Nippon Sanso Holdings (TSE:4091): Assessing Valuation After Earnings Beat, Higher Dividends, and European Growth

Nippon Sanso Holdings (TSE:4091) just delivered its first-half earnings update, announcing higher revenue and a notable jump in net income. Following this performance, the company has raised both its interim and annual dividend forecasts.

See our latest analysis for Nippon Sanso Holdings.

Momentum around Nippon Sanso Holdings has been mixed this year. While the company’s upbeat earnings and higher dividends helped maintain a supportive narrative, recent months saw the share price soften, with a 3.3% one-month pullback. However, the longer-term story remains remarkably strong. Investors who have held on over the last three or five years still enjoy total shareholder returns of 136% and 234% respectively, even with a -4.7% total return over the past year. With strategic acquisitions and European growth adding substance to its outlook, the stock’s current market action appears to be a pause within a much bigger, multi-year climb.

If you’re interested in uncovering more opportunities, now’s an ideal time to broaden your perspective and discover fast growing stocks with high insider ownership

With fresh earnings growth, higher dividends, and continued expansion in Europe, the question now is whether Nippon Sanso Holdings is trading at an attractive valuation or if investors have already priced in its ambitions for future growth.

Most Popular Narrative: 4.9% Undervalued

The most widely followed narrative places Nippon Sanso Holdings' fair value at ¥5,332.86, which is about 5% higher than its last close of ¥5,073. This suggests there could be some meaningful upside. The rationale for this estimate centers on expectations for lasting industry transformation and operational improvements that may drive the company’s next phase of growth.

Anticipated acceleration in demand for industrial and specialty gases linked to the global shift to clean fuels and hydrogen is likely to benefit Nippon Sanso. Given its expertise and recent disciplined CapEx positioning, this could drive future revenue growth as delayed customer investment resumes, especially with policy and economic clarity.

What are the bold assumptions driving this valuation? Find out how the company’s future earnings, profit margins, and a surprisingly high profit multiple set the stage for its potential market rerating. You’ll want to see what’s under the hood of these projections, as there is more to the fair value than meets the eye.

Result: Fair Value of ¥5,332.86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent economic uncertainty and foreign exchange volatility could easily undermine these upbeat projections and have a negative impact on Nippon Sanso Holdings’ earnings outlook.

Find out about the key risks to this Nippon Sanso Holdings narrative.

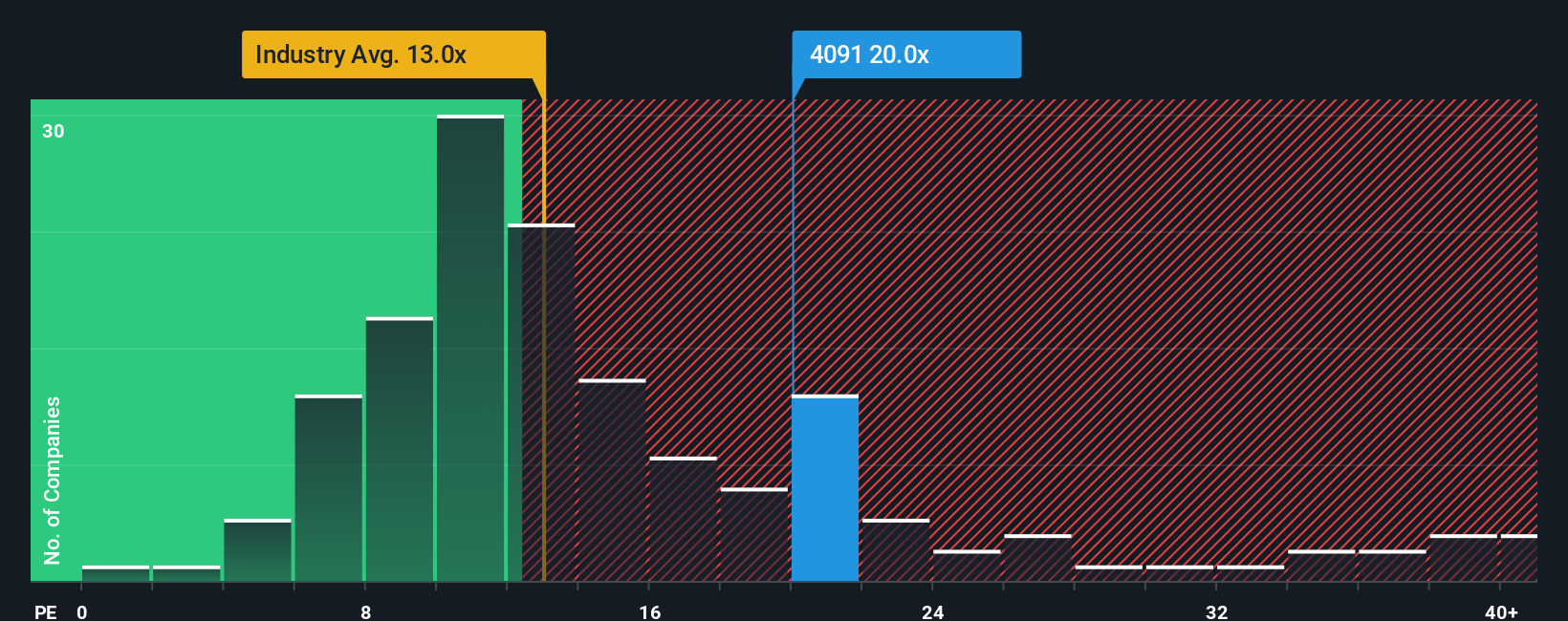

Another View: Multiples Tell a Different Story

Switching gears from fair value estimates, if we look at Nippon Sanso Holdings through the lens of its price-to-earnings ratio, things don’t seem as cheap. The company currently trades at 22.4 times earnings, which is higher than the peer average of 14.5 times and the industry’s 13.2 times. The fair ratio our analysis suggests is 20.4 times, meaning the stock is a bit expensive relative to where the market could drift. This introduces valuation risk if momentum fades. Does this multiple signal sustained optimism, or could expectations shift?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Nippon Sanso Holdings Narrative

If you prefer to dig deeper or would rather reach your own conclusions, you can shape your own perspective on Nippon Sanso Holdings in just a few minutes: Do it your way

A great starting point for your Nippon Sanso Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors don't settle for one opportunity; they keep their radar up for big movers across markets. See which standouts deserve a spot on your watchlist today.

- Power up your portfolio with secure income streams by adding these 21 dividend stocks with yields > 3%, which offers yields above 3% and robust fundamentals.

- Step ahead of the curve by tracking breakthroughs in medical technology among these 34 healthcare AI stocks, reshaping patient care and pharmaceutical innovation.

- Ride the next wave of digital finance evolution with these 81 cryptocurrency and blockchain stocks, unlocking possibilities in blockchain and cryptocurrency markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com