Is Enphase Energy Looking Attractive After 64% Stock Drop and Sector Uncertainty in 2025?

- Wondering if Enphase Energy is finally a bargain or if there's more pain ahead? You're definitely not alone. Now is a great time to dig into how much the stock is truly worth.

- The share price has dropped sharply lately, losing 15.5% in the past week and down nearly 64% over the past year. This hints at a major shift in how investors perceive growth and risk.

- Much of this decline has been linked to sector-wide concerns around renewable energy stocks and recent regulatory changes impacting solar incentives, which have led to volatility across the industry. Headlines around global supply chain challenges and shifting consumer demand have only amplified the uncertainty for Enphase and its peers.

- If you look at our valuation scorecard, Enphase currently scores 5 out of 6 for being undervalued on key metrics. We will look at what different valuation approaches say about the stock in a moment, but there is a smarter way to put all the numbers together, so stick around for the end.

Find out why Enphase Energy's -63.7% return over the last year is lagging behind its peers.

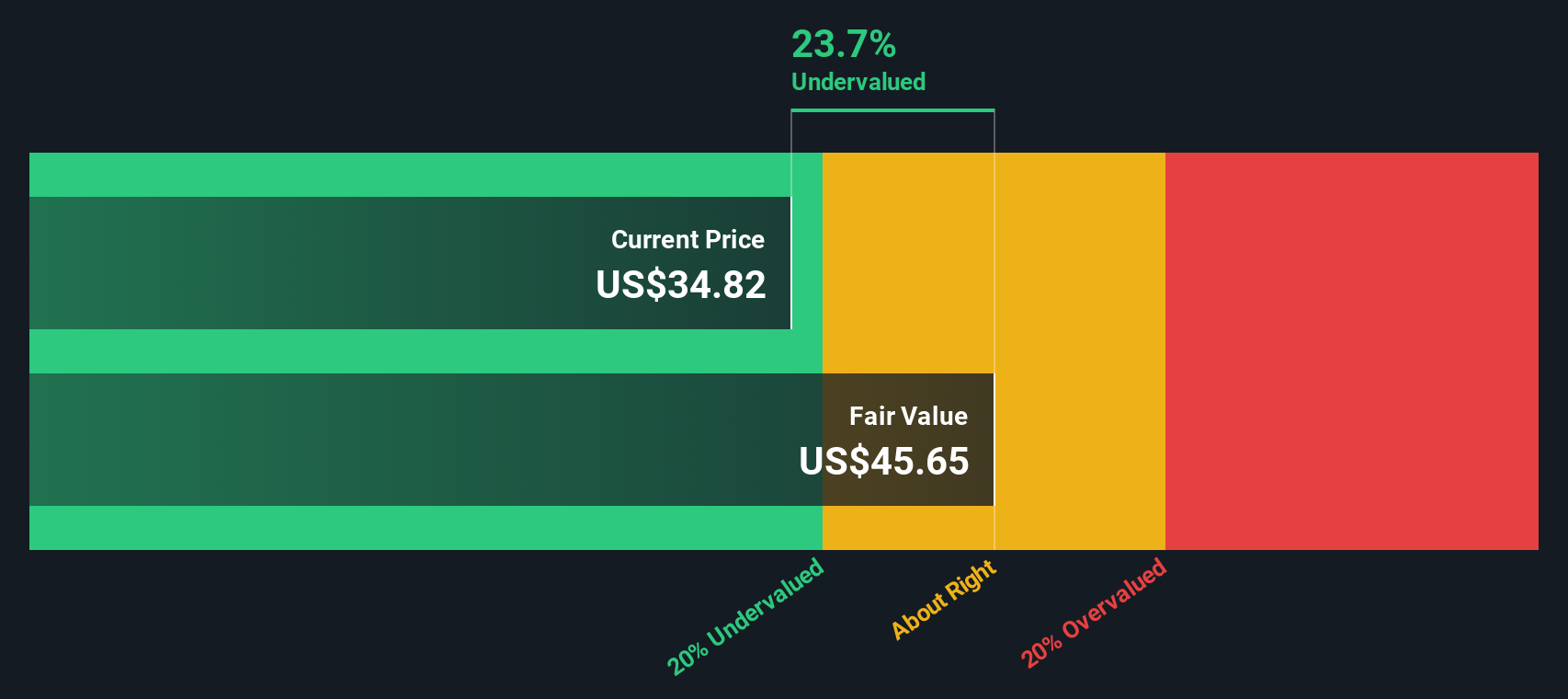

Approach 1: Enphase Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to what they're worth today. This helps investors understand what they should be willing to pay for the stock based on the company’s ability to generate cash in the years ahead.

