Examining Eli Lilly’s High Valuation After Breakthrough Weight-Loss Drug Headlines in 2025

- Wondering if Eli Lilly's sky-high stock price actually reflects real value, or if there are still opportunities to be found? You are not alone. Let's dig into what the numbers and bigger picture say.

- Eli Lilly's share price has popped 12.0% over the last month, and while it is up 479.0% over five years, it actually dipped -3.2% in the last year, hinting at changing investor sentiment or shifting risk perceptions.

- Recent headlines have swirled around Eli Lilly's breakthroughs in weight-loss drugs and regulatory wins, fueling optimism for long-term growth. At the same time, some analysts are raising questions about competitive pressures and future margins as new therapies enter the market.

- When we crunch the numbers, Eli Lilly scores just 2 out of 6 on our standard valuation checks. It is worth exploring if traditional models are missing something important here. Stick around, because we will get into multiple approaches and a fresh perspective on value by the end.

Eli Lilly scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Eli Lilly Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to today's dollars. This method gives investors a sense of what the business could be worth based on its ability to generate free cash flow over time.

For Eli Lilly, the most recent reported Free Cash Flow (FCF) was approximately $2.25 billion. Analysts project aggressive growth; by 2029, the FCF is expected to reach nearly $34.1 billion. While analysts have published estimates for the next five years, Simply Wall St extrapolates these further to provide a longer-term outlook.

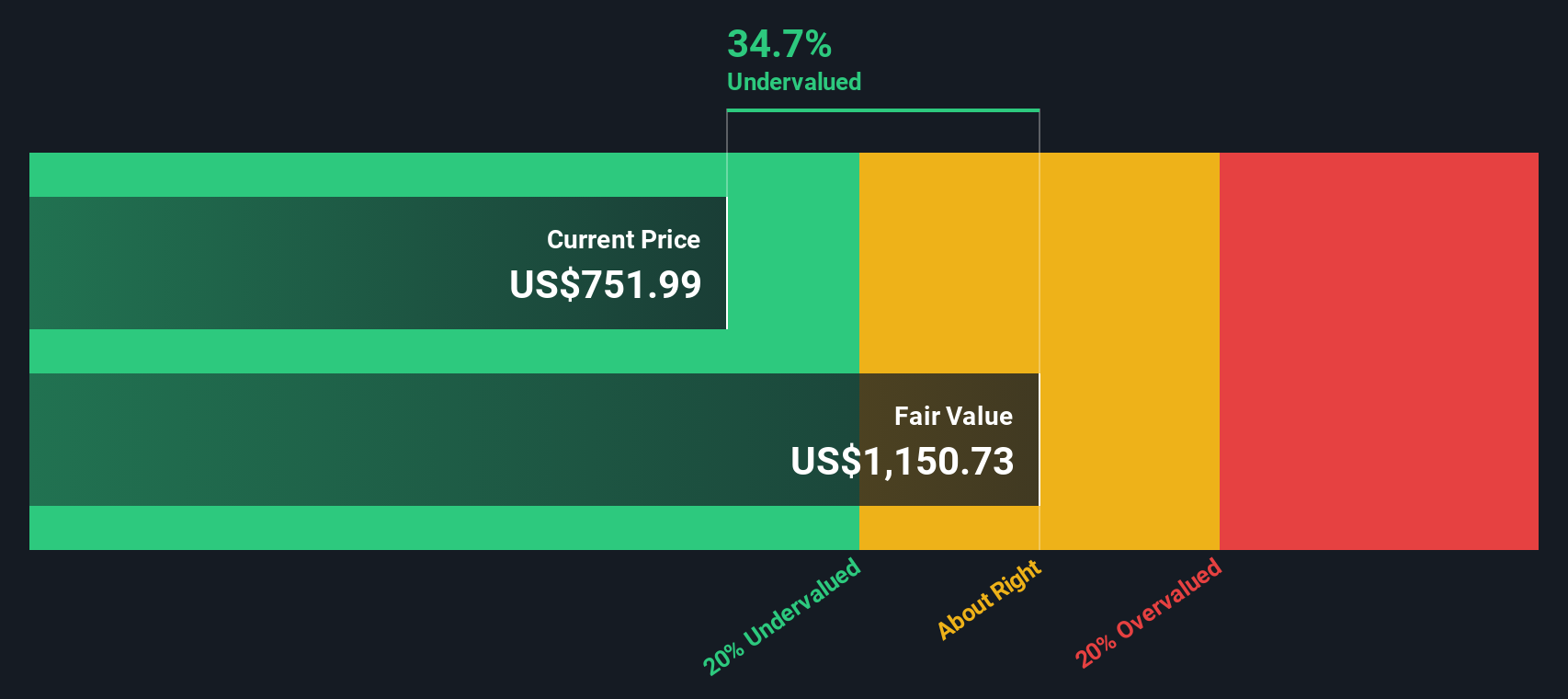

All figures are in US dollars, which matches Eli Lilly's listing currency. Using the two-stage DCF model, the estimated intrinsic value of the company comes to $1,169 per share. This figure suggests that Eli Lilly's stock is currently trading at a 30.4% discount to its calculated fair value.

Based on this approach, Eli Lilly appears significantly undervalued using long-term cash flow projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Eli Lilly is undervalued by 30.4%. Track this in your watchlist or portfolio, or discover 851 more undervalued stocks based on cash flows.

Approach 2: Eli Lilly Price vs Earnings

The Price-to-Earnings (PE) ratio is a fundamental tool for valuing profitable companies like Eli Lilly, as it helps investors compare how much they are paying for each dollar of current earnings. The PE ratio is particularly useful when evaluating well-established businesses, since it reflects both market expectations of future growth and the perceived risk surrounding those earnings.

A higher PE ratio can indicate that investors expect faster growth or see the company as less risky, while a lower PE often signals the opposite. Eli Lilly’s current PE ratio is 52.9x, which is well above the pharmaceuticals industry average of 17.9x and the average among similar peers at 15.3x. At first glance, this might suggest the stock is significantly overvalued based on traditional benchmarks.

However, Simply Wall St’s “Fair Ratio” offers a more nuanced perspective. This proprietary figure, 39.7x for Eli Lilly, factors in details like its robust expected earnings growth, profit margin, industry dynamics, market capitalization, and unique risks. By considering these elements, the Fair Ratio gives a tailored valuation that peer and industry averages cannot match.

Comparing Eli Lilly’s actual PE of 52.9x to its Fair Ratio of 39.7x, the stock trades at a premium above what would be considered fair based on its risk and growth profile.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1396 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Eli Lilly Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative makes investing personal and actionable by letting you define a company's story, your view on its future prospects, risks, and strengths, and connect that story to a forecast of revenue, margins, and eventual fair value. Narratives bridge the gap between the reasons you believe in a company and the numbers behind your investment decisions, so you are not just reacting to data but using it to validate your own thinking.

On Simply Wall St’s Community page, millions of investors post their Narratives, making this powerful approach easy and accessible for you too. By using Narratives, you can quickly compare any fair value estimate to the latest share price and see if the stock matches your view for buying, holding, or selling. These Narratives are automatically updated when fresh news, earnings, or industry events emerge, so your investment thesis is always current.

For example, some investors see Eli Lilly’s growth in next-generation obesity treatments and U.S. market advantages supporting a fair value above $1,180, while others focus on regulatory risks and margin pressures, estimating a much more cautious target of $650. This highlights how Narratives put your unique perspective and decision-making at the center of the investing process.

Do you think there's more to the story for Eli Lilly? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com