Marsh McLennan (MMC): Rethinking Valuation as Shares Lose Momentum

Marsh & McLennan Companies (MMC) stock has come under some pressure in the past month, with shares sliding about 11%. Investors might be reassessing its valuation as the broader insurance sector faces shifting market conditions.

See our latest analysis for Marsh & McLennan Companies.

Shares of Marsh & McLennan Companies have lost ground recently, adding to a broader pullback that sees the stock down 11.5% over the past month and nearly 16% year-to-date. The momentum has definitely faded, shifting the tone after several strong years, but the longer-term picture still includes a 75% total shareholder return over five years. This shows that patient investors have generally fared well despite near-term jitters.

If you’re looking to spot what else is trending beyond insurance, this is an ideal moment to broaden your search and discover fast growing stocks with high insider ownership

With Marsh & McLennan stock now trading well below recent highs and analysts suggesting a notable discount to fair value, investors may be wondering whether this weakness is an invitation for long-term investors or if future growth is already fully reflected in the price.

Most Popular Narrative: 18.4% Undervalued

Based on the narrative’s assessment, Marsh & McLennan Companies’ fair value estimate substantially exceeds the recent closing price, fueling debate around whether the market is underestimating future prospects or pricing in hidden risks. The narrative’s foundation leans on a set of bullish business drivers, but also recognizes there are active uncertainties at play.

Strategic investments in digital transformation, advanced analytics, and AI (for example, proprietary data tools for risk modeling and agentic interfaces) are expected to enhance operational efficiency and improve product and service offerings, enabling margin expansion and net earnings growth through improved client retention and lower cost to serve.

Want to discover what’s powering this high conviction? The key to this optimistic valuation lies in a handful of aggressive growth forecasts analysts are betting on. How much could revenue and profit margins really expand? The answer might surprise you. Dive deeper to find out which key assumptions tip the balance in this fair value calculation.

Result: Fair Value of $218.21 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent declines in insurance pricing and volatile consulting demand could create challenges for Marsh & McLennan’s long-term revenue and earnings growth outlook.

Find out about the key risks to this Marsh & McLennan Companies narrative.

Another View: Valuation by Multiples

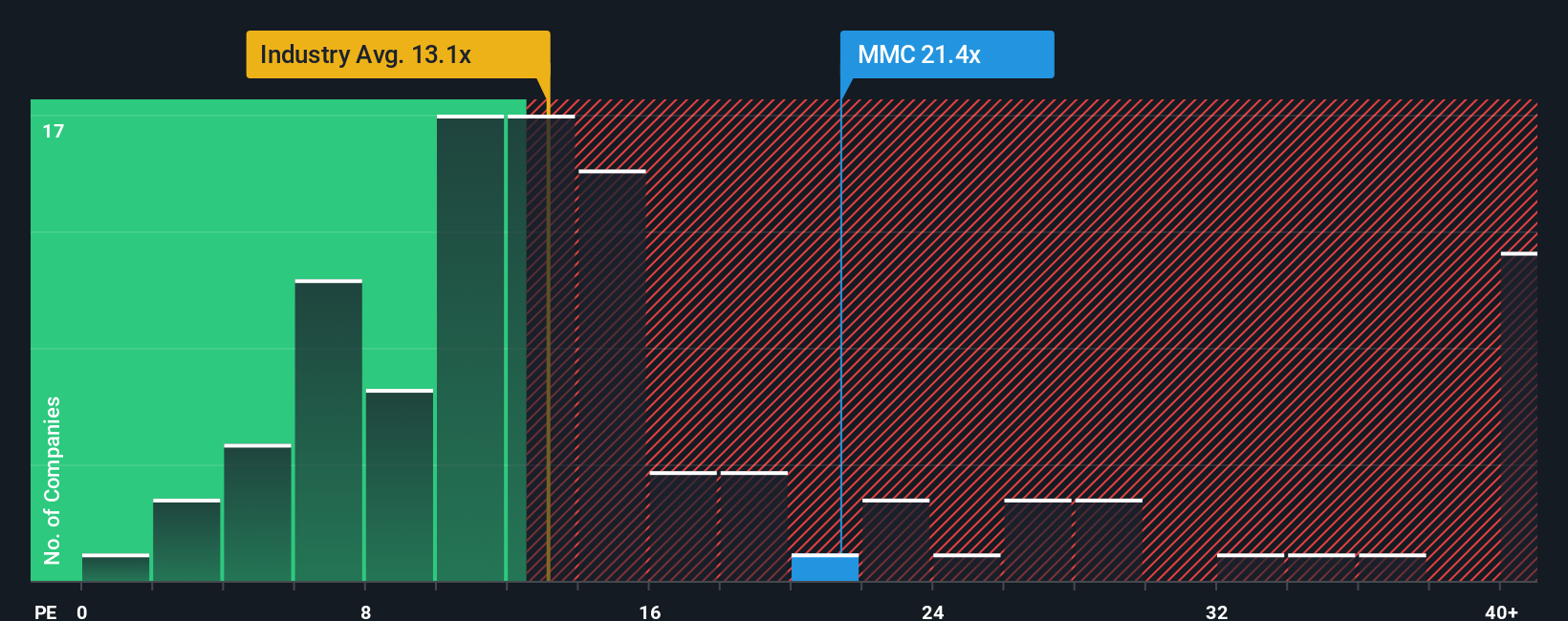

Taking a different angle, the current price-to-earnings ratio stands at 21.1 times, which is higher than both the US Insurance industry average of 13.2 times and the fair ratio of 16.3 times. This suggests Marsh & McLennan is valued at a premium compared to its peers. Could this indicate added risk for investors, or does it represent confidence in future prospects?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Marsh & McLennan Companies Narrative

Prefer your own approach or see the data differently? You can analyze the numbers and piece together your own take in just a few minutes. Do it your way

A great starting point for your Marsh & McLennan Companies research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Give yourself an edge by checking out stocks that fit your strategy. These handpicked ideas could put you ahead of the crowd before the next big shift.

- Tap into the excitement of up-and-coming digital assets by reviewing these 81 cryptocurrency and blockchain stocks that are driving innovation in blockchain and decentralized finance.

- Catch the wave of strong cash flows and low valuations with these 832 undervalued stocks based on cash flows poised for a potential rebound based on solid fundamentals.

- Supercharge your long-term income by browsing these 22 dividend stocks with yields > 3% offering yields above 3% and proven track records of rewarding shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com