Assessing CNA Financial (CNA): Is the Current Valuation Overlooking Long-Term Growth Potential?

See our latest analysis for CNA Financial.

While CNA Financial’s share price has seen a modest dip this year, with a year-to-date return of -7.2%, its long-term total shareholder returns paint a much brighter picture, with gains of over 32% in three years and nearly doubling over five. This blend of short-term turbulence and solid long-term performance suggests investors are still weighing the company’s risk profile, but the growth story hasn’t faded.

If you're looking for more opportunities like CNA, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

With CNA Financial’s shares trading close to analyst targets, but well below calculated intrinsic value, the question remains: is the company currently undervalued and ripe for upside, or is all future growth already reflected in its price?

Price-to-Earnings of 13.7x: Is it justified?

CNA Financial is trading at a price-to-earnings (P/E) ratio of 13.7x. This puts its shares above the industry average and signals a relatively rich valuation at its recent closing price of $44.55.

The P/E ratio is a common benchmark for comparing a company’s market value to its earnings. In the insurance sector, where profits can fluctuate based on underwriting cycles and investment income, a higher P/E can reflect market confidence in sustained earnings or expectations of future growth.

But is this valuation warranted? CNA’s P/E is not only higher than the US Insurance industry average of 13.2x, but it also matches the average for its peer group (13.7x). This suggests investors are expecting performance at least on par with, if not slightly above, its rivals. However, against the estimated fair P/E ratio of 20.3x for CNA, today’s price could be seen as conservative relative to its growth outlook. This may hint at possible upside if the market recalibrates its expectations.

Explore the SWS fair ratio for CNA Financial

Result: Price-to-Earnings of 13.7x (ABOUT RIGHT)

However, unpredictability in annual net income and ongoing sector shifts could pose risks that temper expectations for CNA Financial’s near-term performance.

Find out about the key risks to this CNA Financial narrative.

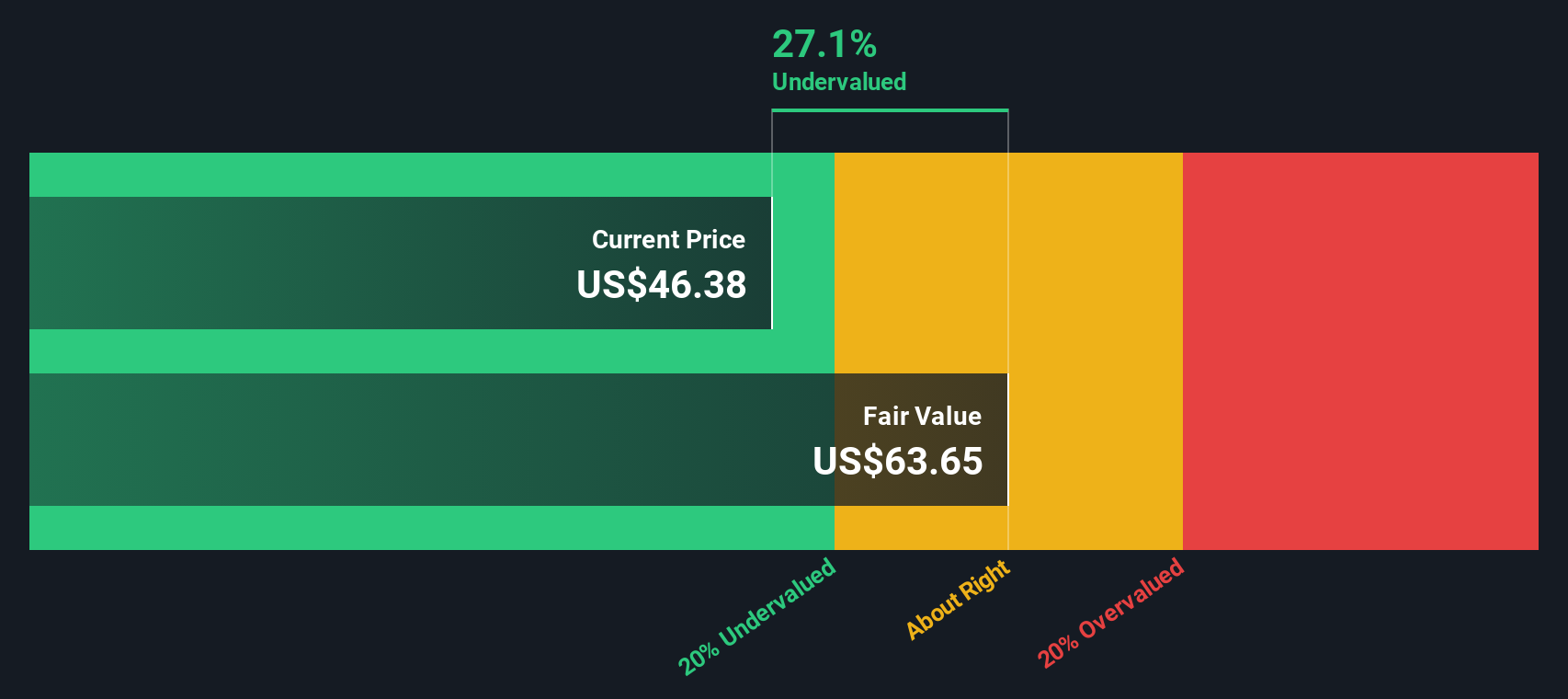

Another View: What Does a Discounted Cash Flow Say?

While the share price seems lofty relative to sector averages, our DCF model tells a different story by estimating CNA’s fair value at $65.97 per share, which is well above its current trading price. This suggests the market may be underpricing CNA’s future cash flows. Could the street be missing something bigger?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CNA Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 832 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own CNA Financial Narrative

If you see things differently or want to dive deeper yourself, you can put together your own analysis and personal narrative in just a few minutes, and Do it your way.

A great starting point for your CNA Financial research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Take charge of your investing journey by searching smarter and spotting your next potential winner. These hand-picked opportunities are waiting for you today.

- Accelerate your search for high returns with these 832 undervalued stocks based on cash flows, offering standout value in today’s market.

- Secure reliable passive income streams by tapping into these 22 dividend stocks with yields > 3%, packed with top dividend payers yielding over 3%.

- Seize big potential by jumping into these 26 AI penny stocks, featuring innovative companies shaping the future of artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com