Is Super Micro Computer’s 75% Jump in 2025 Justified After AI Partnership Surge?

- Ever wondered if Super Micro Computer is fairly priced right now? Let’s break down what today’s price really means for investors thinking about growth, value, or risk.

- The stock has delivered a jaw-dropping 1,756.6% return over five years, with strong momentum continuing in 2024, as shares are up 75.3% year to date.

- Super Micro Computer has been in the spotlight as AI and data center demands drive industry headlines, fueling renewed interest across the tech sector. This surge comes after several high-profile partnerships and industry-wide optimism about the company’s role in enabling next-generation infrastructure.

- Looking at valuation, Super Micro Computer scores just 1 out of 6 on our undervaluation checks. So is its price justified by the numbers, or is there something more going on under the hood? Ahead, we’ll dive into the standard valuation approaches, with a fresh perspective at the end you won’t want to miss.

Super Micro Computer scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Super Micro Computer Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them to reflect their value in today's dollars. This approach helps investors gauge whether the current share price makes sense given the company's real, underlying earning power.

Super Micro Computer has reported Free Cash Flow (FCF) of $1.52 Billion over the last twelve months. Analysts expect future FCF to fluctuate, with projections showing $653 Million in 2028, while estimates for 2026 temporarily dip into negative territory before rebounding in subsequent years. Since analysts only provide up to five years of forecasts, the model extrapolates cash flows further out and accounts for uncertainty as time goes on.

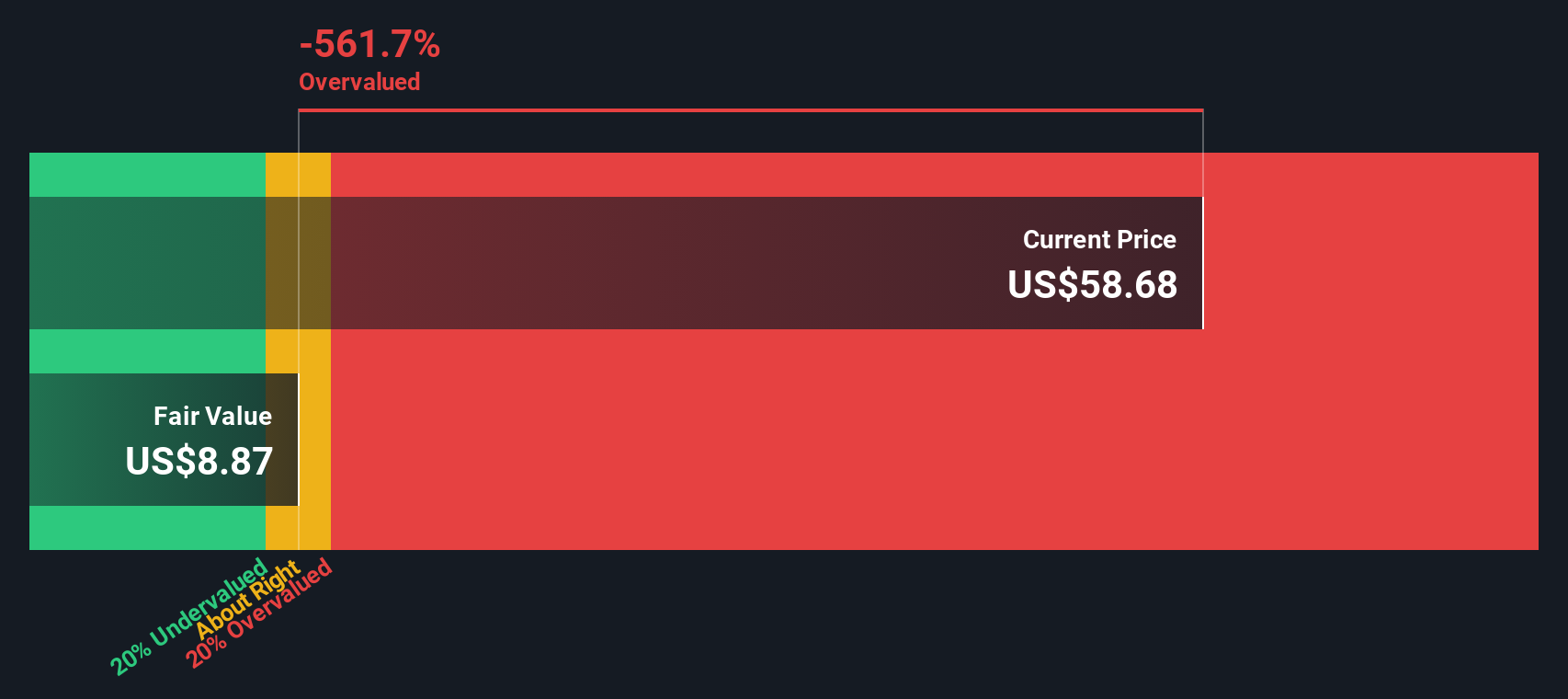

By discounting all future estimated cash flows back to the present, the DCF analysis produces an estimated intrinsic value per share of $3.66. This figure is dramatically lower than the company's current share price, implying that Super Micro Computer is trading at a 1,340.4% premium to its DCF value. According to this model, the market price is far above what the underlying cash flows would justify, even with optimistic growth assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Super Micro Computer may be overvalued by 1340.4%. Discover 849 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Super Micro Computer Price vs Earnings

