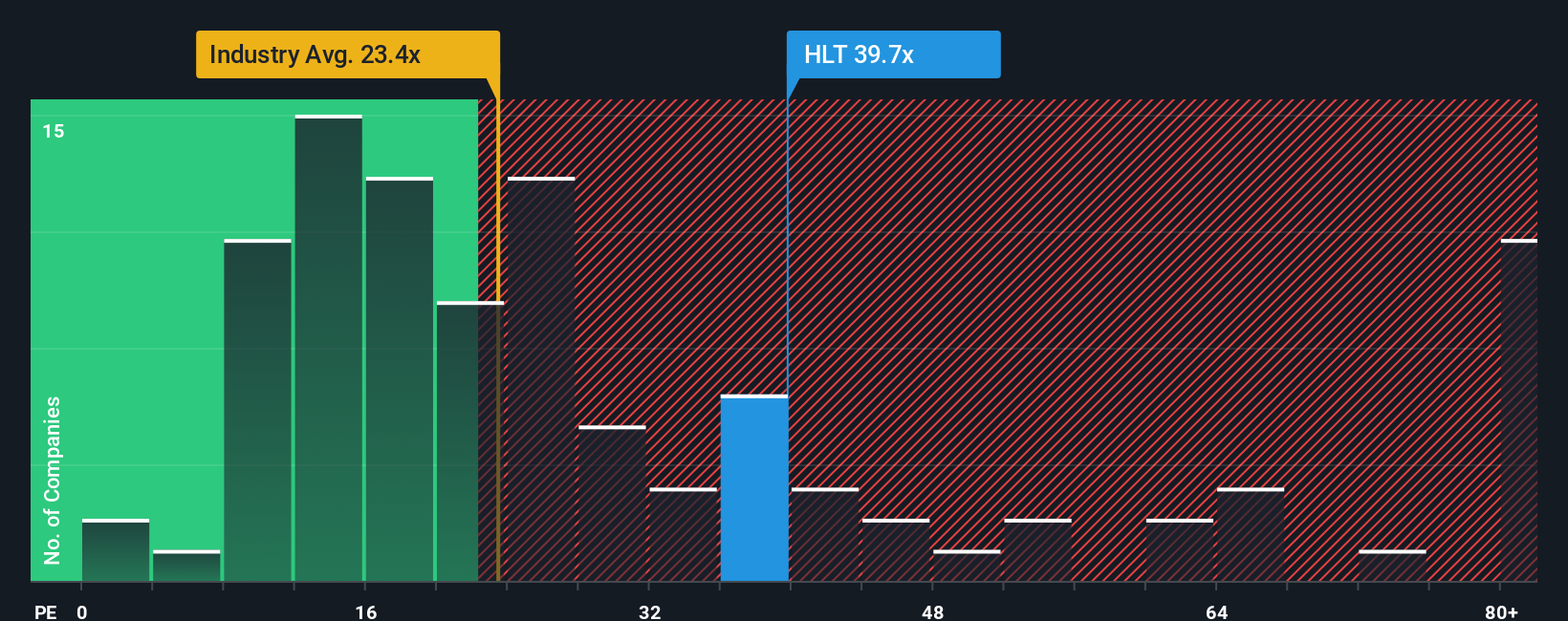

Hilton’s current PE ratio stands at 35.9x. This is considerably higher than both the Hospitality industry average of 23.3x and the average for similar peers at 22.9x. At first glance, this suggests Hilton’s shares are trading at a premium to its sector and closest rivals.

However, Simply Wall St’s proprietary Fair Ratio, which is 28.9x for Hilton, is even more useful because it incorporates a range of specific factors including Hilton’s earnings growth, profit margins, size, risks, and industry characteristics. The Fair Ratio takes these dynamics into account and offers a more tailored and reliable assessment than looking just at broad industry averages.

