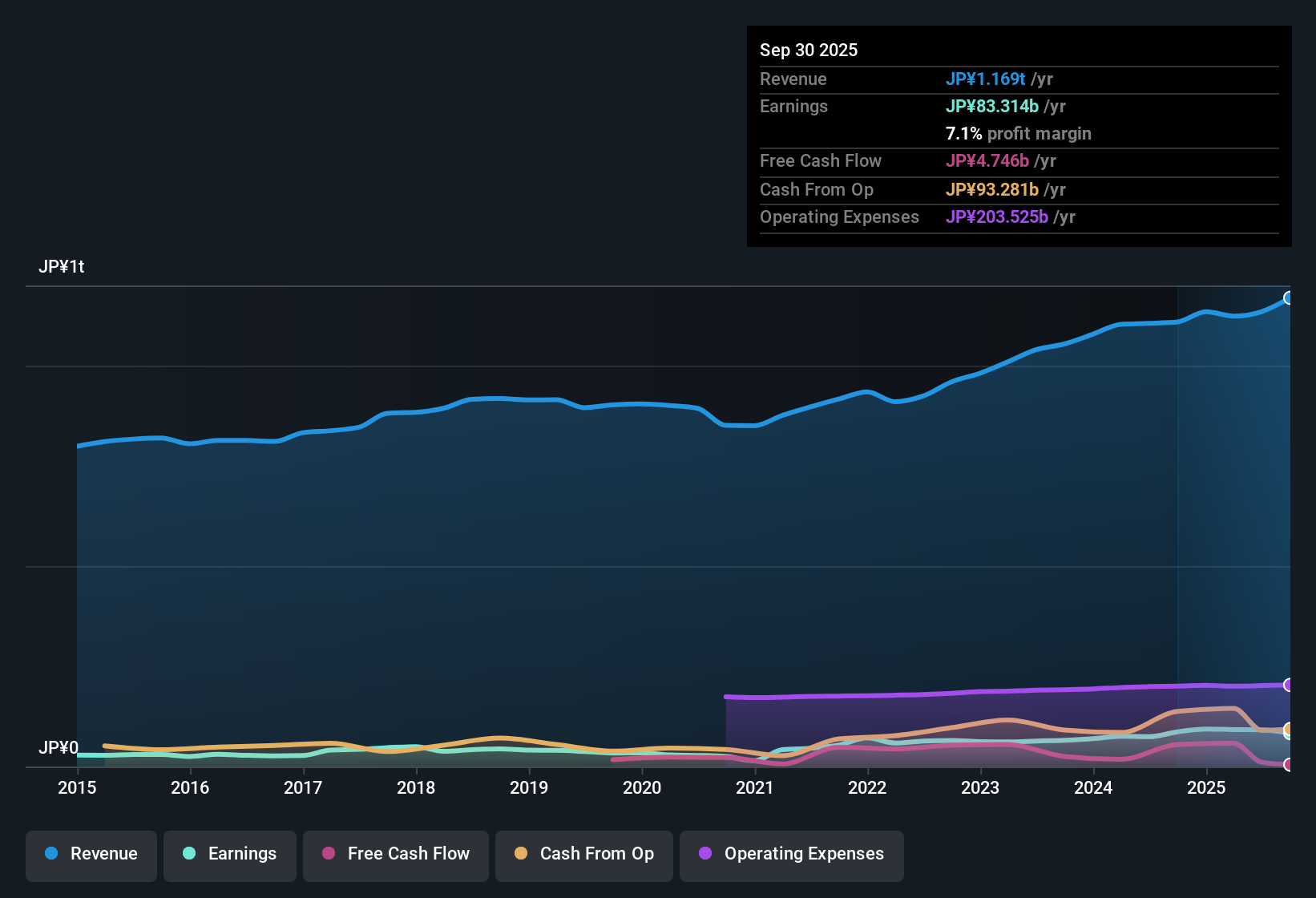

Fuji Electric (TSE:6504) Margin Decline Challenges Bullish Narratives Despite Higher Earnings Growth Forecast

Fuji Electric (TSE:6504) reported revenue that is forecast to grow at 3.6% per year, trailing the broader Japanese market’s expected 4.5% annual growth. Earnings are projected to rise at 8.6% per year, which is a step ahead of the market average of 7.9%. However, the past year delivered negative earnings growth compared to the impressive 18.6% per year over the previous five years. Meanwhile, profit margins narrowed to 7.1% from 7.8% last year, signaling some pressure despite the company’s reputation for high-quality earnings.

See our full analysis for Fuji Electric.The next section will look at how these latest numbers compare with market expectations and the most prominent narratives surrounding Fuji Electric. It is a chance to see which stories hold up, and where the results call for a rethink.

See what the community is saying about Fuji Electric

Profit Margins Projected to Recover

- Analysts forecast that Fuji Electric’s profit margins will rise from 8.1% to 8.3% by 2028, following a dip to 7.1% this year. This indicates a gradual, but not dramatic, improvement ahead.

- Analysts' consensus view highlights that while near-term margin compression is connected to capacity expansion and increased costs, there is confidence that long-term electrification and renewable energy trends, along with new, higher-value project wins, can support rising operating margins and strong cash flow generation.

- Upward revisions to consolidated earnings guidance support the idea that management is extracting value from these structural industry shifts.

- The consistent push into energy management, semiconductors, and automation is seen as a buffer for margins, even in the face of rising fixed and raw material costs.

- See what management’s outlook means for long-term investors in the full Consensus Narrative. 📊 Read the full Fuji Electric Consensus Narrative.

Domestic Market Reliance Poses a Growth Risk

- Overseas sales made up just 29% of total revenue and declined year-on-year, underscoring Fuji Electric’s continued dependence on its home market and its exposure to shifts in the Japanese economy.

- Analysts' consensus view flags that heavy domestic concentration, combined with weaker overseas demand, creates vulnerability.

- If domestic economic conditions stall, long-term revenue growth may be capped despite global electrification and automation tailwinds.

- Negative trends in the automotive semiconductor business and factory automation, including rising costs from new capacity, echo these risks to sustaining profits.

Valuation Sits Between Bargain and Premium

- Fuji Electric’s price-to-earnings ratio of 19.6x is higher than the Japanese electrical industry average of 13.3x, but below peer companies at 32.3x. Meanwhile, the ¥11060.0 share price currently sits above the DCF fair value estimate of ¥7299.43, and also exceeds the average analyst price target of ¥10590.0.

- According to analysts' consensus, the narrow 4.4% gap between the current share price and the consensus price target suggests that shares are not dramatically overvalued or undervalued.

- Long-term growth hopes are balanced by only moderate expected improvements in margins and continued cost risks.

- This tension leads to mixed sentiment. Investors must judge if structural industry advantages outweigh present valuation headwinds, given the lack of a deep discount to fair value.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Fuji Electric on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a fresh take on these results? Share your perspective and shape your own story in just a few minutes. Do it your way

A great starting point for your Fuji Electric research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Fuji Electric faces ongoing valuation pressure because of only modest profit growth and its limited exposure outside the domestic market.

If you want to focus on companies trading at more attractive prices with upside potential, take a look at our these 832 undervalued stocks based on cash flows for better value opportunities right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com