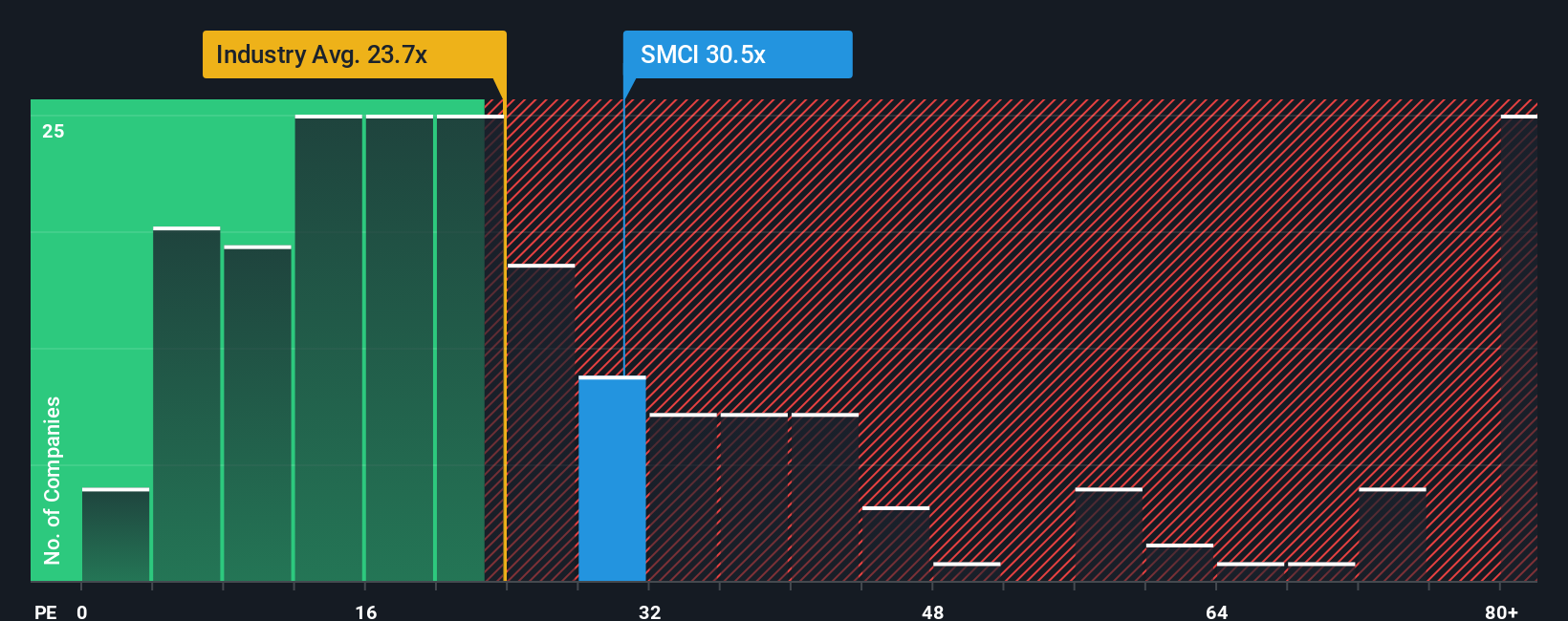

For profitable companies like Super Micro Computer, the Price-to-Earnings (PE) ratio is a go-to valuation method. This metric helps investors understand how much they are paying for each dollar of a company’s earnings, making it crucial for businesses with solid profits.

The "right" or "fair" PE ratio depends on several factors, such as how quickly a company is expected to grow earnings and what risks might stand in its way. Fast-growing, stable companies generally deserve a higher PE ratio. In contrast, slower or riskier businesses command lower multiples.

Super Micro Computer currently trades at a PE ratio of 29.9x. For context, the Tech industry’s average PE is 23.8x, while the company's peers average 21.9x. This means Super Micro Computer is valued at a premium compared to both the broader sector and its closest competitors.

Simply Wall St’s proprietary Fair Ratio takes this analysis further by factoring in growth prospects, profit margins, business model risks, industry nuances, and company size. This all-in-one approach provides a tailored benchmark that better reflects what the company might deserve compared to one-size-fits-all industry or peer averages.

According to the Fair Ratio, Super Micro Computer would trade at 65.9x. Comparing this to its actual PE of 29.9x, the stock appears undervalued using this method, as the market is assigning less value than the company’s fundamentals would justify.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1380 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Super Micro Computer Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your unique, story-driven perspective on a company, combining your assumptions about future revenue, profit margins, and fair value with your understanding of its business prospects and risks. Instead of relying solely on historic data or static analyst targets, Narratives let you connect the company's story to a dynamic financial forecast, making your investment decision both personal and well-informed.

