Is Kraft Heinz a Value Opportunity After a 20.8% Decline in 2025?

- Curious if Kraft Heinz is a bargain or a value trap? Here’s what makes this giant in food staples worth a closer look right now.

- Kraft Heinz stock has dropped 4.9% over the last week and is down 20.8% for the year so far, which is turning some heads about its future prospects and risk profile.

- Recent headlines have focused on changes in consumer trends and company efforts to adapt its product lineup. This context helps explain the recent dip in share price and why investors are watching closely for any renewed growth catalysts.

- On our quick-check valuation score, Kraft Heinz clocks in at 4 out of 6, suggesting it is undervalued in several key areas. Next, we will walk through the usual ways to value a stock like this, but stick around for an even better approach revealed at the end.

Find out why Kraft Heinz's -23.6% return over the last year is lagging behind its peers.

Approach 1: Kraft Heinz Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates the true value of a company by projecting its future cash flows and discounting them back to today, reflecting the time value of money. This approach aims to provide an intrinsic valuation based on financial fundamentals instead of market sentiment.

Kraft Heinz’s most recent Free Cash Flow (FCF) is approximately $3.45 billion. Analysts have provided FCF estimates out to 2028, projecting it will reach around $3.79 billion in that year. Beyond this, future projections have been modeled to 2035, gradually increasing to over $4.65 billion as per extrapolations. These cash flows are all denominated in US dollars and reflect a steady, if modest, growth outlook.

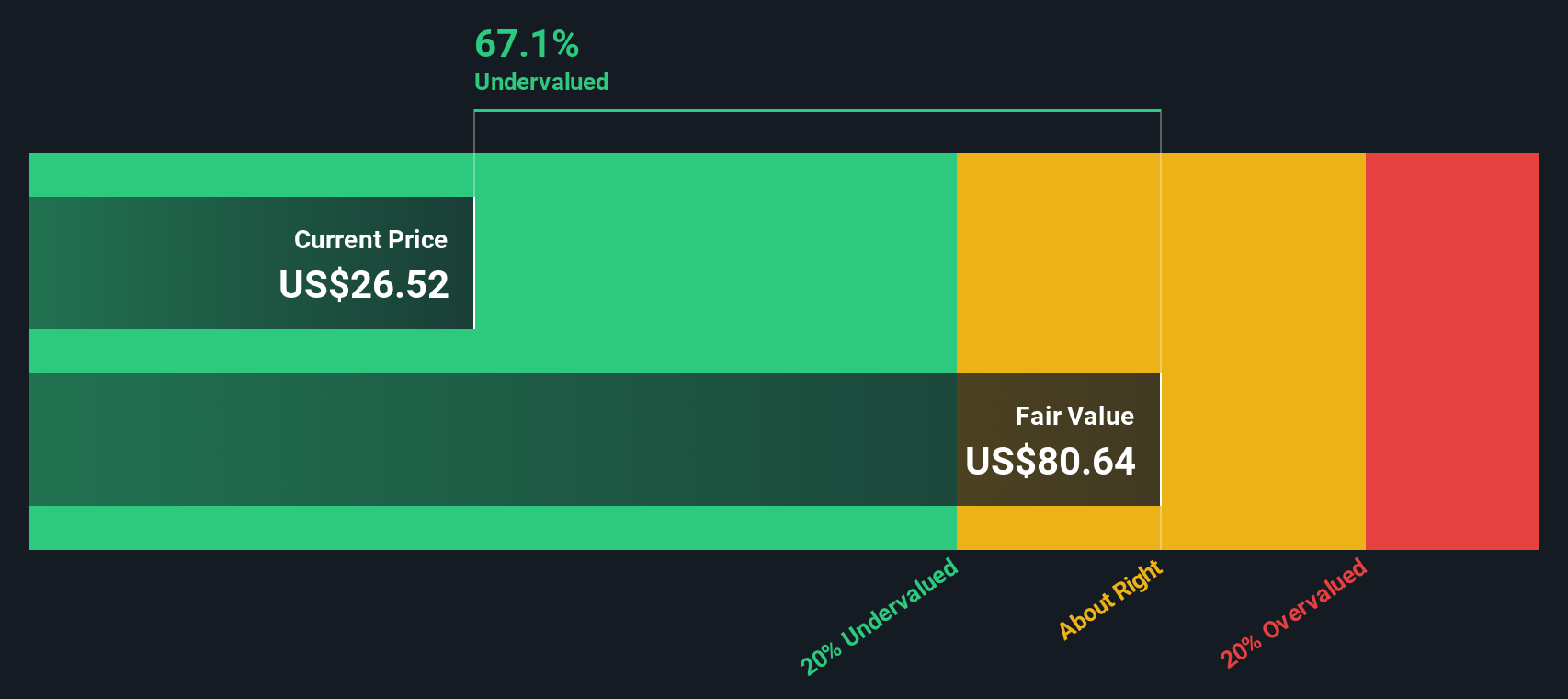

By applying the 2 Stage Free Cash Flow to Equity method, the model calculates an estimated intrinsic fair value per share of $81. Compared to the current share price, this implies the stock is trading at a substantial 69.9% discount to its intrinsic value. This suggests Kraft Heinz may be significantly undervalued based on cash flow projections alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kraft Heinz is undervalued by 69.9%. Track this in your watchlist or portfolio, or discover 848 more undervalued stocks based on cash flows.

