Assessing Alimak Group (OM:ALIG) Valuation After Mixed Earnings and Recent Trading Volatility

Alimak Group (OM:ALIG) just released its Q3 earnings, highlighting a dip in quarterly sales and profits compared to last year. However, net income for the first nine months showed a solid improvement.

See our latest analysis for Alimak Group.

Alimak Group’s latest earnings update follows a stretch where momentum has clearly faded, with the share price down 12.3% over the past month and off 15.8% in the last quarter. Still, if you zoom out, the company’s total shareholder return is up an impressive 17.2% over the last year, and a stellar 189% over three years. This suggests that investors with a longer-term view have been strongly rewarded despite recent volatility.

If you’re curious what other stocks are driving strong longer-term gains, this might be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership.

With Alimak Group trading at a notable discount to analyst targets and recent growth figures sending mixed signals, the key question becomes whether the current dip is an undervalued entry point or if future gains are already reflected in the current price.

Most Popular Narrative: 17% Undervalued

According to the most widely followed narrative, Alimak Group’s estimated fair value stands well above its recent close, indicating a double-digit upside in the eyes of consensus. The estimated fair value blends detailed earnings, margin, and discount rate projections to reflect potential long-term gains, not just short-term price movements.

Expansion of automation and digitalization is opening new recurring revenue streams, with Alimak investing in product development, digital offerings, and remote monitoring solutions. This is evident in both recent innovation awards and ongoing R&D focus, and these initiatives support improved margins and drive higher earnings through more differentiated and value-added solutions.

Curious what’s fueling the analyst outlook? The formula behind this valuation includes ambitious profit growth, bullish margin expansion, and a future earnings multiple typically reserved for market favorites. Want to uncover the full story and the crucial forecast that could shape Alimak’s next move? Dive in to see which financial assumptions are driving the potential upside.

Result: Fair Value of $169.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weakness in global construction or failure to execute recent acquisitions could undermine Alimak Group’s margin progress and dilute future earnings growth.

Find out about the key risks to this Alimak Group narrative.

Another View: The Multiples Perspective

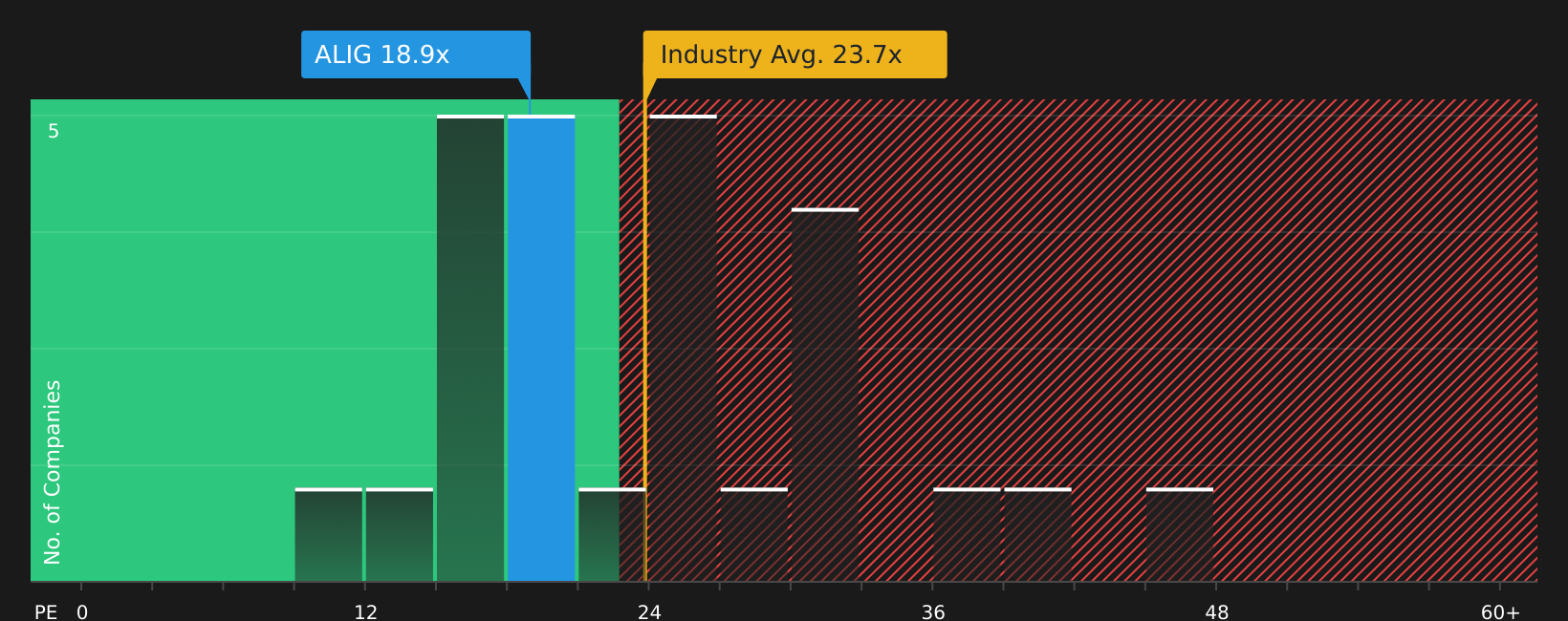

While consensus points to upside based on projected earnings growth, the current price-to-earnings ratio of 21.4 times is actually higher than the fair ratio estimate of 20.8 times. It still sits well below both industry (24.5x) and peer averages (28.4x), highlighting both value potential and valuation risk. Will the market move to close this gap, or is this a sign that caution is warranted?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Alimak Group Narrative

If you see things differently or want to dig into the numbers yourself, it’s easy to create your own take in just a few minutes. Do it your way.

A great starting point for your Alimak Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Missing out on the right stock now could mean leaving impressive gains on the table. Give yourself an edge with these fresh opportunities tailored to your strategy:

- Uncover high yields by tapping into these 22 dividend stocks with yields > 3% that consistently deliver over 3% returns for income-focused investors.

- Accelerate your portfolio’s growth potential by targeting these 26 AI penny stocks with proven leadership in artificial intelligence markets.

- Advance your holdings with these 28 quantum computing stocks as they move the needle in tomorrow’s quantum computing breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com