Should You Consider Estée Lauder After Its 32% Stock Surge and Global Expansion News?

- Wondering if Estée Lauder Companies is a hidden gem or just pricy perfume for your portfolio? You’re not alone in questioning whether now is the right moment to buy in.

- The stock has swung up 10.8% in the last month and is up an impressive 31.9% year-to-date, but it’s still climbing back after a rough couple of years, with a 44.2% gain over the past 12 months.

- Recent headlines highlight increasing interest around Estée Lauder's global brand moves, including expansions in Asia and renewed strategic marketing pushes. Investor optimism appears to be growing as the company seeks to recapture market share and adapt to evolving consumer preferences.

- Right now, Estée Lauder scores just 1/6 on our valuation checks, so let's break down how analysts and different models look at its value. There may be an even more insightful approach by the end of this article.

Estée Lauder Companies scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Estée Lauder Companies Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a popular valuation approach that projects a company’s future cash flows, then discounts them back to today’s values. This method provides a data-driven estimate of what the business is considered to be worth at present.

For Estée Lauder Companies, the latest reported Free Cash Flow stands at $483.3 million. Analysts estimate that cash flows will increase over the coming years, reaching about $2.03 billion by 2029. It is important to note that cash flow estimates rely on analyst projections for the next five years, with further estimates extrapolated by Simply Wall St to cover the decade ahead.

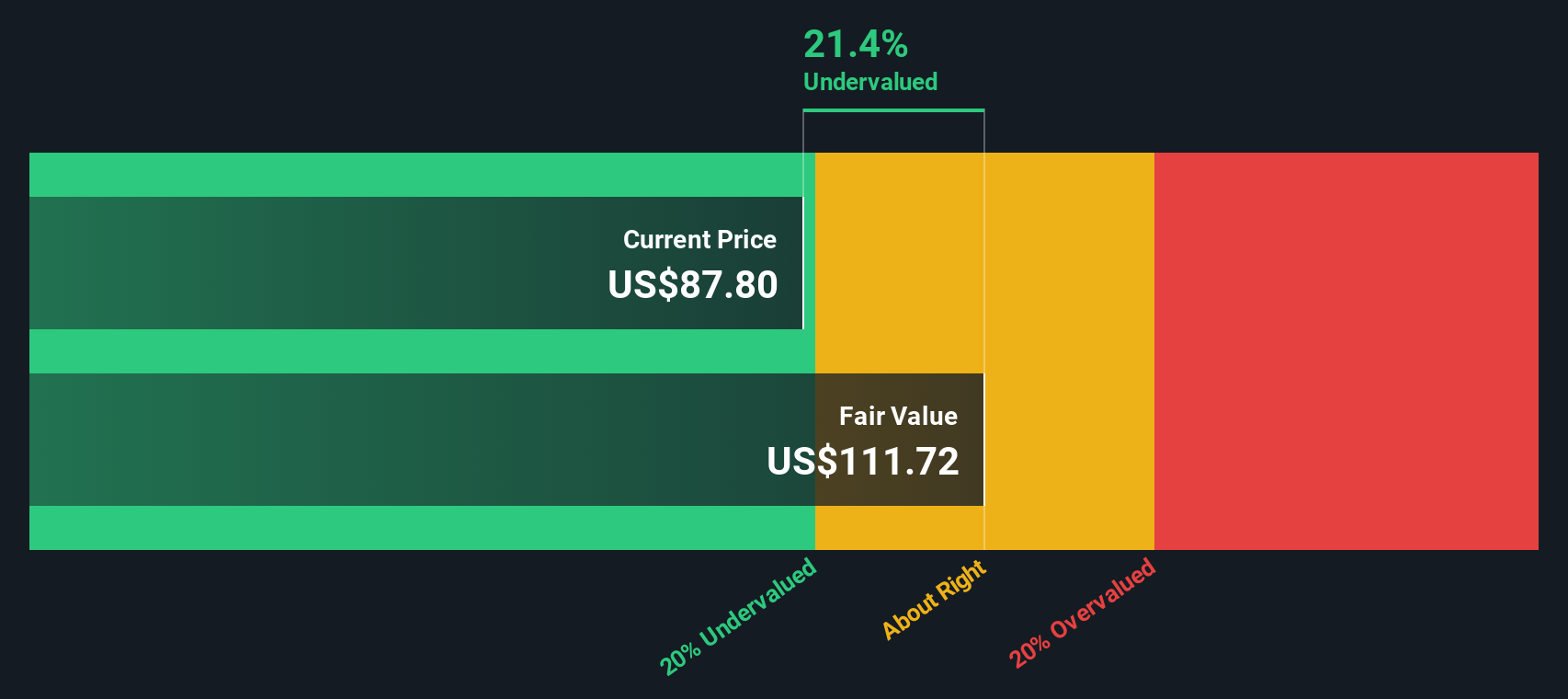

Based on these projections, the DCF model calculates an intrinsic value per share of $116.13. Compared to its current share price, the stock appears to be trading at a 15.9% discount, suggesting it is undervalued according to these cash flow assumptions.

In summary, if you trust these long-range estimates, Estée Lauder appears to offer value for investors seeking a price below what the underlying discounted cash flows indicate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Estée Lauder Companies is undervalued by 15.9%. Track this in your watchlist or portfolio, or discover 831 more undervalued stocks based on cash flows.