Narratives are easy to use and fully accessible in the Simply Wall St Community page, where millions of investors share their views. With Narratives, you can quickly see how your chosen fair value compares to Super Micro Computer’s current share price, helping you decide when to buy or sell. They automatically update as key information changes, such as earnings reports or news, so your analysis stays current without extra effort.

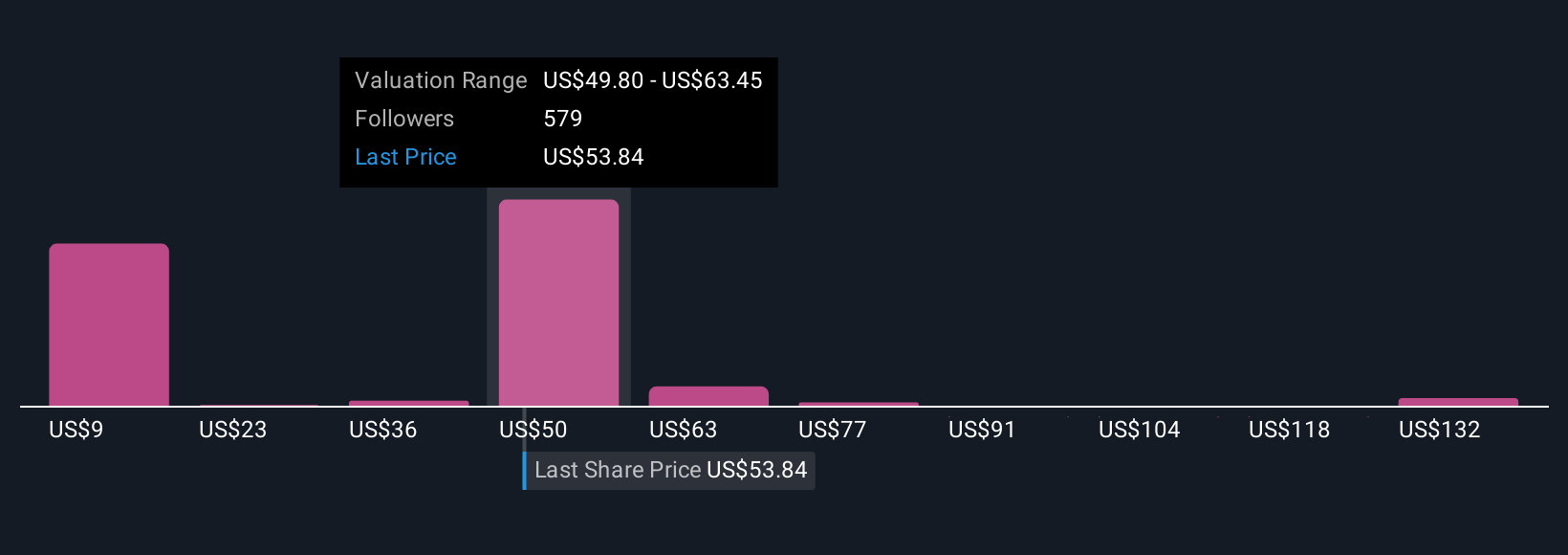

For example, some investors, focused on fast AI growth and strong partnerships, set a Narrative with a fair value above $74 per share, expecting Super Micro Computer to more than double its revenue by 2028. Others, concerned about governance and tougher competition, estimate a fair value near $26, reflecting a much more cautious outlook. Narratives empower you to take ownership of your investment thesis and adjust your view as the story evolves.

For Super Micro Computer, we'll make it really easy for you with previews of two leading Super Micro Computer Narratives:

🐂 Super Micro Computer Bull Case

Bull Narrative Fair Value: $74.53

Current price is 29.3% below this fair value

Assumed Revenue Growth: 50%

- Management forecasts bold revenue growth through innovative technologies like Direct Liquid Cooling and strong guidance for 2025 and 2026, anticipating $50bn in revenue by 2028.

- Strategic partnerships with industry giants such as Nvidia, AMD, xAI, and Intel position Super Micro as one of the top AI infrastructure providers, benefiting from expansion in Cloud, 5G, and storage markets.

- Following accounting controversy and successful remediation, the narrative expects renewed investor confidence and emphasizes both short and long-term upside as one of the most consolidated AI growth opportunities.

🐻 Super Micro Computer Bear Case

Bear Narrative Fair Value: $50.59

Current price is 4.2% above this fair value

Assumed Revenue Growth: 28.6%

- Analysts see global AI and analytics demand fueling robust sales and margin improvements, but highlight exposure to customer concentration and supply chain risk as threats to earnings stability.

- Competitive pressures and risk of commoditization could erode margins, especially with high reliance on a handful of major customers and volatile product transitions.

- The consensus price target is $50.59, which is 4.2% below the current price, reflecting tempered growth and profitability projections that require careful scrutiny of the company’s ability to sustain its current valuation.

Do you think there's more to the story for Super Micro Computer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com