A Look at Comfort Systems USA’s (FIX) Valuation Following Record Growth in Sales, Margins, and AI-Driven Demand

Comfort Systems USA (FIX) caught investor attention after unveiling third quarter results, where sales and profits jumped meaningfully. The company credits strong demand in technology construction and data center projects for this upward momentum.

See our latest analysis for Comfort Systems USA.

Comfort Systems USA’s share price has surged over the past year, notching a 124.8% year-to-date gain and helping deliver a total shareholder return of 147% in just twelve months. This momentum has only intensified recently, with robust third quarter earnings, a fresh dividend hike, and ongoing buybacks all supporting recent stock strength. Investors who have held on longer term have been rewarded handsomely as well, as the company’s three-year total shareholder return now stands at an eye-catching 732%.

If these kinds of outsized gains have sparked your curiosity, it’s the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With the stock up sharply in 2025 and growth bets fueling bullish analyst targets, investors must now ask whether Comfort Systems USA shares remain undervalued, or if the market is already pricing in years of future expansion.

Most Popular Narrative: 4.4% Undervalued

With Comfort Systems USA stock closing at $963.30 and the narrative consensus fair value at $1,007.80, the stage is set for a valuation debate driven by surging demand, record profits, and robust future expectations.

Strategic execution and disciplined project selection, prioritizing high-growth, higher-margin markets and leveraging skilled talent positioning, enable superior pricing power and operational efficiency. This drives continued gross margin and operating income expansion relative to industry peers.

Want to know what’s fueling this premium valuation? The secret mix behind record-breaking revenue, profit expansion, and future earnings multiples might surprise you. See how bold expectations on growth, profit margins, and share count shape the math. Find out what turns analyst optimism into a compelling fair value.

Result: Fair Value of $1,007.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, looming risks such as a cooling technology sector or persistent labor shortages could threaten both revenue growth and margin expansion in the future.

Find out about the key risks to this Comfort Systems USA narrative.

Another View: Multiples Hint at Lofty Valuations

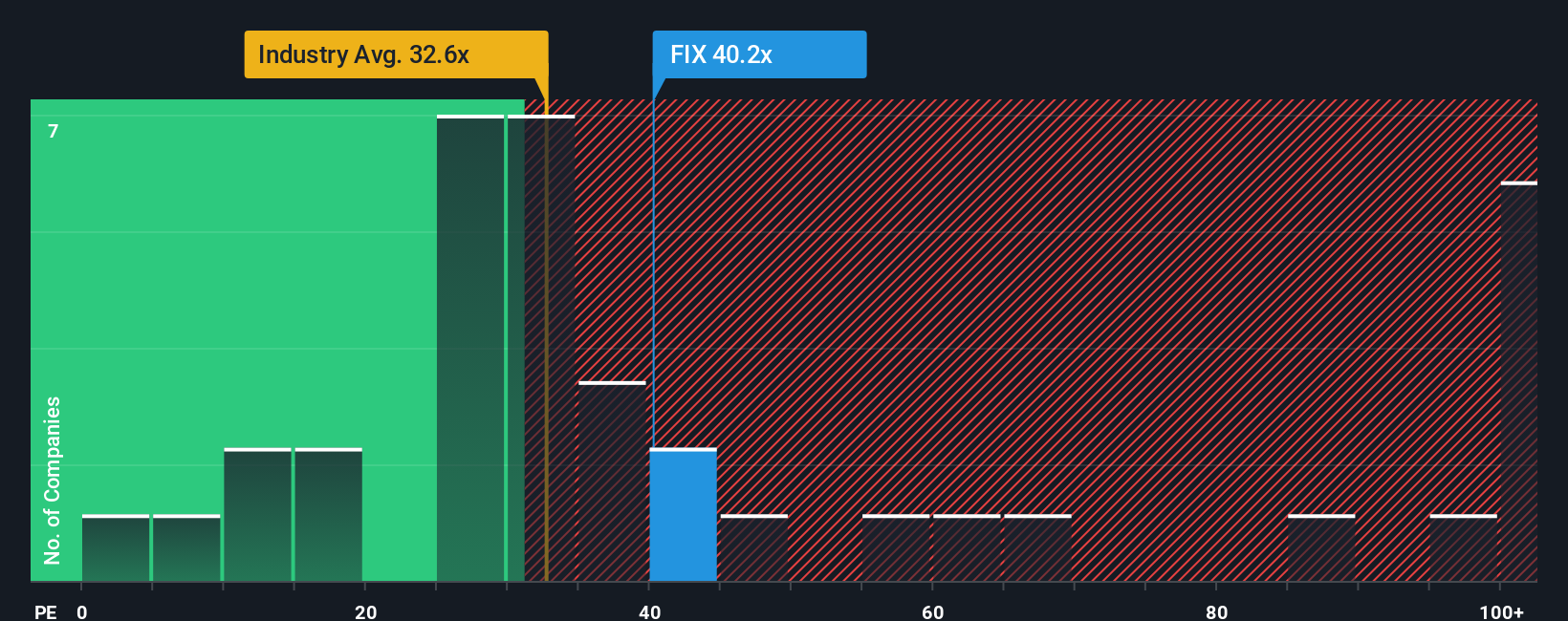

Looking at Comfort Systems USA from a price-to-earnings perspective, the shares trade at 40.5 times earnings, which is well above the US Construction industry average of 34.8 and the peer average of 46.1. While this signals premium expectations, it is actually below the stock's fair ratio of 47.8. This suggests there could still be some runway. Does this market optimism signal fresh upside or increased risk if the growth story falters?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Comfort Systems USA Narrative

Not convinced by these perspectives, or looking to dive deeper into the numbers yourself? You can quickly craft your own story and see how your conclusions stack up. Do it your way.

A great starting point for your Comfort Systems USA research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors stay flexible and always have an edge. Don’t just watch one stock soar while others pass you by. Expand your horizons with these powerful opportunities right now:

- Unlock higher yields as you scan for consistent income winners with these 24 dividend stocks with yields > 3% delivering returns above 3%.

- Capitalize on the unstoppable momentum in healthcare breakthroughs by using these 34 healthcare AI stocks to spot the next leaders in AI-driven medical innovation.

- Catch emerging market trends early by checking out these 81 cryptocurrency and blockchain stocks, where tech-savvy disruptors are changing the landscape of finance and blockchain.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com