European Stocks That May Be Trading Below Estimated Value

As European markets experience a period of growth, with major indices like the STOXX Europe 600 and Germany's DAX posting gains, investors may find opportunities in stocks that are potentially trading below their estimated value. In this environment, identifying undervalued stocks involves assessing companies that demonstrate solid fundamentals and potential for recovery or growth despite current market fluctuations.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Truecaller (OM:TRUE B) | SEK29.20 | SEK56.88 | 48.7% |

| Stratec (XTRA:SBS) | €22.60 | €45.19 | 50% |

| STEICO (XTRA:ST5) | €20.60 | €40.79 | 49.5% |

| Nordisk Bergteknik (OM:NORB B) | SEK11.90 | SEK23.59 | 49.5% |

| Lingotes Especiales (BME:LGT) | €5.55 | €11.03 | 49.7% |

| GomSpace Group (OM:GOMX) | SEK16.66 | SEK32.65 | 49% |

| Axfood (OM:AXFO) | SEK259.20 | SEK507.86 | 49% |

| Atea (OB:ATEA) | NOK151.20 | NOK296.06 | 48.9% |

| Aquafil (BIT:ECNL) | €1.936 | €3.85 | 49.7% |

| Absolent Air Care Group (OM:ABSO) | SEK240.00 | SEK473.04 | 49.3% |

We're going to check out a few of the best picks from our screener tool.

YIT Oyj (HLSE:YIT)

Overview: YIT Oyj offers construction services in Finland, the Czech Republic, Slovakia, Poland, and internationally with a market cap of €679.02 million.

Operations: The company's revenue is derived from Infrastructure (€452 million) and Building Construction (€672 million) segments.

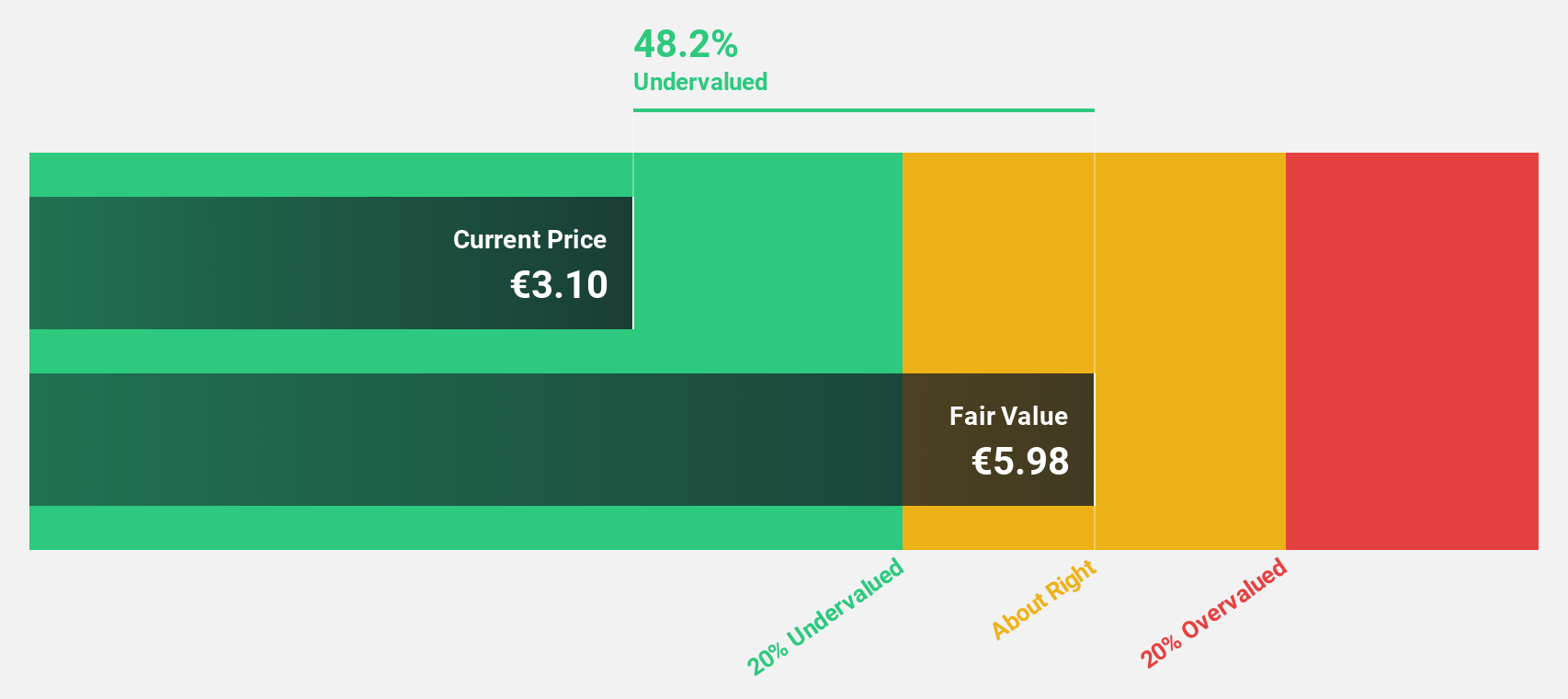

Estimated Discount To Fair Value: 43.2%

YIT Oyj is trading at a substantial discount, approximately 43.2% below its estimated fair value of €5.19, highlighting its potential as an undervalued stock based on cash flows. Despite its low forecasted return on equity of 5.4%, YIT's earnings are expected to grow significantly at 88.9% annually over the next three years, outpacing the Finnish market's revenue growth rate of 4%. However, YIT's debt coverage by operating cash flow remains inadequate.