For Enphase Energy, the current Free Cash Flow (FCF) stands at $203.4 million. Analysts expect this figure to rise steadily over the next several years, with forecasts calling for FCF to reach $445.75 million by the end of 2029. Since analysts only provide estimates for the next five years, Simply Wall St has extrapolated additional projections to provide a fuller long-term picture using a two-stage approach.

Considering these projections, the DCF model calculates an intrinsic value of $39.27 per share. This is about 23.3% higher than where the stock currently trades. The analysis suggests the shares are undervalued based on expected future cash flows.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Enphase Energy is undervalued by 23.3%. Track this in your watchlist or portfolio, or discover 848 more undervalued stocks based on cash flows.

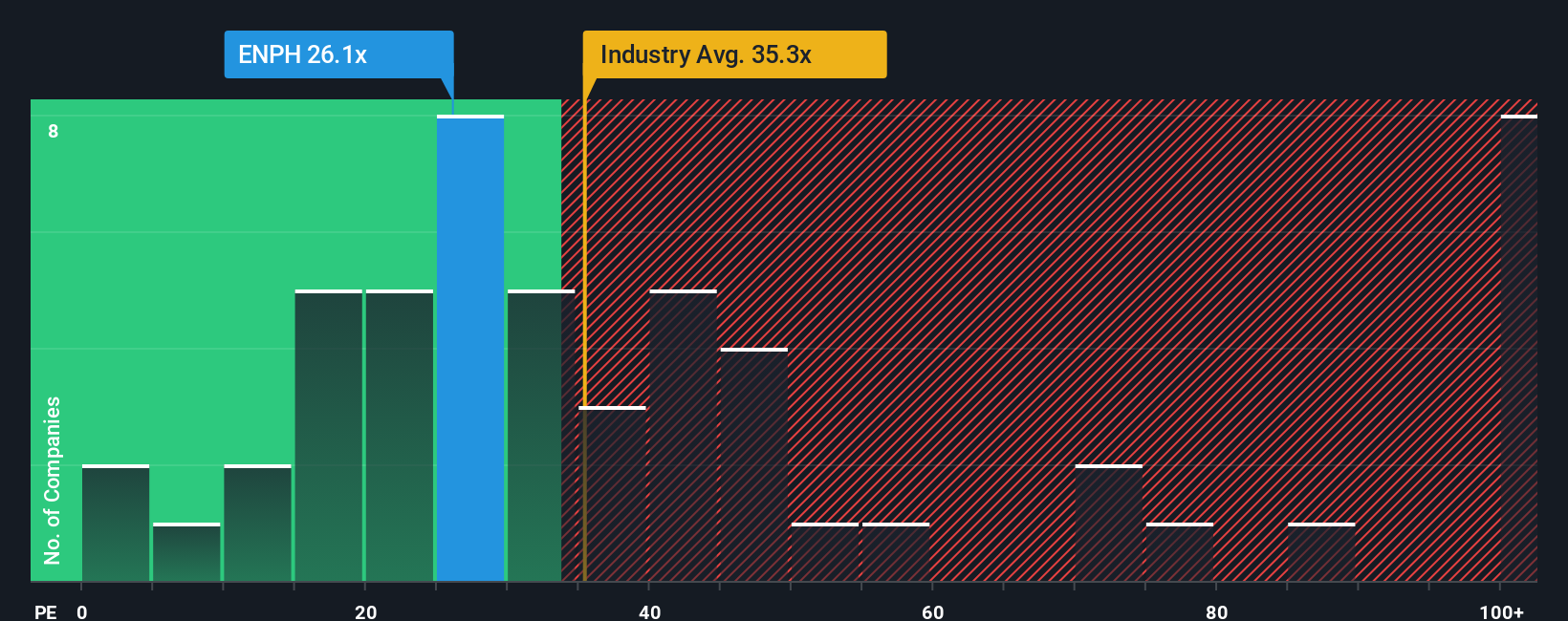

Approach 2: Enphase Energy Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely recognized ways to value profitable companies like Enphase Energy. It essentially tells you how much investors are willing to pay for each dollar of earnings the company generates. Since Enphase is consistently profitable, using the PE ratio provides a clear, apples-to-apples comparison with both its peers and the broader market.

Interpreting the PE ratio requires context. Fast-growing, lower-risk companies can usually support higher PE multiples, while those facing slower growth or higher uncertainty often trade at lower multiples. The appropriate PE ratio is therefore shaped by Enphase’s growth outlook, profitability, and the risks associated with its business.