Comparing Hilton’s current PE of 35.9x to the Fair Ratio of 28.9x, the stock appears to be trading well above what would be expected when considering all its relevant factors.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1411 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hilton Worldwide Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Think of a Narrative as your investment story, a clear, personalized perspective that connects what you believe about a company’s future with specific financial forecasts and a fair value that reflects those beliefs.

Narratives make investing more approachable by turning your unique view into numbers. You can easily create or explore Narratives on Simply Wall St’s Community page, used by millions of investors. Each Narrative ties together your expectations for Hilton Worldwide Holdings' revenue, earnings growth, and profit margins, and then instantly calculates a fair value for the stock.

This approach empowers you to decide whether Hilton is a buy or sell by seeing how your Narrative’s fair value compares to the current market price. Since Narratives update automatically when new news or earnings are released, you always have relevant, actionable insight at your fingertips.

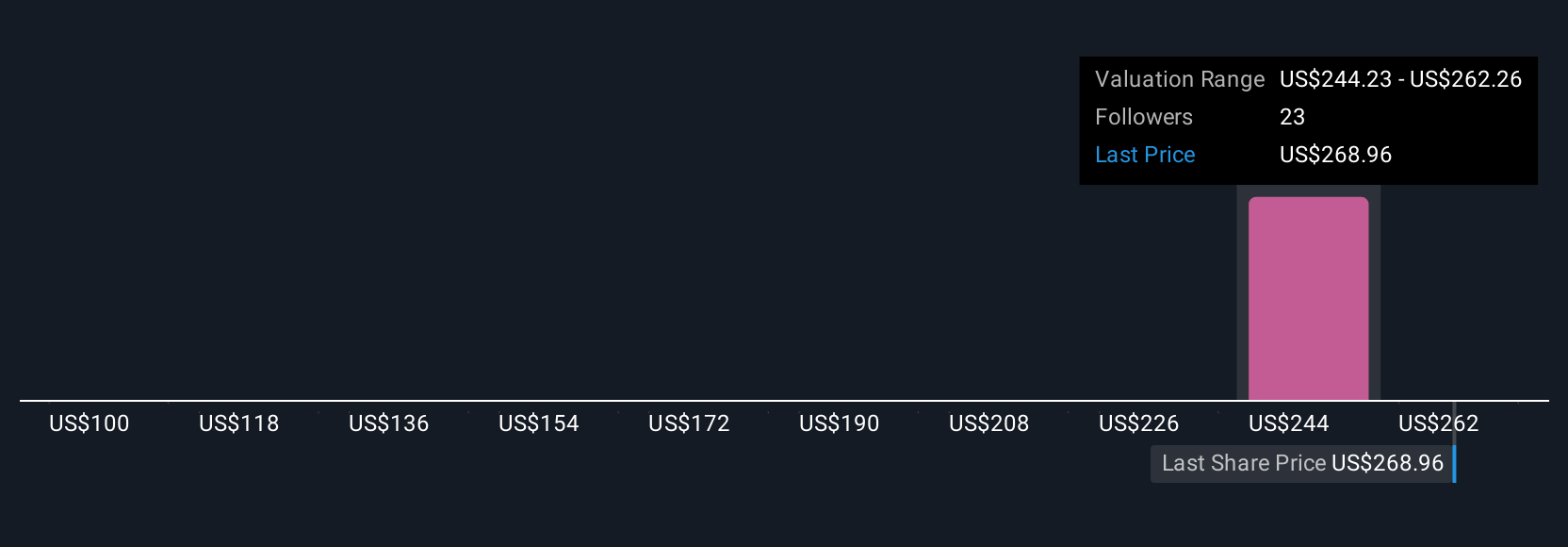

For example, some Hilton Worldwide Holdings investors see aggressive global expansion and premium brand focus driving earnings much higher, and their Narrative sets an optimistic fair value near $311 per share. Others worry about economic and competitive headwinds, leading them to a more cautious Narrative with a fair value closer to $229. Narratives help you make decisions with confidence, based on your own view of the future.

Do you think there's more to the story for Hilton Worldwide Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com