- According our earnings growth report, there's an indication that YIT Oyj might be ready to expand.

- Unlock comprehensive insights into our analysis of YIT Oyj stock in this financial health report.

Atal (WSE:1AT)

Overview: Atal S.A. operates in Poland, focusing on the construction and sale of residential real estate as well as the rental of commercial properties, with a market cap of PLN2.51 billion.

Operations: The company's revenue segments consist of PLN1.16 billion from development activities and PLN11.03 million from rental services in Poland.

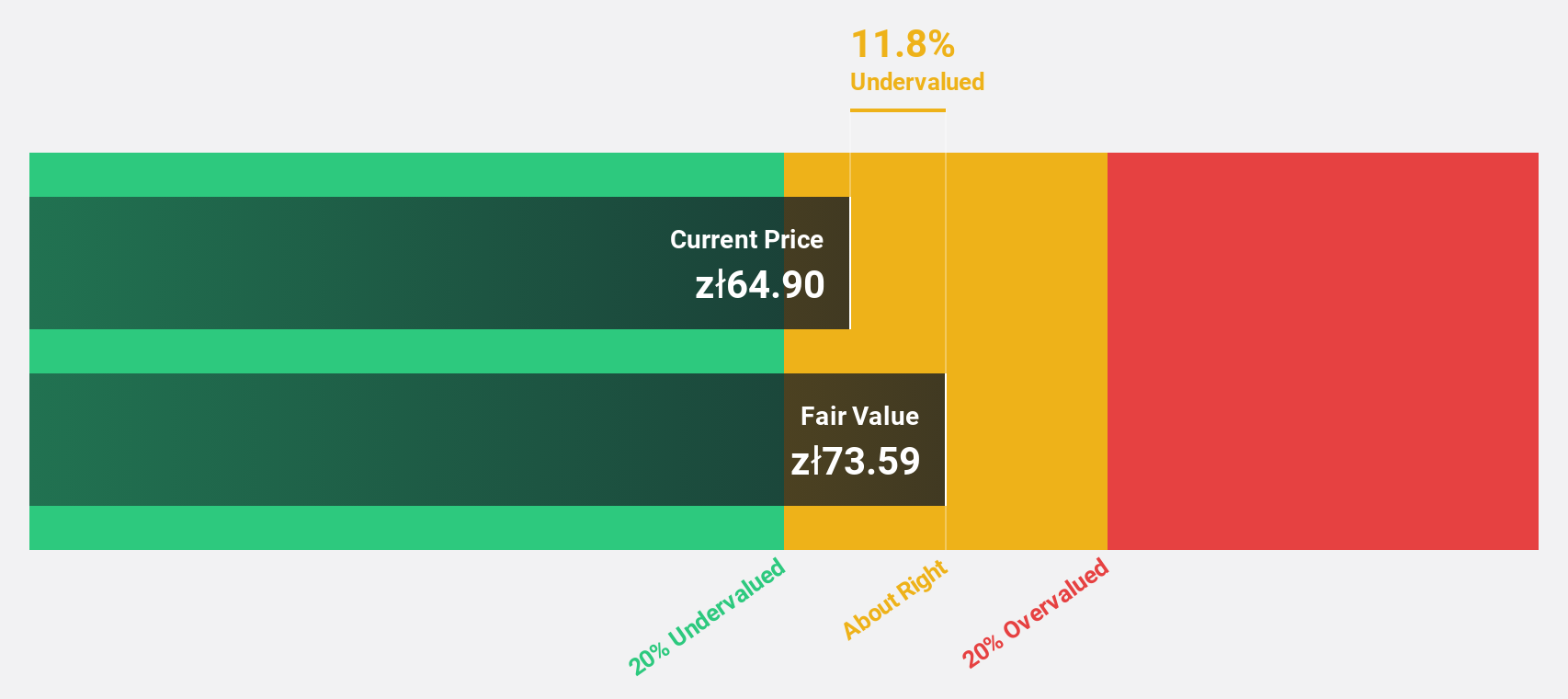

Estimated Discount To Fair Value: 44.9%

Atal is trading at a significant discount, approximately 44.9% below its estimated fair value of PLN105.17, positioning it as an undervalued stock based on cash flows. Despite a recent decline in net income to PLN57.39 million for H1 2025 from PLN154.22 million the previous year, Atal's earnings are forecast to grow significantly at 25.3% annually over the next three years, outpacing the Polish market's growth rate of 15.7%. However, its dividend yield of 9.48% is not well covered by earnings or free cash flows and debt coverage by operating cash flow remains inadequate.

