Cytokinetics (CYTK) Faces Lawsuits After FDA Delays Heart Drug Review for REMS Omission – Has the Investment Thesis Shifted?

- In October 2025, Cytokinetics disclosed that the FDA extended its review period for the cardiac drug aficamten due to the omission of a required Risk Evaluation and Mitigation Strategy (REMS), prompting several class action lawsuits alleging the company misled investors about regulatory risks and timelines.

- This development highlighted potential gaps between the company's public communications and regulatory expectations, leading to heightened investor scrutiny regarding clinical and legal risk disclosures.

- Next, we'll assess how increased regulatory uncertainty and legal challenges tied to aficamten could shift Cytokinetics' investment narrative.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

Cytokinetics Investment Narrative Recap

Cytokinetics’ investment story centers on the successful regulatory approval and commercial launch of aficamten, a late-stage cardiac therapy. The recent news of an FDA review extension and related class action lawsuits introduces real uncertainty around the most immediate catalyst, FDA clearance of aficamten, and highlights regulatory compliance as the company’s biggest near-term risk. How management addresses regulatory feedback and legal scrutiny going forward remains in sharp focus, as any further delays or negative outcomes could materially impact revenue timelines.

Most relevant to this topic is the September 2025 announcement, when Cytokinetics confirmed it discussed the proposed aficamten REMS with the FDA during its Late Cycle Meeting. This update provided detail on post-marketing requirements but did not flag the now consequential REMS omission, underlining why transparent communications about regulatory hurdles and pending drug applications are critical in shaping investor expectations during pivotal approval cycles.

In contrast to catalysts around aficamten’s market potential, investors should also be aware that...

Read the full narrative on Cytokinetics (it's free!)

Cytokinetics' narrative projects $649.5 million revenue and $90.6 million earnings by 2028. This requires 96.4% yearly revenue growth and a $696.9 million earnings increase from current earnings of -$606.3 million.

Uncover how Cytokinetics' forecasts yield a $75.83 fair value, a 22% upside to its current price.

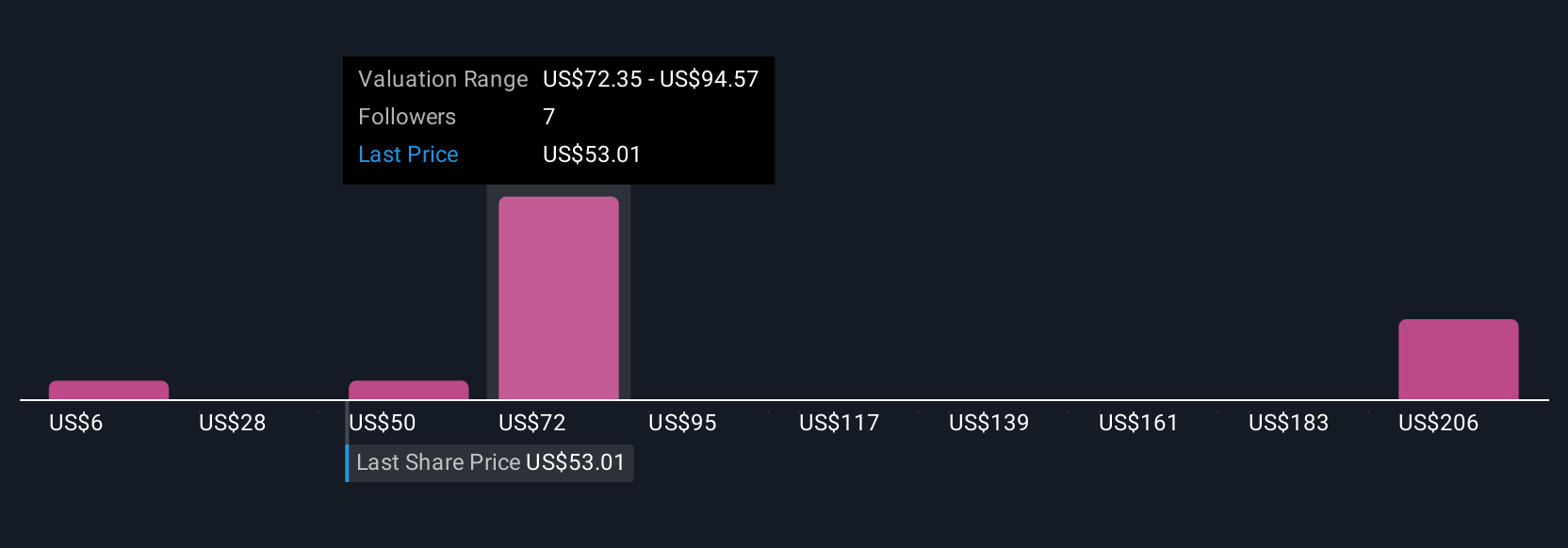

Exploring Other Perspectives

Five Community members estimated Cytokinetics’ fair value from as low as US$5.69 to as high as US$208.66 per share. As regulatory risk looms larger following the REMS-related delay, broad opinion differences show just how much your outlook on approvals and legal overhangs could shape expectations for the company’s performance.

Explore 5 other fair value estimates on Cytokinetics - why the stock might be worth over 3x more than the current price!

Build Your Own Cytokinetics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cytokinetics research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Cytokinetics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cytokinetics' overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com