Approach 2: Kraft Heinz Price vs Sales

For established, profitable food companies like Kraft Heinz, the Price-to-Sales (P/S) ratio is a particularly useful metric. It gives investors a sense of how much they are paying for each dollar of revenue, which is a helpful gauge in an industry where profit margins are stable but not extravagant. The P/S ratio is less prone to distortion from non-cash charges or temporary margin swings than alternatives like Price-to-Earnings or Price-to-Book. This makes it relevant for assessing stalwart brands in competitive consumer markets.

What is a “normal” or “fair” P/S ratio? Expectations for sales growth, risk, and profitability all feed into what investors are willing to pay for each dollar of revenue. If a company is expected to grow quickly or is especially resilient, its P/S ratio can justifiably be higher. Conversely, slower growth or higher risk typically demands a discount.

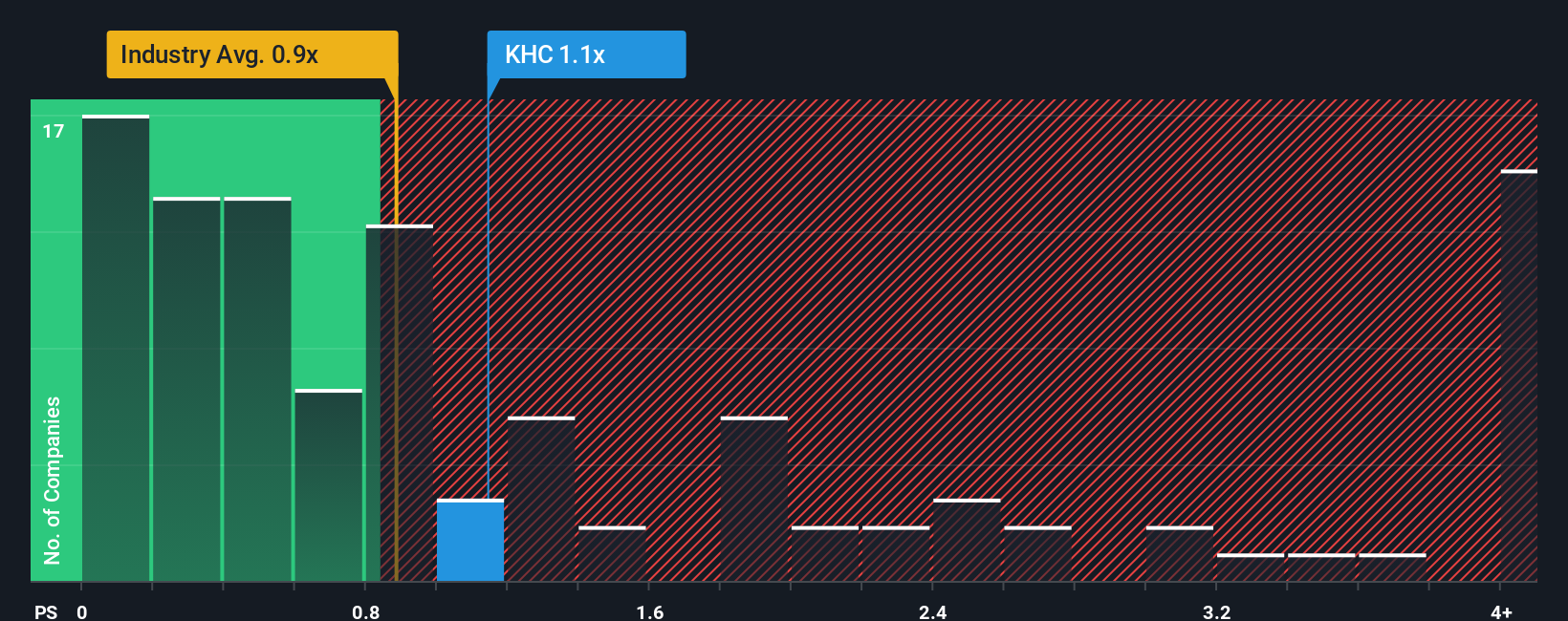

Kraft Heinz currently trades at a P/S ratio of 1.14x. This sits slightly above the industry average of 0.91x, but below the peer average of 1.76x. Simply Wall St’s proprietary “Fair Ratio” for Kraft Heinz is calculated at 1.44x, taking into account the company’s expected growth, profit margin, risk profile, industry dynamics, and market capitalization. Unlike a simple comparison with peers or industry, this Fair Ratio is more tailored and holistic. It blends the nuances of Kraft Heinz’s competitiveness and future prospects into a single, actionable multiple.

Comparing Kraft Heinz’s current 1.14x P/S to its Fair Ratio of 1.44x shows the stock is trading noticeably below what is considered fair value for a company with its characteristics and outlook.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1380 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kraft Heinz Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are a straightforward, insightful approach that lets investors attach their own story to a company, then connect that perspective directly to financial estimates like fair value and future growth. Instead of just following the numbers, you add context: your view on Kraft Heinz’s competitive position, market changes, management actions, and industry trends, all linked to your own forecasts for revenue, earnings, and margins.

Narratives make stock analysis personal yet disciplined, helping you translate your outlook into a specific fair value so you can easily compare it to today’s price and decide when to buy or sell. Available right on Simply Wall St’s Community page, Narratives are used by millions of investors and update dynamically as new news or earnings arrive, meaning your investment case stays relevant. For example, some investors may tell a positive Narrative backed by anticipated growth in emerging markets, innovation, and higher margins, expecting Kraft Heinz to reach a value as high as $51 per share. More cautious users focus on weaker core performance and margin pressures, setting fair value closer to $27. With Narratives, it is simple, transparent, and always tailored to your own view.

Do you think there's more to the story for Kraft Heinz? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com