- The analysis detailed in our Atal growth report hints at robust future financial performance.

- Click here to discover the nuances of Atal with our detailed financial health report.

XTB (WSE:XTB)

Overview: XTB S.A. is a brokerage firm offering ETF, currency derivatives, commodities, indices, stocks, and bonds services across Central and Eastern Europe, Western Europe, Latin America, and the Middle East with a market cap of PLN8.05 billion.

Operations: XTB S.A. generates revenue through its brokerage services, which include ETFs, currency derivatives, commodities, indices, stocks, and bonds across various regions including Central and Eastern Europe, Western Europe, Latin America, and the Middle East.

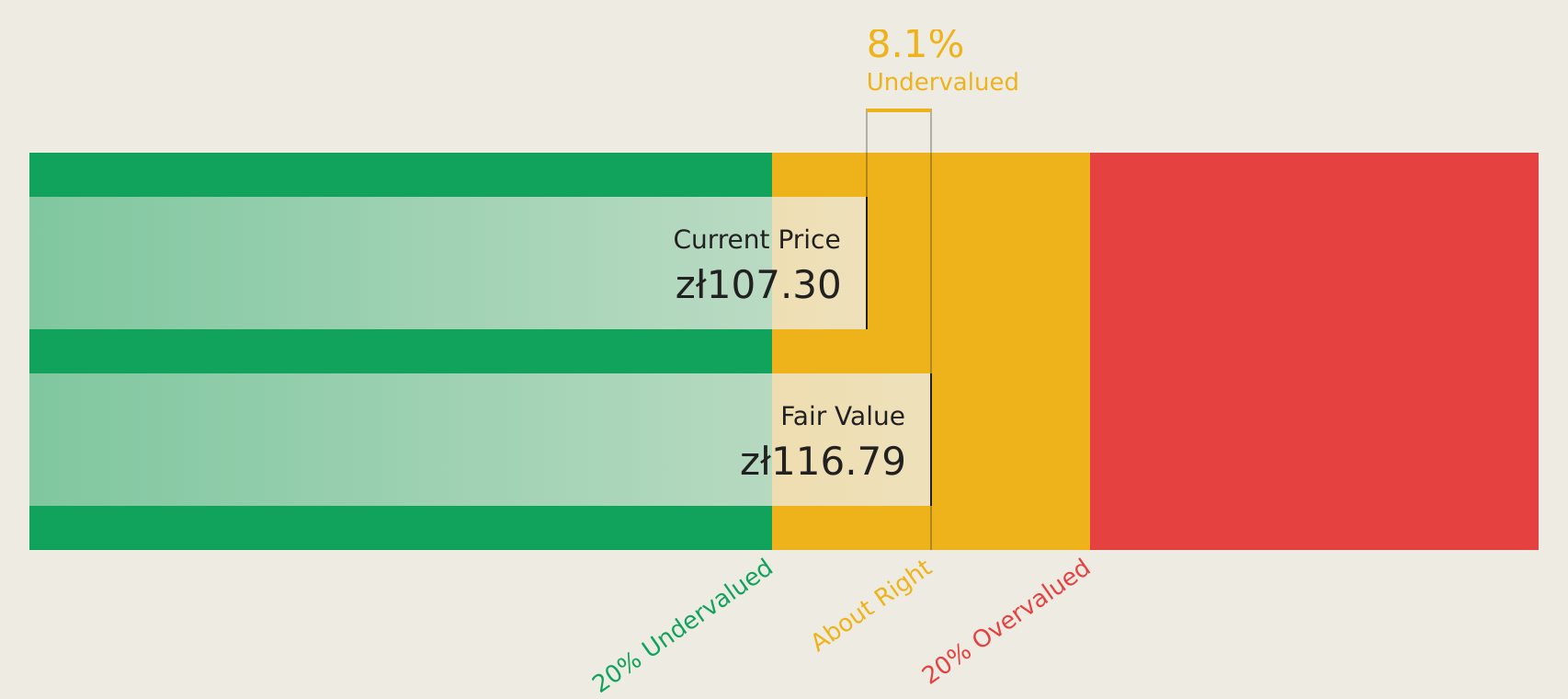

Estimated Discount To Fair Value: 32.6%

XTB is trading at PLN68.5, significantly below its estimated fair value of PLN101.64, highlighting its undervaluation based on cash flows. Despite a decline in net income to PLN53.23 million for Q3 2025 from PLN203.83 million the previous year, earnings are projected to grow substantially at 36.2% annually over the next three years, surpassing Polish market growth rates. However, its dividend yield of 7.96% is not adequately covered by free cash flows.

- The growth report we've compiled suggests that XTB's future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of XTB.

Summing It All Up

- Click through to start exploring the rest of the 202 Undervalued European Stocks Based On Cash Flows now.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com