At the moment, Enphase Energy trades at a PE ratio of 20.16x. That is significantly below the semiconductor industry average of 37.74x, and also much cheaper than its peer group average of 53.40x. However, instead of relying solely on these broad benchmarks, Simply Wall St's proprietary “Fair Ratio” provides a tailored benchmark. It incorporates not just earnings growth, but also factors in profit margins, the company’s industry, market cap, and even specific risks that can impact future performance.

Enphase’s “Fair Ratio” comes in at 21.32x, just a bit higher than its current PE. This suggests that, after adjusting for what matters most to Enphase’s outlook, the stock’s valuation is in line with expectations and is neither meaningfully overvalued nor undervalued at the moment.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1405 companies where insiders are betting big on explosive growth.

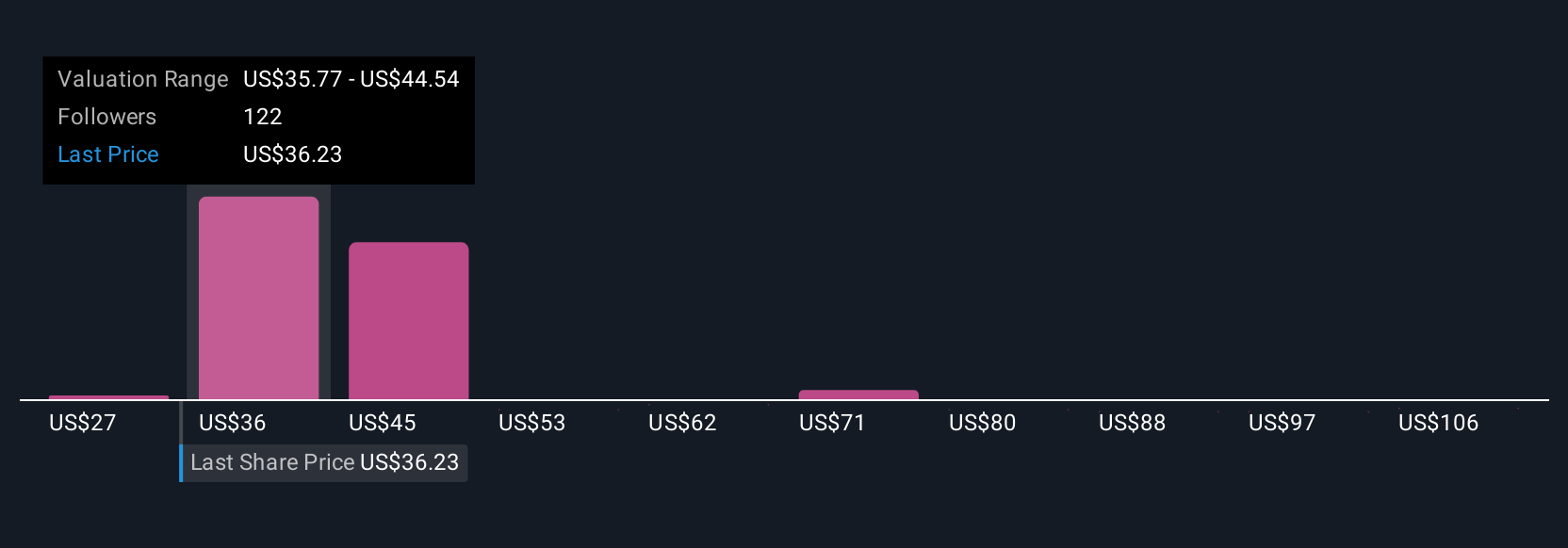

Upgrade Your Decision Making: Choose your Enphase Energy Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal investment story that connects your outlook on a company, such as how its industry, products, or leadership will shape the future, to your assumptions about its revenue, earnings, profit margins, and fair value. Narratives link these real-world beliefs directly to a financial forecast, helping you see if the numbers truly fit the story you tell yourself about Enphase Energy.

With Simply Wall St’s Community page, Narratives are a simple and accessible tool used by millions of investors. They let you create, share, or follow investor perspectives, and are always updated dynamically when new news or earnings roll in. Narratives make it easy to compare your Fair Value estimate to the current Price, guiding your decisions on when to buy or sell.

For example, one Enphase Narrative expects robust global expansion and product innovation, backing a Fair Value of $85.00. Another sees harsh competition, slower growth, and values the stock at just $27.00. Narratives reveal these differences and keep you focused on your own investment logic so you can stay confidently in control, no matter the market noise.

Do you think there's more to the story for Enphase Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com