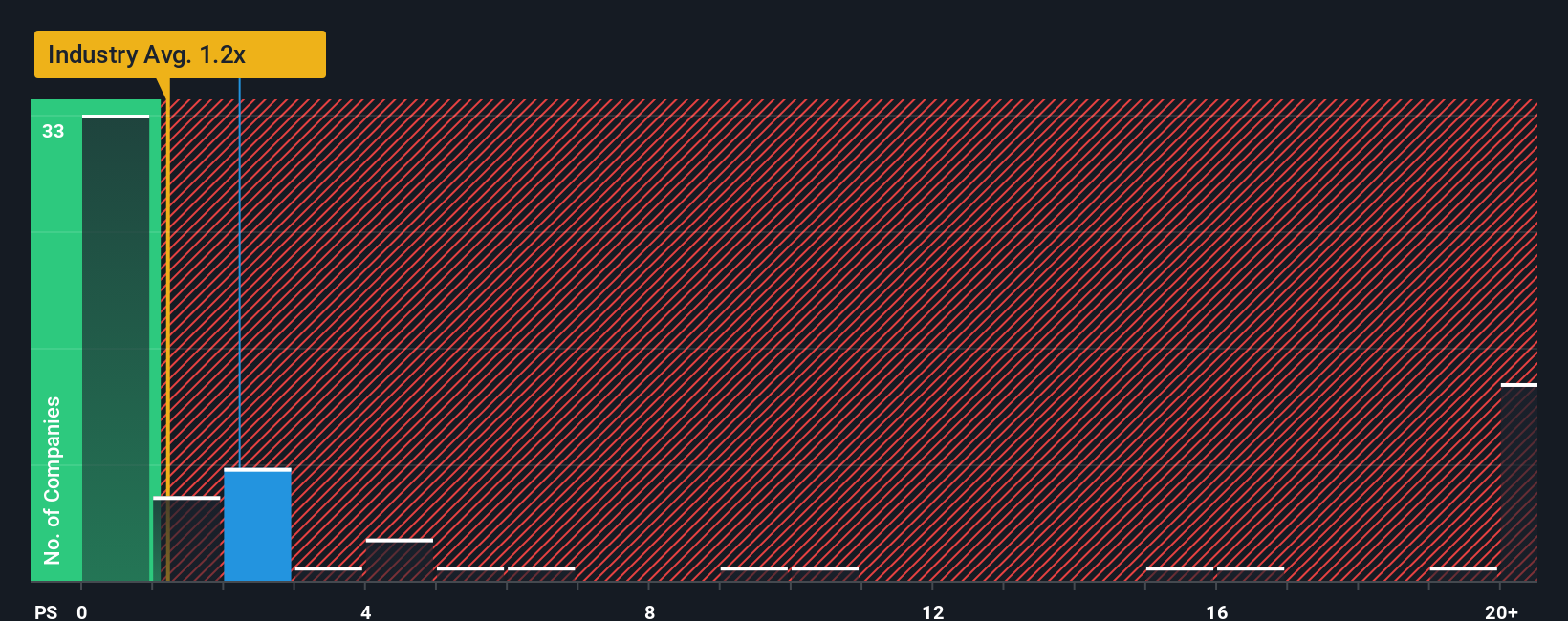

Approach 2: Estée Lauder Companies Price vs Sales

The Price-to-Sales (P/S) ratio is often viewed as a useful metric for valuing consumer product companies like Estée Lauder, particularly when profits are not consistent or earnings are negative. It reflects how much investors are willing to pay for each dollar of revenue, helping assess whether a stock is richly or fairly valued based on its top-line performance rather than earnings.

Growth expectations and perceived business risks have a significant influence on what counts as a “normal” or fair P/S ratio. Fast-growing or lower-risk companies can command higher multiples, while sluggish or riskier firms usually see lower ratios.

Estée Lauder’s current P/S ratio stands at 2.46x. For context, this is just above the average for similar peers at 2.38x and notably higher than the broader personal products industry average of 1.09x. While traditional analysis might rely on these benchmarks alone, Simply Wall St’s proprietary “Fair Ratio” gives a more tailored view. The Fair Ratio, at 2.28x for Estée Lauder, takes into account not just its industry, but also growth prospects, profit margins, risk factors, and the company’s size. This methodology helps weed out the distortions that pure peer or sector averages can create and offers a fairer, more nuanced comparison tailored to the business.

Comparing Estée Lauder’s current P/S of 2.46x with its Fair Ratio of 2.28x suggests the stock may be trading at a modest premium, but not to a degree that stands out when considering its growth and quality. Since the difference is less than 0.10, it is best judged as ABOUT RIGHT.

Result: ABOUT RIGHT

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1394 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Estée Lauder Companies Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives: a practical, easy-to-use feature on Simply Wall St's Community page, trusted by millions of investors. This feature lets you connect your understanding of Estée Lauder Companies’ business story directly to key financial forecasts and a fair value estimate.

A Narrative is more than just a number. It is your specific perspective on the company's future, where you outline what you believe will drive Estée Lauder’s revenues, margins, and risks, and what that means for its fair value today. Narratives link what you know about the company's market, strategy, and potential to a set of numbers and valuations, making sense of the moving pieces behind every price.

With Narratives, you can easily see whether your view suggests the stock is a buy, hold, or sell by comparing your fair value to the current share price. Your Narrative automatically updates as new earnings or news come in. For example, one investor may have a bullish Narrative, believing Estée Lauder will gain share in emerging markets and digital sales, translating to a high fair value above $120. Another may highlight risks from restructuring and China exposure, arriving at a cautious value near $61. Narratives distill these stories and assumptions into a dynamic, actionable investing tool tailored to you.

Do you think there's more to the story for Estée Lauder Companies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com